Robust Growth, Digital Transformation, and Government Initiatives Drive Success

By MYBRANDBOOK

The Indian IT hardware market has witnessed remarkable growth and transformation over the years, propelled by advancements in technology and the increasing demand for digital infrastructure. In the financial year 2022-23, the market continued to expand, driven by factors such as remote work and education, digital transformation initiatives, and government-led initiatives like Make in India and Atmanirbhar Bharat.

Market Size and Growth: The IT hardware market in India experienced robust growth in FY22-23. According to industry reports, the market size reached an estimated value of USD 25 billion, reflecting a growth rate of 10% compared to the previous fiscal year. The surge in demand for laptops, desktops, servers, networking equipment, storage devices, and peripherals contributed significantly to the market’s expansion.

Remote Work and Education: The COVID-19 pandemic accelerated the adoption of remote work and online education, creating a surge in demand for IT hardware. Organizations and educational institutions swiftly embraced remote working and digital learning models, leading to an increased need for laptops, desktops, and other related equipment. As a result, many IT hardware companies experienced heightened demand for their products during this period.

Digital Transformation Initiatives: The Indian government’s Digital India program and various digital transformation initiatives across industries have been instrumental in driving the growth of the IT hardware market. The adoption of cloud computing, big data analytics, artificial intelligence, and the Internet of Things (IoT) has necessitated investments in advanced IT infrastructure. Organizations have been focusing on upgrading their hardware capabilities to support these technological advancements, which has further fueled the demand for IT hardware solutions.

Government-led Initiatives: Government initiatives like Make in India and Atmanirbhar Bharat have played a crucial role in promoting domestic manufacturing and reducing dependency on imports. These initiatives have encouraged several IT hardware companies to establish or expand their manufacturing facilities in India. With incentives and support from the government, the domestic production of laptops, desktops, and other IT hardware components has witnessed a significant boost, leading to job creation and economic growth.

Key Players and Competition: The IT hardware market in India is highly competitive, with several domestic and international players vying for market share. Some prominent companies operating in the Indian IT hardware space include Dell, HP, Lenovo, Acer, Asus, Apple, Samsung, and Indian brands such as HCL, Wipro, and Micromax. These companies offer a wide range of products catering to different segments and price points.

PC Market

According to the latest data from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker, the traditional PC market in India witnessed a modest year-over-year (YoY) growth of 0.3% in 2022, reaching a total of 14.9 million units. However, the market faced significant challenges in the fourth quarter of 2022 (Oct-Dec), experiencing a steep YoY decline of 28.5%.

Within the PC market, desktops continued to show positive growth, maintaining an upward trend. However, notebooks experienced a sharp YoY decline of 37.8% in the fourth quarter. The consumer segment was particularly affected by inflation and low sentiment, leading to a decline of 27.4%. Furthermore, delayed orders and inventory challenges impacted the enterprise segment, resulting in a significant decline of 42.6% YoY.

In terms of market segments, the government and education sectors emerged as the biggest gainers in 2022, growing YoY at 117.6% and 28.3%, respectively. However, the enterprise segment faced a decline of 5.9% YoY. Desktops showed strong growth, expanding by 32.3% YoY, while workstations grew by 24.7% YoY. Conversely, the notebook category, which accounted for the majority of PC volume, experienced a decline of 8.4% YoY due to softening demand across different segment groups.

The premium notebook segment, comprising devices priced above US$1,000, witnessed a decline of 7.9% YoY in the commercial segment. However, on the consumer side, premium notebooks and MacBooks continued to be popular, resulting in a growth of 14.6% YoY.

In terms of distribution channels, the online channel faced challenges, declining by 9.4% YoY in 2022, with a steeper YoY decline of 37.5% in the fourth quarter (4Q22).

These figures highlight the mixed performance of the traditional PC market in India during 2022, with desktops showing resilience while notebooks faced challenges, particularly in the consumer segment. The government and education sectors exhibited strong growth, but enterprises experienced a decline. The market dynamics, including inflation, low sentiment, and inventory challenges, influenced the overall performance of the PC market in India.

Top 5 Vendors

HP: In 2022, HP Inc. dominated the market with a 30.2% share, driven by strong demand from global accounts and the government segment. Although HP’s notebook sales declined by 10.7% YoY, its desktops and workstations experienced significant YoY gains.

Dell: Dell Technologies secured the second position with a 19.2% share, despite a decline of 18.5% YoY. The company performed well in the commercial segment with a 25.2% share, while its presence in the consumer segment dropped to 12.5%. Dell’s strength remained in serving enterprises, benefiting from increased demand from global accounts and Indian IT/ITES majors.

Lenovo: Lenovo closely followed Dell in third place with an 18.9% share. The company witnessed a 3.1% YoY growth in 2022, experiencing positive momentum in both the consumer and commercial segments. Despite undergoing an inventory correction in 4Q22, Lenovo achieved a 14.1% YoY growth in the SMB segment, which has been a primary driver for the company.

Acer: Acer Group held the fourth position with a 9.9% share. Acer recorded a strong growth of 21% YoY in 2022, primarily fueled by robust demand for commercial desktops. In the commercial desktop segment, Acer ranked second after HP with a 26.7% share, enjoying a YoY growth of 45.7%.

ASUS: ASUS secured the fifth position with a 6.8% share in 2022. The company experienced significant growth in consumer notebooks, ranking third after HP and Lenovo, with a 15.6% share and a YoY growth rate of 20%. ASUS’s focus on expanding its offline channels played a key role in its substantial gains.

Apple: Apple made a noteworthy entry into the top 5 vendors for 4Q22. The company consistently achieved strong numbers in recent quarters and managed to surpass ASUS to secure the fifth spot. While other vendors focused on inventory correction and experienced reduced shipments, Apple witnessed positive traction, growing by 10.9% YoY.

Printer Business

India’s print market showed positive growth in the second quarter of 2022 (Apr-Jun), with shipments reaching 0.84 million units, reflecting a year-over-year (YoY) increase of 20.5%. However, from a quarter-over-quarter (QoQ) perspective, the market declined by 16.7%. The print market comprises inkjet printers, laser A3/A4 printers and copiers, serial dot matrix printers, and line printers.

The inkjet segment experienced YoY growth of 23.1% due to improved stock availability compared to the same period in the previous year. However, the segment witnessed a QoQ decline of 14.6% due to a temporary dip in demand from the consumer segment. Anticipating the festive period sale, market demand is expected to pick up in the third quarter of 2022, following decreased footfall in 2Q22 and summer vacations in schools and colleges.

The laser printers’ segment, including copiers, recorded a YoY growth of 19.6%, despite the challenges faced by vendors in terms of availability of popular entry-level models. The laser copier segment performed even better with a YoY growth of 82.0%. Demand from the government and banking sectors continued to contribute to this growth in 2Q22, and the market witnessed a revival of demand from large enterprises, which had been stalled since the COVID-19 pandemic.

Color laser copier shipments exceeded pre-COVID levels, capturing a market share of 15.1%, the second-highest in history. The introduction of new color models and the government’s increasing interest in color copiers supported this growth. In the laser printer segment, there was a gradual shift in market demand from 1-40 ppm to the 40+ ppm speed range. Vendors supplemented this shift with attractive schemes on high-speed printer-based color laser printers.

Overall, the print market in India showed positive growth in various segments, driven by factors such as improved stock availability, demand from the government and banking sectors, and the introduction of new color models.

Epson emerged as a dominant player in the inkjet printer market, securing a significant market share of 39.3% based on unit shipments. During the period under consideration, Epson shipped a total of 853,572 printers.

Epson’s success can be attributed to its range of EcoTank printers, which leverage heat-free technology. This revolutionary approach allows the printers to consume less power compared to laser printers, resulting in cost savings and environmental benefits. Epson introduced the concept of InkTank printing to the world in 2011, with the launch of the world’s first integrated Inktank system printers. In 2022, Epson EcoTank Printers completed 11 years in India. Over this period, Epson has sold more than 6 million EcoTank printers in India and a staggering 70 million printers worldwide.

HP Inc. (excluding Samsung) continued to dominate the overall Home and Office Printing (HCP) market, maintaining a leadership position with a substantial share of 43.8%. The company witnessed impressive year-over-year (YoY) shipment growth of 45.1%. The Inkjet segment played a significant role in this growth, with HP experiencing a remarkable YoY growth of 70.5%, allowing it to expand its market share to 37.3%. This growth can be attributed to the increased availability of HP’s ink tank models.

In the Laser segment, including the copier segment, HP achieved a solid growth of 26.8%. Notably, HP’s focus on the Laser copier segment resulted in a quarter-over-quarter (QoQ) growth of 5.3%, propelling the company to the third position. This growth was fueled by HP’s intensified efforts in targeting small and medium-sized businesses (SMBs) and corporate accounts.

Canon demonstrated a year-over-year (YoY) growth of 9.9% in the overall Home and Office Printing (HCP) market, securing the third position with a unit market share of 20.6%. In the inkjet segment, Canon experienced a notable YoY growth of 13.4%, driven by the increased availability of its single-function models.

In the laser segment, including laser copiers, Canon maintained its second position with a solid market share of 22.0% and achieved a YoY growth of 5.1%. The company’s remarkable growth of 82.3% YoY in the laser copier segment solidified its leadership position, capturing a significant market share of 35.9%. This growth was propelled by the introduction of new color models by Canon.

External storage

The India external storage market was valued at $2.2 billion in 2022. The market is expected to grow at a CAGR of 15% from 2022 to 2028, reaching a value of $4.7 billion by 2028. The global external storage market was valued at $35.5 billion in 2022. The market is expected to grow at a CAGR of 12.5% from 2022 to 2028, reaching a value of $75.1 billion by 2028.

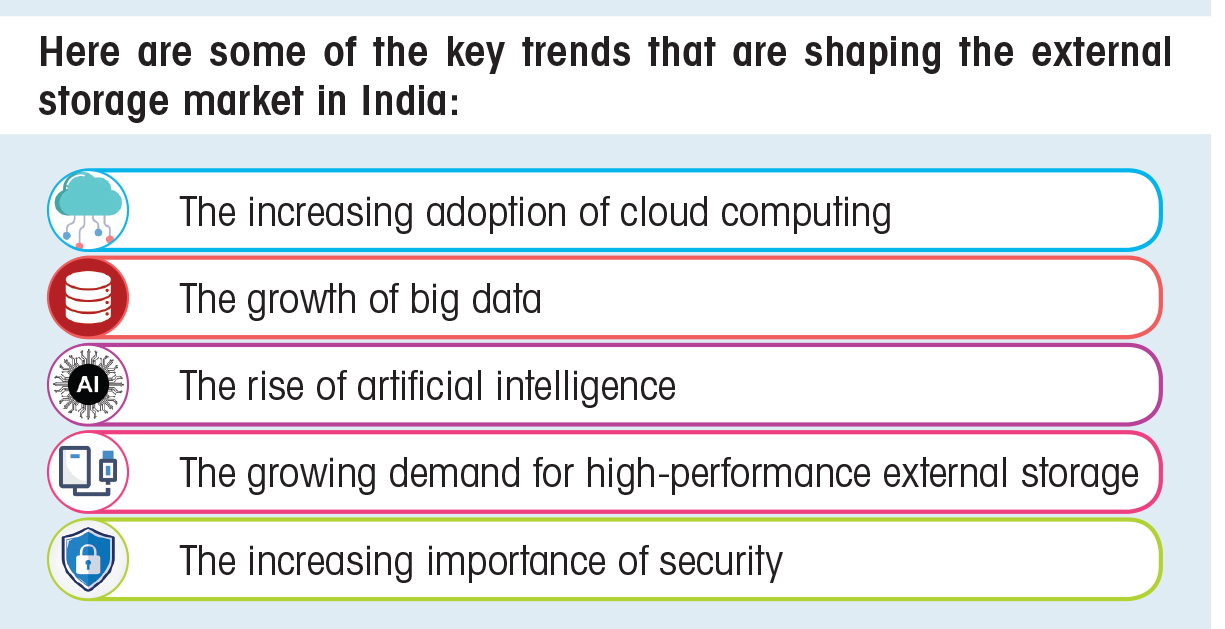

The growth is being driven by the increasing adoption of cloud computing, big data, and artificial intelligence.

Cloud computing is one of the major drivers of growth in the external storage market in India. The increasing adoption of cloud-based applications and services is driving demand for external storage to store data that is not being used on a regular basis. Big data is another major driver of growth in the external storage market. The increasing amount of data being generated by businesses and individuals is driving demand for external storage to store and process this data.

Artificial intelligence is also a major driver of growth in the external storage market. The increasing use of AI in applications such as fraud detection, image recognition, and natural language processing is driving demand for external storage with high processing power and memory.

The top three external storage vendors in India are Dell, HPE, and NetApp. These vendors are well-positioned to benefit from the growth of the external storage market in India due to their strong product portfolios and their established relationships with businesses in India.

The external storage market in India is expected to continue to grow in the coming years. The growth of cloud computing, big data, and artificial intelligence will continue to drive demand for external storage in India. The top three external storage vendors in India are well-positioned to benefit from this growth.

Server Business

The India server market, valued at USD 1602.97 million in 2022, is projected to reach USD 2416.68 million by 2028, growing at a CAGR of 7.19%. This estimation encompasses both hardware and operating systems used across different regions and end-user sectors in the country.

The demand for servers has increased in sectors such as healthcare, BFSI, education, and hospitality due to technological advancements and the need to manage and store data effectively. The Indian government has also prioritized projects related to the establishment of data centers (servers) in various states. For instance, the UP-Data Center Policy FY2021 aimed at attracting an investment of INR 20,000 Crores (USD 2.5 Billion) to develop a 250MW data center industry.

Cloud computing is one of the major drivers of growth in the server market in India. The increasing adoption of cloud-based applications and services is driving demand for servers to host these applications. Big data is another major driver of growth in the server market. The increasing amount of data being generated by businesses and individuals is driving demand for servers to store and process this data.

Businesses are increasingly adopting technologies like cloud computing, virtualization, and big data to cater to their digital transformation journey. To be able to run multiple workloads from the edge to the core to the cloud, they need to deploy advanced servers which can optimize AI/ML and IoT processes for them seamlessly. It is driving demand for servers with high processing power and memory.

The top three server vendors in India are Dell, HPE and IBM. These vendors are well-positioned to benefit from the growth of the server market in India due to their strong product portfolios and their established relationships with businesses in India.

Dell Technologies emerged as the leader in India’s x86 mainstream server market in 2022, according to IDC. The growth of Dell Technologies in India highlights the country’s importance as a key market, driven by businesses embracing a digital-first approach. Maintaining its No.1 position for the seventh consecutive quarter, Dell Technologies achieved the highest recorded revenue share of 48.6% since 2003 in the mainstream server segment.

The other prominent players in this space include Cisco Systems India, Lenovo (India) and Acer India.

Future Prospects and Challenges

Looking ahead, the IT hardware market in India is expected to continue its growth trajectory in the coming years. Factors such as increasing internet penetration, government initiatives, rising digital literacy, and the ongoing digital transformation across sectors will be the key drivers of the market’s expansion. The demand for laptops, tablets, and other portable devices is likely to remain strong as remote work and digital learning continue to be prevalent.

However, the industry also faces challenges. The global semiconductor shortage, which began in 2021, has affected the availability and pricing of IT hardware components, leading to supply chain disruptions. The industry needs to mitigate these challenges through proactive supply chain management and diversification of sourcing strategies.

Conclusion

The IT hardware market in India has witnessed substantial growth in FY22-23, driven by factors such as remote work and education, digital transformation initiatives, and government-led campaigns. The market is expected to continue expanding in the coming years, offering immense opportunities for the country and the technology companies. Overall, the IT hardware market in India is dynamic and competitive, with both domestic and international players vying for market share. The market is driven by technological advancements, digital transformation initiatives, and government support for domestic manufacturing.

Legal Battle Over IT Act Intensifies Amid Musk’s India Plans

The outcome of the legal dispute between X Corp and the Indian government c...

Wipro inks 10-year deal with Phoenix Group's ReAssure UK worth

The agreement, executed through Wipro and its 100% subsidiary,...

Centre announces that DPDP Rules nearing Finalisation by April

The government seeks to refine the rules for robust data protection, ensuri...

Home Ministry cracks down on PoS agents in digital arrest scam

Digital arrest scams are a growing cybercrime where victims are coerced or ...

Hrithik Roshan to endorse RuPay as Brand Ambassador

RuPay is reportedly planning to feature Bollywood superstar Hrithik Rosha

India Today Group launches – AI Pop Stars

Staying true to our industry leadership position in using cutting-edge tech

TelioLabs ropes in Phaniraj V A as the Group CEO

TelioLabs has announced the onboarding of Phaniraj V A as its new Group CE

Wipro Appoints Amit Kumar as Managing Partner and Global Head

Wipro Limited (NYSE: WIT, BSE: 507685, NSE: WIPRO), a leading technology s

Autodesk continually pushing the boundaries in the Design and

Autodesk’s vision is of a better world designed and made for all. It inte

In India, 88% of Indian business leaders are planning to inves

As we move through 2024, it has become increasingly clear that AI is not ju

MSI Announces the availability of RTX 50 series of laptops in

MSI, the innovative computing manufacturer in gaming, creator

goes on sale today, starting at Rs 19,999")

Nothing Phone (3a) goes on sale today, starting at Rs 19,999

The phone was launched on March 4, featuring a 50MP main, ultra-wide, and t

DATA SAFEGUARD INDIA PRIVATE LIMITED

EXATRON SERVERS MANUFACTURING PVT. LTD.

ACER INDIA PVT. LTD.

RELIANCE JIO INFOCOMM LTD.

Icons Of India : PRATIVA MOHAPATRA

Prativa is a transformational leader with an incredible breadth of exp...

Icons Of India : RAJENDRA SINGH PAWAR

Rajendra Singh Pawar is the Executive Chairman and Co-Founder of NIIT ...

ICONS OF INDIA : SUNIL VACHANI

Sunil Vachani is the Chairman of Dixon Technologies (India) Ltd. Under...

RailTel Corporation of India Limited

RailTel is a leading telecommunications infrastructure provider in Ind...

NSE - National Stock Exchange

NSE is the leading stock exchange in India....

CSC - Common Service Centres

CSC initiative in India is a strategic cornerstone of the Digital Indi...

Indian Tech Talent Excelling The Tech World - JAY CHAUDHRY, CEO – Zscaler

Jay Chaudhry, an Indian-American technology entrepreneur, is the CEO a...

Indian Tech Talent Excelling The Tech World - Aneel Bhusri, CEO, Workday

Aneel Bhusri, Co-Founder and Executive Chair at Workday, has been a le...

Indian Tech Talent Excelling The Tech World - Aman Bhutani, CEO, GoDaddy

Aman Bhutani, the self-taught techie and CEO of GoDaddy, oversees a co...

of images belongs to the respective copyright holders

of images belongs to the respective copyright holders