Indian Telecom Services Market: Continues to Shine!

By MYBRANDBOOK

India’s telecom sector achieved a significant milestone in FY23, with its revenues surpassing a remarkable Rs 3 lakh crore for the first time. This exceptional growth of 20% can be attributed to increased data and content consumption, as well as the government’s reform package providing financial relief to the industry. As a result, the government experienced a boost in earnings through the revenue share arrangement, collecting over Rs 167,000 crore in license fees.

Reliance Jio, the leading player, and Bharti Airtel, the second-ranked company, drove this growth by benefiting from tariff hikes and the growing utilization of data and other services by consumers.

However, Vodafone Idea, the country’s third-largest private telecom provider, is still striving to turn things around, especially since the government became its largest shareholder by converting outstanding liabilities into equity.

State-owned BSNL and MTNL have also faced their fair share of challenges in their revival efforts. Nonetheless, the government’s comprehensive revival packages and the voluntary retirement scheme (VRS) have been instrumental in improving the financial positions and operations of these companies.

The telecom industry’s remarkable revival indicates that the government’s reforms have been effective. Furthermore, the upcoming 5G rollout by mobile operators, coupled with increased investments in network expansion, will inject fresh momentum into the industry and further bolster its revenues in the years to come.

The telecom relief package introduced in September 2021, under the leadership of Ashwini Vaishnaw, the communications minister, has been a key factor in empowering the industry with financial stability.

The government provided telecom companies with the option of a four-year moratorium on spectrum holdings, extending it from 20 to 30 years, and eliminated spectrum usage charges for recently auctioned airwaves.

The surge in gross revenues also had a similar impact on the adjusted gross revenues of the industry, which determines the levies charged by the government.

Both the government and mobile operators are optimistic about the continued growth of revenues, driven by the nationwide rollout of 5G and increased user engagement.

The positive effects of higher usage are already evident, as the average revenue per user (ARPU) has continued to rise following tariff increases for both postpaid and prepaid subscribers. For instance, Jio’s ARPU increased from Rs 167.6 in March 2022 to Rs 178.8 in March 2023.

The Indian telecom services market is expected to grow at a compound annual growth rate (CAGR) of 11.5% from FY22 to FY23. The market is driven by the increasing adoption of smartphones and data-intensive applications, such as video streaming and gaming.

Broadband subscriber base

In March 2023, the total number of broadband subscribers in India witnessed growth, reaching 846.57 million, compared to 839.33 million in February 2023. This represented a monthly growth rate of 0.86%.

The top five service providers accounted for a significant market share of 98.37% of the total broadband subscribers by the end of March 2023. These leading providers were as follows: Reliance Jio Infocomm Ltd with 438.56 million subscribers, Bharti Airtel with 241.90 million subscribers, Vodafone Idea with 124.83 million subscribers, BSNL with 25.37 million subscribers, and Atria Convergence with 2.14 million subscribers.

Regarding wired broadband services as of March 31, 2023, the top five service providers were Reliance Jio Infocomm Ltd with 8.33 million subscribers, Bharti Airtel with 6.12 million subscribers, BSNL with 3.60 million subscribers, Atria Convergence Technologies with 2.14 million subscribers, and Hathway Cable & Datacom with 1.12 million subscribers.

For wireless broadband services as of March 31, 2023, the top five service providers were Reliance Jio Infocomm Ltd with 430.23 million subscribers, Bharti Airtel with 235.78 million subscribers, Vodafone Idea with 124.82 million subscribers, BSNL with 21.77 million subscribers, and Intech Online Pvt. Ltd. with 0.23 million subscribers.

Wireline subscriber base

Wireline subscriber base

In March 2023, the number of wireline subscribers in India experienced growth, rising from 27.97 million in February 2023 to 28.41 million. This resulted in a net increase of 0.44 million subscribers, reflecting a monthly growth rate of 1.58%.

At the end of March 2023, the distribution of wireline subscribers between urban and rural areas was as follows: urban subscribers accounted for 92.09% of the total, while rural subscribers constituted 7.91%.

The overall wireline tele-density in India also saw an increase, climbing from 2.02% in February 2023 to 2.05% in March 2023. During the same period, urban wireline tele-density stood at 5.36%, while rural wireline tele-density reached 0.25%.

Among the wireline service providers, BSNL and MTNL, the two public sector access service providers, held a combined market share of 33.15% as of March 31, 2023.

Wireless subscriber

During March 2023, the total number of wireless subscribers in India witnessed a slight increase, reaching 1,143.93 million compared to 1,141.96 million in February 2023. This represented a monthly growth rate of 0.17%. In urban areas, wireless subscriptions rose from 626.37 million to 627.54 million, while in rural areas, they increased from 515.60 million to 516.38 million. The monthly growth rates for urban and rural wireless subscriptions were 0.19% and 0.15% respectively.

The wireless tele-density in India also experienced a slight rise, moving from 82.38% in February 2023 to 82.46% in March 2023. Urban wireless tele-density increased from 128.41% to 128.45%, while rural tele-density increased from 57.39% to 57.46% during the same period. At the end of March 2023, urban wireless subscribers accounted for 54.86% of the total, while rural wireless subscribers constituted 45.14%.

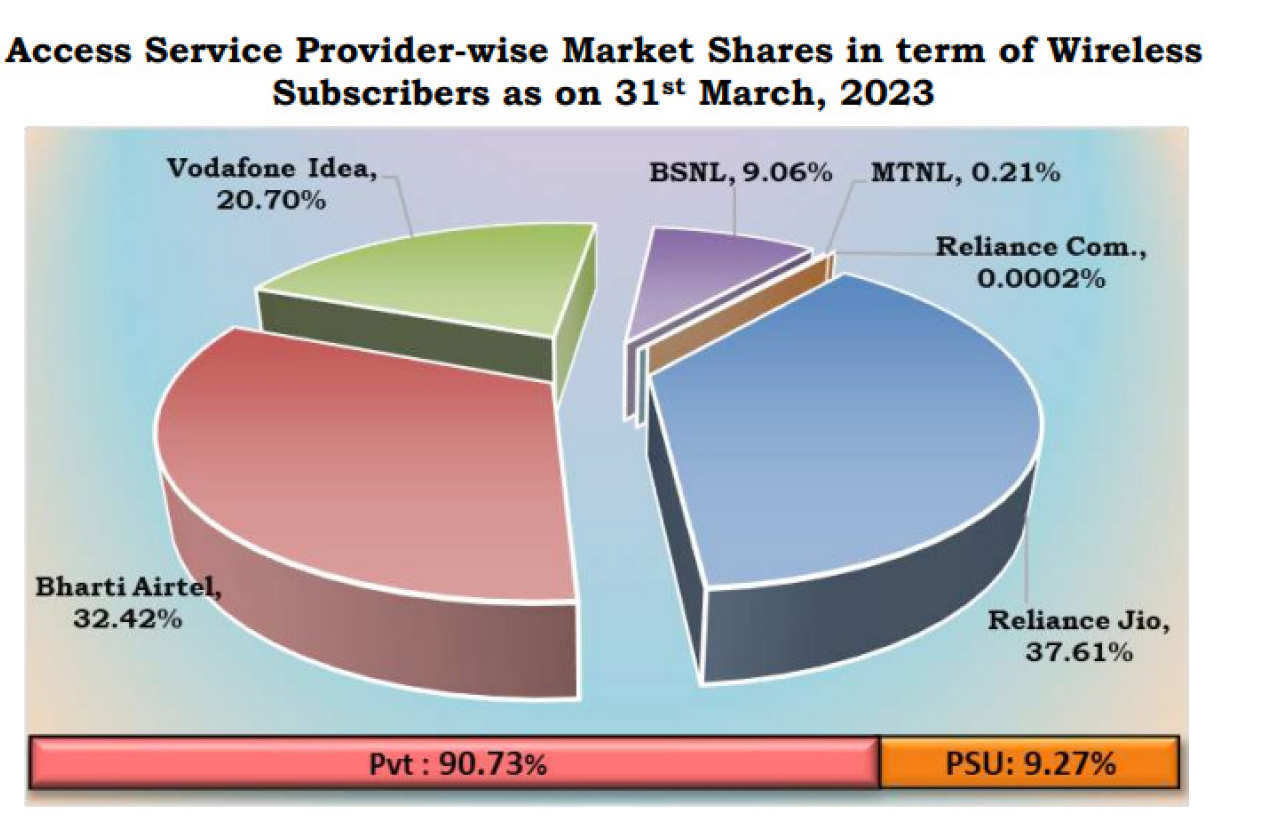

As of March 31, 2023, private access service providers held a dominant market share of 90.73% among wireless subscribers, whereas BSNL and MTNL, the two public sector access service providers, had a market share of only 9.27%.

Total Telephone Subscribers

In March 2023, the total number of telephone subscribers in India witnessed an increase, reaching 1,172.84 million compared to 1,169.93 million in February 2023. This represented a monthly growth rate of 0.21%.

Urban telephone subscriptions rose from 652.16 million to 653.71 million, while rural subscriptions increased from 517.77 million to 518.63 million during the same period. The monthly growth rates for urban and rural telephone subscriptions were 0.24% and 0.17% respectively in March 2023.

The overall tele-density in India also saw a slight increase, moving from 84.40% in February 2023 to 84.51% in March 2023. Urban tele-density increased from 133.70% to 133.81%, while rural tele-density increased from 57.63% to 57.71% during the same period. At the end of March 2023, urban telephone subscribers accounted for 55.76% of the total, while rural subscribers constituted 44.24%.

Trends

The Indian telecom services market is witnessing a number of trends, including:

The increasing adoption of smartphones: The number of smartphone users in India is expected to reach 500 million by FY23. This will drive the demand for data-intensive services, such as video streaming and gaming.

The growth of the Internet of Things (IoT): The IoT is expected to connect billions of devices in India by FY23. This will create new opportunities for telecom service providers to offer data and connectivity services to businesses and consumers.

The rise of cloud computing: Cloud computing is becoming increasingly popular in India. This is driving the demand for high-speed data connectivity and storage services from telecom service providers.

Challenges

The Indian telecom services market is facing a number of challenges, including:

The high cost of spectrum: The government’s auction of spectrum is often criticized for being too expensive. This is a major challenge for telecom service providers, as it limits their ability to invest in new networks and services.

The low ARPU (average revenue per user): The ARPU in India is one of the lowest in the world. This is a challenge for telecom service providers, as it makes it difficult to generate enough revenue to cover their costs and invest in new networks and services.

The high level of competition: The Indian telecom services market is highly competitive. This is a challenge for telecom service providers, as they need to constantly innovate and offer new services to stay ahead of the competition.

Government Push

In the Union Budget 2023-24, the Department of Telecommunications was allocated a budget of Rs. 97,579.05 crore (US$ 11.92 billion). This allocation includes Rs. 400 crore (US$ 48.88 million) for Research and Development and Rs. 5,000 crore (US$ 611.1 million) for Bharatnet.

RailTel, a mini Ratna PSU, launched the Prime Minister Wi-Fi Access Network Interface (PM-WANI), providing public WiFi services across 100 railway stations. This initiative encompasses 2,384 WiFi hotspots spread across 22 states.

The Universal Service Obligation Fund (USOF) officially introduced the Telecom Technology Development Fund (TTDF) Scheme on October 1st, 2022.

The government intends to update the existing regulatory framework with the Indian Telecommunication Bill, 2022.

As of July 2022, a total of 5,84,747 km of Open Fiber Control (OFC) has been laid, connecting 1,87,245 Gram Panchayats. In 1,81,888 of these Gram Panchayats, the service is ready for deployment through fiber and satellite connectivity.

Prime Minister Mr. Narendra Modi inaugurated 5G services on October 1, 2022, marking a significant milestone in the country’s telecommunications sector.

In December 2022, the Production-linked Incentive (PLI) Scheme approved investments of US$ 502.95 million (Rs. 4,115 crore) from 42 companies. This includes 28 MSMEs and 14 Non-MSMEs, consisting of eight domestic and seven global companies.

The implementation of dedicated government schemes such as the BharatNet Project Scheme, Telecom Development Plan, Aspirational District Scheme, and Comprehensive Telecom Development Plan (CTDP) in the North-Eastern Region has resulted in a remarkable 200% increase in rural internet subscriptions between 2015 and 2021.

To foster the development of 6G technology, the Department of Telecommunications (DoT) has established a dedicated innovation group for sixth-generation (6G) research and advancement.

Conclusion

While the Indian telecom services market continues to face challenges such as the high cost of spectrum, low ARPU, and intense competition, it remains a dynamic and growing industry. With the increasing adoption of smartphones, data-intensive applications, and the Internet of Things, the market is poised for continued growth. The government’s reforms, along with the upcoming rollout of 5G and investments in network expansion, provide a positive outlook for the industry’s future. As the sector evolves and innovates, it holds the potential to transform connectivity and communication in India, driving progress and empowering millions of individuals and businesses across the country.

Elon Musk's xAI is looking for Hindi-speaking 'AI tutors'

Tech billionaire Elon Musk's AI venture, xAI, is in search of AI tutors ...

Ericsson steps up focus on R&D in India

Ericsson (NASDAQ: ERIC) today announced that it is stepping up its focus o...

Rubrik Unveils Data Security Posture Management for Microsoft

With Rubrik DSPM, organizations can confidently navigate the growing demand...

Apple eyeing the smart home domain with new devices and 'homeO

Apple is also looking at developing a new operating system likely called ho...

Remo D'Souza and Wife Booked for Fraud

A most popular Indian Choreographer Remo D'Souza, his wife Lizelle, and f

Salman Khan Receives Death Threat: ₹5 Crore Demanded to End

The message reportedly stated, "If Salman Khan wants to stay alive and end

Infopercept names Jhilmil Kochar as the Board’s Strategic Ad

Managed security services company, Infopercept Consulting has announced t

Akriti Chopra, co-founder & CPO Zomato resigns

Online food delivery platform Zomato Ltd announced the resignation of it

AMD Pensando driving innovation in the DPU architecture space

AMD Pensando stands out in the DPU (Data Processing Unit) market with its u

Alpha Max offers high end solutions in the network space to en

The vision at Alpha Max is to attain quality as the trademark and create a

Dassault Systèmes Boosts Axldrone's Efficiency

Dassault Systèmes (Euronext Paris: FR0014003TT8, DSY.PA) today announced

HPE Unveils New Solutions to Boost AI Model Training

Hewlett Packard Enterprise (NYSE: HPE) today announced the HPE ProLiant Co

FIRE BOLTT

LUMINOUS POWER TECHNOLOGIES PVT. LTD.

BHARAT ELECTRONICS LTD.

HAVELLS INDIA LTD.

Icons Of India : AALOK KUMAR

Aalok Kumar is celebrated as a global leader and recipient of the Peop...

ICONS OF INDIA : VIJAY SHEKHAR SHARMA

Vijay Shekhar Sharma is an Indian technology entrepreneur and multimil...

Icons Of India : B.V.R. Subrahmanyam

A 1987 batch (Chhattisgarh cadre) Indian Administrative Service Office...

GSTN - Goods and Services Tax Network

GSTN provides shared IT infrastructure and service to both central and...

RailTel Corporation of India Limited

RailTel is a leading telecommunications infrastructure provider in Ind...

HPCL - Hindustan Petroleum Corporation Ltd.

HPCL is an integrated oil and gas company involved in refining, market...

Indian Tech Talent Excelling The Tech World - Shantanu Narayen, CEO- Adobe Systems Incorporated

Shantanu Narayen, CEO of Adobe Systems Incorporated, is renowned for h...

Indian Tech Talent Excelling The Tech World - JAY CHAUDHRY, CEO – Zscaler

Jay Chaudhry, an Indian-American technology entrepreneur, is the CEO a...

Indian Tech Talent Excelling The Tech World - Thomas Kurian, CEO- Google Cloud

Thomas Kurian, the CEO of Google Cloud, has been instrumental in expan...