With an ever increasing telecom user-base and growing demand for data-based services, India Inc. is eagerly waiting to leverage the power of 5G

By MYBRANDBOOK

For decades, telecom has been the poster boy of Indian business success stories. The industry that has brought many firsts to the country is now the world’s second largest market in terms of subscriber base with 1.16 billion users. The country that was among the fastest in the world to rollout 4G services across its geography is now eagerly awaiting the launch of 5G services. Higher multi-Gbps speeds, lower latency, and more reliability compared to the previous-generation mobile networks are some of the benefits of 5G. As per DoT, India can expect the launch of 5G services within this year.

Market size

India is the world’s second-largest telecommunications market. The total subscriber base, wireless subscriptions as well as wired broadband subscriptions have grown consistently. Tele-density stood at 85.91%, as of December 2021, total broadband subscriptions grew to 792.1 million until December 2021 and total subscriber base stood at 1.18 billion in December 2021.

Gross revenue of the telecom sector stood at Rs. 64,801 crore (US$ 8.74 billion) by end of March, 2022. The total wireless data usage in India grew 16.54% quarterly to reach 32,397 PB in the first quarter of FY22. The contribution of 3G and 4G data usage to the total volume of wireless data usage was 1.78% and 97.74%, respectively, in the third quarter of FY21. Share of 2G data usage stood at 0.48% in the same quarter.

Telecom subscriber base

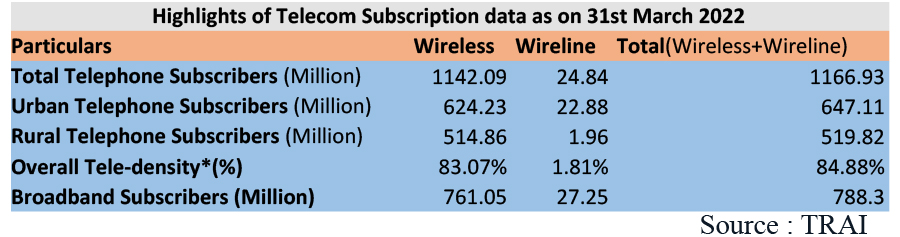

The total number of telephone subscribers in India was 1,166.93 million at the end of March-22. Urban telephone subscription decreased from 647.76 million at the end of February-22 to 647.11 million at the end of March-22 and the rural subscription also increased from 518.29 million to 519.82 million during the same period. The monthly growth rates of urban and rural telephone subscription were -0.10% and 0.30% respectively during the month of March-22. At the end of the year, the tele-density of India was 84.88%. The urban tele-density was 134.94% whereas the rural tele-density was 58.07%.

Wireless subscriber

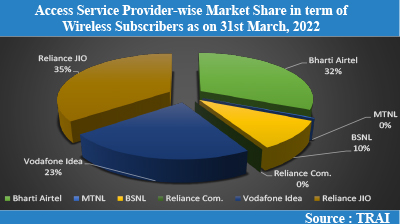

Total wireless subscribers increased from 1,141.53 million at the end of February-22 to 1,142.09 million at the end of March-22, thereby registering a monthly growth rate of 0.05%. Wireless subscription in urban areas decreased from 625.19 million at the end of February-22 to 624.23 million at the end of March-22 however wireless subscription in rural areas increased from 516.34 million to 517.86 million during the same period. Monthly growth rates of urban and rural wireless subscription were -0.15% and 0.29% respectively Of the total wireless subscriber base, the private players command a market size of 89.76% whereas the public operators hold a market size of 10.24%. Among the operators, Reliance Jio dominated the wireless subscriber user-base with 35.37% market share and is followed by Bharti Airtel with 31.55%. Vodafone-Idea or Vi is at 3rd position with 22.83% market share.

Total wireless subscribers increased from 1,141.53 million at the end of February-22 to 1,142.09 million at the end of March-22, thereby registering a monthly growth rate of 0.05%. Wireless subscription in urban areas decreased from 625.19 million at the end of February-22 to 624.23 million at the end of March-22 however wireless subscription in rural areas increased from 516.34 million to 517.86 million during the same period. Monthly growth rates of urban and rural wireless subscription were -0.15% and 0.29% respectively Of the total wireless subscriber base, the private players command a market size of 89.76% whereas the public operators hold a market size of 10.24%. Among the operators, Reliance Jio dominated the wireless subscriber user-base with 35.37% market share and is followed by Bharti Airtel with 31.55%. Vodafone-Idea or Vi is at 3rd position with 22.83% market share.

Wireline subscribers

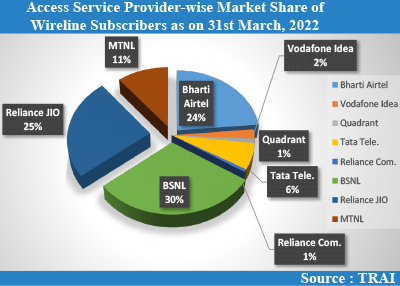

Wireline subscribers increased from 24.52 million at the end of February-22 to 24.84 million at the end of March-22. Net increase in the wireline subscriber base was 0.32 million with a monthly growth rate of 1.31%. The share of urban and rural subscribers in total wireline subscribers were 92.12% and 7.88% respectively at the end of March, 2022. Among the operators, BSNL has the majority market share of 30.23% of all wireline subscriber base and is closely followed by Reliance Jio with 24.85%. Airtel is 3rd position with 3.55% market share and the other state-run operator MTNL has a market share of 10.84% at the end of March 2022.

Wireline subscribers increased from 24.52 million at the end of February-22 to 24.84 million at the end of March-22. Net increase in the wireline subscriber base was 0.32 million with a monthly growth rate of 1.31%. The share of urban and rural subscribers in total wireline subscribers were 92.12% and 7.88% respectively at the end of March, 2022. Among the operators, BSNL has the majority market share of 30.23% of all wireline subscriber base and is closely followed by Reliance Jio with 24.85%. Airtel is 3rd position with 3.55% market share and the other state-run operator MTNL has a market share of 10.84% at the end of March 2022.

Broadband

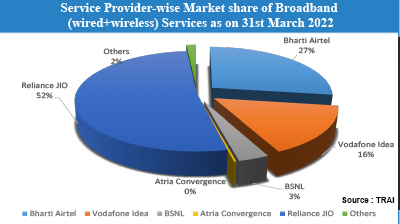

The total broadband subscriber base at the end of the fiscal year 22 was 788.3 million as against 765 million by the same period a year ago. There are a total of 653 broadband operators in the country though the space is primarily occupied by four major players. Reliance Jio holds the lion’s share of 51.92% in the broadband market whereas the closest follower Airtel is with 27.31% market share followed by Vodafone Idea with 15.54% market share. PSU operator BNL holds a market share of 3.45%.

The total broadband subscriber base at the end of the fiscal year 22 was 788.3 million as against 765 million by the same period a year ago. There are a total of 653 broadband operators in the country though the space is primarily occupied by four major players. Reliance Jio holds the lion’s share of 51.92% in the broadband market whereas the closest follower Airtel is with 27.31% market share followed by Vodafone Idea with 15.54% market share. PSU operator BNL holds a market share of 3.45%.

Highlights of FY2021

With daily increasing subscriber base, there have been a lot of investment and development in the sector. FDI inflow in the telecom sector stood at US$ 38.25 billion between April 2000-December 2021.

Some of the major developments in the recent past are:

Govt. initiatives

The Government has fast-tracked reforms in the telecom sector and continues to be proactive in providing room for growth for telecom companies. Some of the key initiatives taken by the Government are as follows:

Outlook

The future of Indian telecom looks rosy from both consumers as well as service providers’ perspective though network connectivity still remains a big issue. India is consistently growing in terms of subscriber addition and is among the biggest consumer of data worldwide with over 11 GB data consumption per month. It is expected that, over the next five years, rise in mobile-phone penetration and decline in data costs will add 500 million new internet users in India, creating opportunities for new businesses. While all this data refers to the opportunities with 4G, the horizon is expected to be much wider once 5G is rolled out in the country.

According to reports, India will have 350 million 5G subscribers by 2026 accounting for 27% of all mobile subscribers. By 2025, India will need approximately 22 million skilled workers in 5G-centric technologies such as Internet of Things (IoT), Artificial Intelligence (AI), robotics and cloud computing.

Legal Battle Over IT Act Intensifies Amid Musk’s India Plans

The outcome of the legal dispute between X Corp and the Indian government c...

Wipro inks 10-year deal with Phoenix Group's ReAssure UK worth

The agreement, executed through Wipro and its 100% subsidiary,...

Centre announces that DPDP Rules nearing Finalisation by April

The government seeks to refine the rules for robust data protection, ensuri...

Home Ministry cracks down on PoS agents in digital arrest scam

Digital arrest scams are a growing cybercrime where victims are coerced or ...

Hrithik Roshan to endorse RuPay as Brand Ambassador

RuPay is reportedly planning to feature Bollywood superstar Hrithik Rosha

India Today Group launches – AI Pop Stars

Staying true to our industry leadership position in using cutting-edge tech

TelioLabs ropes in Phaniraj V A as the Group CEO

TelioLabs has announced the onboarding of Phaniraj V A as its new Group CE

Wipro Appoints Amit Kumar as Managing Partner and Global Head

Wipro Limited (NYSE: WIT, BSE: 507685, NSE: WIPRO), a leading technology s

AMD Pensando driving innovation in the DPU architecture space

AMD Pensando stands out in the DPU (Data Processing Unit) market with its u

Acer addresses evolving customer needs by consistently pushing

Acer offers a comprehensive range of products under one roof, including des

MSI Announces the availability of RTX 50 series of laptops in

MSI, the innovative computing manufacturer in gaming, creator

goes on sale today, starting at Rs 19,999")

Nothing Phone (3a) goes on sale today, starting at Rs 19,999

The phone was launched on March 4, featuring a 50MP main, ultra-wide, and t

AMARA RAJA POWER SYSTEMS LTD.

SAMRIDDHI AUTOMATIONS PVT. LTD.

DATA SAFEGUARD INDIA PRIVATE LIMITED

WIPRO LTD.

ICONS OF INDIA : SANJAY NAYAR

Sanjay Nayar is a senior finance professional in the Indian private in...

Icons Of India : MUKESH D. AMBANI

Mukesh Dhirubhai Ambani is an Indian businessman and the chairman and ...

ICONS OF INDIA : RITESH AGARWAL

Ritesh Agarwal is an Indian billionaire entrepreneur and the founder a...

PFC - Power Finance Corporation Ltd

PFC is a leading financial institution in India specializing in power ...

GeM - Government e Marketplace

GeM is to facilitate the procurement of goods and services by various ...

ECIL - Electronics Corporation of India Limited

ECIL is distinguished by its diverse technological capabilities and it...

Indian Tech Talent Excelling The Tech World - AJAY BANGA, President - World Bank

Ajay Banga is an Indian-born American business executive who currently...

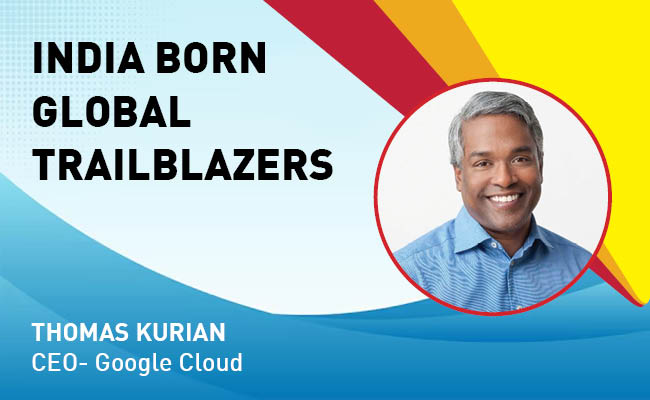

Indian Tech Talent Excelling The Tech World - Thomas Kurian, CEO- Google Cloud

Thomas Kurian, the CEO of Google Cloud, has been instrumental in expan...

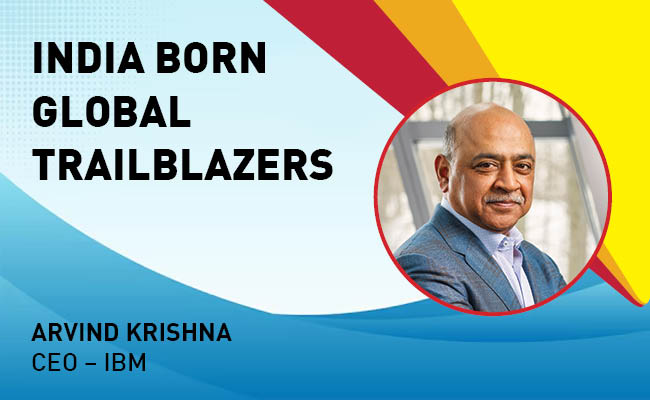

Indian Tech Talent Excelling The Tech World - ARVIND KRISHNA, CEO – IBM

Arvind Krishna, an Indian-American business executive, serves as the C...

of images belongs to the respective copyright holders

of images belongs to the respective copyright holders