Banks' Endeavour to Buyout NBFCs' Loan Book is Synergetic

By MYBRANDBOOK

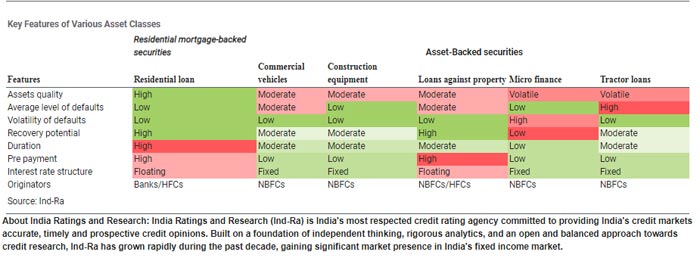

India Ratings and Research (Ind-Ra) believes that the steps taken by Reserve Bank of India (RBI) to support systemic liquidity and State Bank of India (SBI; IND AAA/Stable) to offer balance sheet liquidity for non-banking financial companies (NBFCs) would help alleviate some of the ongoing tightness in the financial system. These measures however are likely to bring about a temporary effect. For long-term sustainability, restoration of normalcy in the credit market especially for NBFCs is critical. Additionally, development of alternative sources of financing such as an active securitisation market would be beneficial.

Actions to Complement System and Balance-sheet Liquidity:The RBI has recently infused INR320 billion of durable liquidity into the system and another INR240 billion is likely to come in the month of October 2018 through open market operations. In addition, to tide over frictional liquidity mismatches, banks are now permitted to reckon SLR securities held by them up to another 2% of their net demand and time liabilities, under the facility to avail liquidity for liquidity coverage ratio within the mandatory SLR requirement. Ind-Ra believes this will help in stabilising the systemic liquidity, especially in light of possible draining of liquidity in the upcoming festive session. SBI has announced an additional INR300 billion asset buyout from NBFCs, which would help them tide over the ongoing challenges.

Potential Source of Liquidity for NBFCs: Ind-Ra has analysed the top eight housing finance companies (HFCs; excluding HDFC Ltd and LIC Housing Finance Limited) and the top 10 non-infrastructure NBFCs. Of the total, 16 entities (are among the largest NBFCs) have about INR5 trillion exposures to asset classes that are preferred (most common are microfinance, commercial vehicles, housing loans etc) for assignment or securitisation. According to the announcement by SBI, it is expected to purchase over INR450 billion (about three times of normal buyouts) of assets from NBFCs over FY19 to create additional source of liquidity for non-banks. Some of the well-capitalised banks, many of which are approaching their sectoral cap on NBFCs, may also expand their buyouts of assets as an alternative to expand funding to non-banks.

Banks can Cherry Pick Assets: As opposed to the asset classes which are typically securitised or assigned, originating granular housing loans, commercial vehicle loans and other such asset classes involves significant operating costs and banks may not have the adequate network to originate them or assess credit quality on a large scale. In the current environment, banks could cherry pick assets from NBFCs and price them well instead of originating them, thus avoiding scope for early delinquencies. This proposition is likely to result in better RoAs for banks on both priority sector lending qualifying assets and others that are securitised / assigned.

Ind-Ra also expects other banks (including private banks) with adequate capital buffers to use a similar strategy to cherry pick assets from NBFCs. Additionally, exposure to these assets does not amount to exposure to NBFCs’ balance sheet and hence this route partly addresses the perceived risk aversion. NBFCs will see some relief on the perception of inadequate liquidity over 3QFY19 and the securitisation push would be conducive for matching assets with liabilities. This is also an opportunity for NBFCs to reduce dependence on short-term funding, as they take some assets off the balance sheet.

Decelerating Credit Flows from Non-Banks: The recent data from mutual funds suggest that there has been a considerable drop in assets under management under liquidity fund in September (part of which is seasonal), after a sudden rise in August. Asset management companies have been the largest subscribers of money market instruments and have been instrumental for the surge in NBFCs’ business in the last few years. Overall, incremental inflows into debt funds have decelerated and therefore supply funding could be restricted. This scenario could not only impinge NBFCs’ growth but also pose refinancing challenges, especially for the newer and weaker NBFCs. In these circumstances, monetisation of assets through securitisation to address short-term financing requirements could be beneficial. The current situation also strengthens the necessity of developing a securitisation market for stakeholders to ensure a sustainable funding option along with traditional sources.

Legal Battle Over IT Act Intensifies Amid Musk’s India Plans

The outcome of the legal dispute between X Corp and the Indian government c...

Wipro inks 10-year deal with Phoenix Group's ReAssure UK worth

The agreement, executed through Wipro and its 100% subsidiary,...

Centre announces that DPDP Rules nearing Finalisation by April

The government seeks to refine the rules for robust data protection, ensuri...

Home Ministry cracks down on PoS agents in digital arrest scam

Digital arrest scams are a growing cybercrime where victims are coerced or ...

Hrithik Roshan to endorse RuPay as Brand Ambassador

RuPay is reportedly planning to feature Bollywood superstar Hrithik Rosha

India Today Group launches – AI Pop Stars

Staying true to our industry leadership position in using cutting-edge tech

TelioLabs ropes in Phaniraj V A as the Group CEO

TelioLabs has announced the onboarding of Phaniraj V A as its new Group CE

Wipro Appoints Amit Kumar as Managing Partner and Global Head

Wipro Limited (NYSE: WIT, BSE: 507685, NSE: WIPRO), a leading technology s

Delivering Critical Business Communication Solutions to Enterp

Arya Omnitalk and Syntel’s comprehensive suite of solutions and more than

In India, 88% of Indian business leaders are planning to inves

As we move through 2024, it has become increasingly clear that AI is not ju

MSI Announces the availability of RTX 50 series of laptops in

MSI, the innovative computing manufacturer in gaming, creator

goes on sale today, starting at Rs 19,999")

Nothing Phone (3a) goes on sale today, starting at Rs 19,999

The phone was launched on March 4, featuring a 50MP main, ultra-wide, and t

LAVA INTERNATIONAL LTD.

RELIANCE JIO INFOCOMM LTD.

SAMRIDDHI AUTOMATIONS PVT. LTD.

NUMERIC INDIA, A Group Brand Legrand

ICONS OF INDIA : VINAY SINHA

Vinay Sinha is the Managing Director of Sales for the India Mega Regio...

Icons Of India : Arjun Malhotra

Arjun Malhotra, the Chairman of Magic Software Inc., is widely recogni...

Icons Of India : Deepak Sharma

Deepak Sharma spearheads Schneider Electric India. He brings with him ...

CSC - Common Service Centres

CSC initiative in India is a strategic cornerstone of the Digital Indi...

DRDO - Defence Research and Development Organisation

DRDO responsible for the development of technology for use by the mili...

IFFCO - Indian Farmers Fertiliser Cooperative

IFFCO operates as a cooperative society owned and controlled by its fa...

Indian Tech Talent Excelling The Tech World - Anirudh Devgan , President, Cadence Design

Anirudh Devgan, the Global President and CEO of Cadence Design Systems...

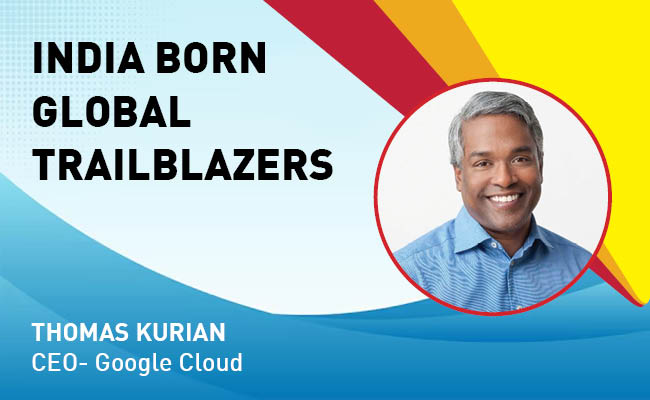

Indian Tech Talent Excelling The Tech World - Thomas Kurian, CEO- Google Cloud

Thomas Kurian, the CEO of Google Cloud, has been instrumental in expan...

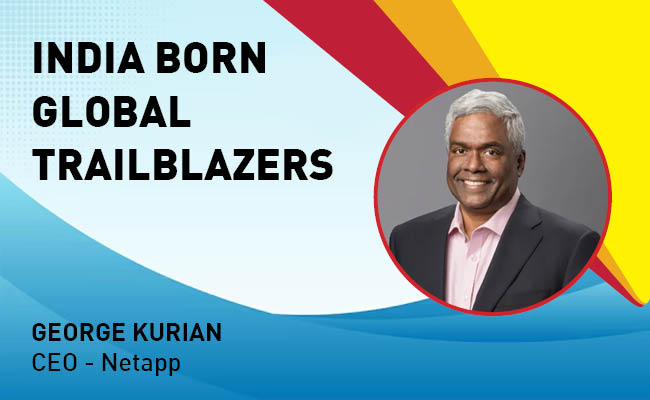

Indian Tech Talent Excelling The Tech World - George Kurian, CEO, Netapp

George Kurian, the CEO of global data storage and management services ...

of images belongs to the respective copyright holders

of images belongs to the respective copyright holders