Multiple factors including post-pandemic euphoria, easy finance, discounts and promotions as well as 5G make 2021 among the top performing years for the Indian smartphone industry

By MYBRANDBOOK

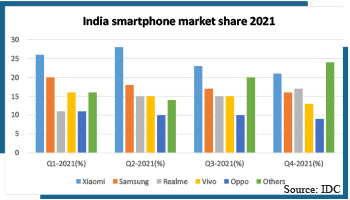

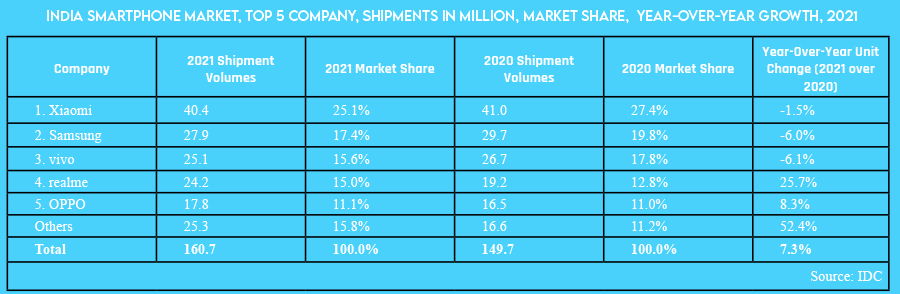

India’s smartphone shipments grew 11% YoY to reach 169 million units in 2021, according to the latest research from Counterpoint Reasearch. 2021 started strong with pent-up demand from 2H20 (Jul- Dec) and positive sentiments around vaccinations but a severe second wave of Covid-19 dealt a blow to the growth. However, the shipments declined 8% YoY in the December quarter due to supply issues plaguing the smartphone manufacturing ecosystem.

Constrained supplies resulted in low inventories across channels in the second half of the year, which usually has a high demand during the festive season.

Trends

Commenting on the market dynamics, Senior Research Analyst Prachir Singh said, “The Indian smartphone market witnessed high consumer demand in 2021, making it the best-performing year. This feat came in a year that witnessed supply constraints due to a multitude of reasons – a second and more virulent COVID-19 wave, global component shortages and price hikes due to these shortages. The high replacement demand fueled by increasing smartphone affordability in the mid and high-price tiers due to promotions and discounts, as well as better financing options, led to an 11% YoY growth in 2021. The demand outstripped the supply in the last two quarters of 2021. During Q4 2021, the smartphone market declined 8% YoY. We expect the supply situation to get better going forward and reach normalcy by the end of Q1 2022.”

Commenting on the competitive landscape and pricing, Counterpoint Research Analyst said, “India’s smartphone market retail ASP (average selling price) grew 14% YoY in 2021 to reach its highest ever at $227. The price hikes in the budget segment due to component price rise, increasing focus of OEMs on the premium segment, and increased demand for mid-range and premium smartphones due to increasing uses and availability of financing options contributed to the increasing ASP. This resulted in the Indian smartphone market revenue crossing $38 billion in 2021, registering a growth of 27% YoY.”

Besides, on the manufacturing front, local manufacturing bounced back, contributing 98% shipments in 2021, compared to 90% in 2020. The PLI scheme has been a great booster for the Indian mobile manufacturing ecosystem, attracting top players like Apple and Samsung to increase their ‘Make in India’ footprint and make India their export hub. Therefore, handset exports saw 26% YoY growth in 2021. Seeing the PLI scheme’s success in the mobile manufacturing ecosystem, the government has launched similar schemes for different product verticals like CIOT and IT hardware.

India’s overall mobile handset market grew 7% YoY in 2021. Samsung captured the top position in the handset market in 2021, taking 17% share. Feature phone shipments reached 86 million units to show flat growth in 2021. itel led the feature phone market, taking 24% share followed by Lava, Samsung and Jio. itel has been leading the feature phone market for the last two consecutive years.

Market analysis

Xiaomi maintained the top position in India’s smartphone market in 2021 with 2% YoY growth. Component shortage in the second half of the year, which affected volumes in the mass market segment, led to slower growth.Xiaomi grew 258% in the premium segment (>INR 30,000, ~$400) in 2021 with the Mi 11x series. Going forward, it will keep focusing on the premium segment and offline expansion.

Samsung remained at the second position in 2021 with an 8% YoY decline in shipments. Supply chain disruptions, absence of new Note series, reduced focus on the entry-level segment and fewer launches in the mid segment compared to the previous year led to an overall decline. However, Samsung was the top brand in 5G smartphone shipments in Q4 2021. Its campaign on providing maximum bands in 5G smartphones facilitated this growth. It also led the INR 20,000-INR 45,000 (~$267-$600) segment with a 28% share. Samsung’s foldable device (Fold and Flip series) shipments grew 388% YoY in 2021.

Among the top five brands, realme was the fastest growing in 2021 with 20% YoY growth. It also captured the second spot in Q4 2021 for the first time ever. Switching to ‘Unisoc’ to manage component shortages, production expansion through partnerships with EMS, focus on the premium segment with newly launched ‘GT series’ and high demand for its revamped C series and Narzo series favored this high growth for realme. Going forward, realme is aiming to provide 5G in all smartphones priced above Rs 15000. It also plans to enter the ultra-premium segment.

vivo emerged as the top 5G smartphone brand in 2021 with a 19% share. It grew 2% YoY in 2021 driven by a strong performance of its Y series and V It remains the leading player in the offline segment while simultaneously strengthening its hold in the online segment through its sub-brand iQOO.

OPPO held the fifth position in 2021 with 6% YoY growth. It now has a leaner portfolio in the budget segment as it is focusing on the upper, mid and premium segments. In the premium segment, it was the fastest growing brand in 2021.

Transsion Group brands (itel, Infinix and TECNO) registered 55% YoY growth in 2021 and crossed 10 million shipments for the first time ever in a single year. They also maintained their third position in the overall handset market, with itel being the largest player in the feature phone market. Aggressive launches with a strong value proposition, strong demand in Tier 2 and Tier 3 cities and hybrid channel strategy were some of the factors behind this growth.

Apple was one of the fastest growing brands in 2021 with 108% YoY growth in shipments. It maintained its lead in the premium segment (>IRs 30,000) with a 44% share. Aggressive offers during the festive season, strong demand for the iPhone 12 and iPhone 13 and increased ‘Make in India’ capabilities drove high growth. We expect strong momentum for Apple in 2022 as well with increased manufacturing and retail footprint.

OnePlus reached its highest ever shipments in 2021, crossing the 5-million mark with 59% YoY growth driven by the OnePlus Nord Series. It led the affordable premium segment (INR 30,000-INR 45,000). It also captured the second position in the premium segment (>INR 30,000) with a 19% share. Camera innovations will be a key focus for OnePlus in 2022.

Major highlights

• India’s smartphone market revenue crossed $38 billion in 2021 with 27% YoY growth.

• Xiaomi led the market with a 24% shipment share. The brand also reached its highest ever share in the premium segment (>INR 30,000, ~$400) with 258% YoY growth.

• Samsung registered its highest ever retail ASP in 2021. The brand led the Rs 20,000-Rs 45,000 price segment with a 28% share.

• OnePlus registered its highest ever shipments in India in 2021 and led the affordable premium segment (Rs 30,000-Rs 45,000)

• 5G shipments registered 555% YoY growth in 2021. vivo led the 5G smartphone shipments in 2021 with a 19% share.

• 5G smartphone shipments crossed 10 mn mark in December 2021

• Among the top five brands in 2021, realme was the fastest growing brand. It captured the second position in Q4 2021 for the first time.

• OnePlus registered its highest ever shipments in India. Nord series cumulative shipments crossed 3 million units.

• Apple led the premium segment (>INR 30,000) with 45% share.

• India’s smartphone market registered its highest ever shipments in H1 2021

• realme became the fastest brand to reach 50 million cumulative smartphone shipments in India

Outlook

The initial two quarters of the year 2022 has shown almost flat growth amidst a low seasonal demand and a mild impact of the third wave of Covid-19. This is expected to give the brands time to replenish their inventories. The transition from 4G to 5G will continue to drive growth, though still restricted to mid and high-tier price segments.

Legal Battle Over IT Act Intensifies Amid Musk’s India Plans

The outcome of the legal dispute between X Corp and the Indian government c...

Wipro inks 10-year deal with Phoenix Group's ReAssure UK worth

The agreement, executed through Wipro and its 100% subsidiary,...

Centre announces that DPDP Rules nearing Finalisation by April

The government seeks to refine the rules for robust data protection, ensuri...

Home Ministry cracks down on PoS agents in digital arrest scam

Digital arrest scams are a growing cybercrime where victims are coerced or ...

Hrithik Roshan to endorse RuPay as Brand Ambassador

RuPay is reportedly planning to feature Bollywood superstar Hrithik Rosha

India Today Group launches – AI Pop Stars

Staying true to our industry leadership position in using cutting-edge tech

TelioLabs ropes in Phaniraj V A as the Group CEO

TelioLabs has announced the onboarding of Phaniraj V A as its new Group CE

Wipro Appoints Amit Kumar as Managing Partner and Global Head

Wipro Limited (NYSE: WIT, BSE: 507685, NSE: WIPRO), a leading technology s

Alpha Max offers high end solutions in the network space to en

The vision at Alpha Max is to attain quality as the trademark and create a

In India, 88% of Indian business leaders are planning to inves

As we move through 2024, it has become increasingly clear that AI is not ju

MSI Announces the availability of RTX 50 series of laptops in

MSI, the innovative computing manufacturer in gaming, creator

goes on sale today, starting at Rs 19,999")

Nothing Phone (3a) goes on sale today, starting at Rs 19,999

The phone was launched on March 4, featuring a 50MP main, ultra-wide, and t

VVDN TECHNOLOGIES

ZOHO CORPORATION PVT. LTD.

FRESHWORKS TECHNOLOGIES PVT. LTD.

NETWEB TECHNOLOGIES INDIA LTD.

Icons Of India : MUKESH D. AMBANI

Mukesh Dhirubhai Ambani is an Indian businessman and the chairman and ...

ICONS OF INDIA : SOM SATSANGI

With more than three decades in the IT Sector, Som is responsible for ...

Icons Of India : Puneet Chandok

Puneet Chandok is President, Microsoft India & South Asia and is respo...

HPCL - Hindustan Petroleum Corporation Ltd.

HPCL is an integrated oil and gas company involved in refining, market...

UIDAI - Unique Identification Authority of India

UIDAI and the Aadhaar system represent a significant milestone in Indi...

ITI - ITI Limited

ITI Limited is a leading provider of telecommunications equipment, sol...

Indian Tech Talent Excelling The Tech World - Soni Jiandani, Co-Founder- Pensando Systems

Soni Jiandani, Co-Founder of Pensando Systems, is a tech visionary ren...

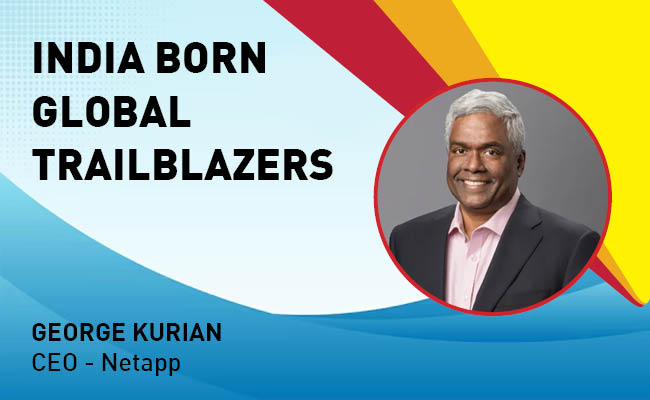

Indian Tech Talent Excelling The Tech World - George Kurian, CEO, Netapp

George Kurian, the CEO of global data storage and management services ...

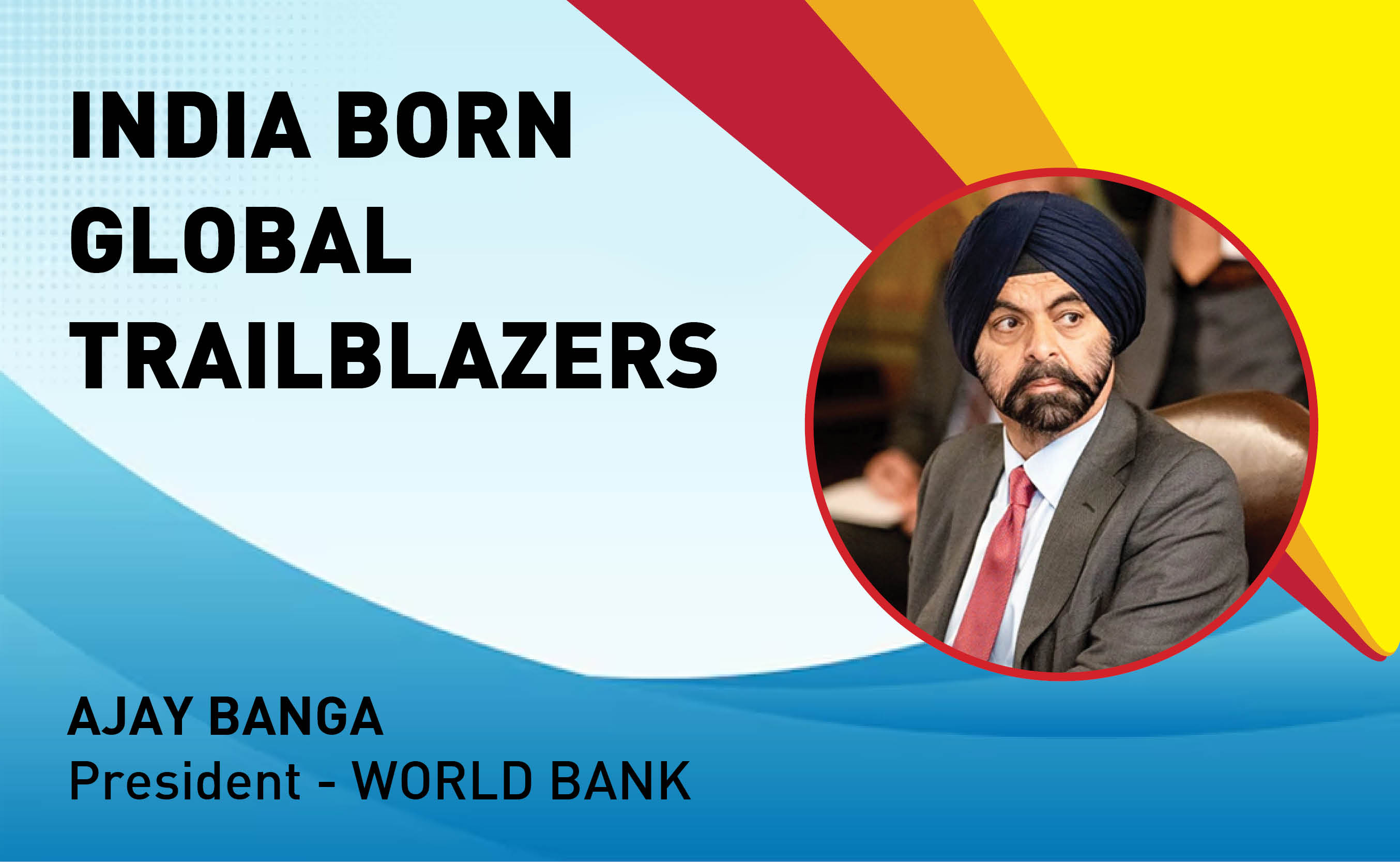

Indian Tech Talent Excelling The Tech World - AJAY BANGA, President - World Bank

Ajay Banga is an Indian-born American business executive who currently...

of images belongs to the respective copyright holders

of images belongs to the respective copyright holders