IT industry revenue to cross US$200 billion in FY2022

By MYBRANDBOOK

The Production-Linked Incentive (PLI) Scheme for IT Hardware aims to boost India’s manufacturing capacity for laptops, tablets, all-in-one PCs, and servers, as well as attract greater foreign investment. Foreign investors with a registered company in India are eligible to participate under this scheme.

Global shipments of traditional PCs, including desktops, notebooks, and workstations, declined 5.1% in the first quarter of 2022 (1Q22) but exceeded earlier forecasts, according to preliminary results from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker. The PC market is coming off two years of double-digit growth, so while the first quarter decline is a change in this momentum, it doesn’t mean the industry is in a downward spiral.

“A perfect storm of geopolitics upheaval, high inflation, currency fluctuations and supply chain disruptions have lowered business and consumer demand for devices across the world, and is set to impact the PC market the hardest in 2022. At the same time the “Consumer PC demand is on pace to decline 13.1% in 2022 and will plummet much faster than business PC demand, which is expected to decline 7.2% year over year.”

The IT spending in India is expected to touch $105.2 billion in 2022, an increase of 5.5% from 2021, as per Gartner. The worldwide IT spending is projected to total $4.5 trillion in 2022, an increase of 5.1% from 2021. Despite the potential impacts of the Omicron variant, economic recovery with high expectations for digital market prosperity will continue to boost technology investments.

The Indian IT industry is expected to clock revenue of $227 billion in FY2022 against $196 billion last year. The industry, which has a total workforce of around 5 million, is likely to register a 15.5 percent growth, the highest since 2011, as per NASSCOM. This was a year of resurgence which came after the one of resilience following the Covid-19 pandemic.

The main growth in the manufacturing (Make In India) is driven by the scheme for Promotion of Manufacturing of Electronic Components and Semiconductors

Government of India’s goal is to make India a significant design and manufacturing hub in the Global Value chain for Electronics as part of its Atmanirbhar Bharat Economic policies. To establish India as a global leader in electronics manufacturing, Government of India has launched many flagship schemes which are aimed at “Atmanirbhar Bharat – A self-reliant India’’ under the aegis of National Policy on Electronics 2019 (NPE 2019). It was notified on April 01, 2020 and provides financial incentive of 25% on capital expenditure for the identified list of electronic goods that comprise downstream value chain of electronic products, i.e., electronic components, semiconductor / display fabrication units, ATMP units, specialized sub-assemblies and capital goods for manufacture of aforesaid goods. The scheme is open to receive applications till 31.03.2023. As on February 28, 2022, the Executive Committee (EC) has approved 23 applications with total project outlay of Rs.6,816 crore and committed incentives of Rs 1,245 crore. The total employment generation potential of the approved applications is 29,021 (Twenty nine thousand and twenty one).

The Government has taken strategic steps and initiatives to expand the electronics manufacturing sector in the country and make India a global electronics manufacturing and design hub. As a result of various initiatives taken by the Government, several proposals have been received from foreign investors under the following schemes:

Under the Modified Special Incentive Package Scheme (M-SIPS), a total of 127 proposals with proposed investment of Rs 59,086 crore from companies having foreign shareholding are under consideration for setting up of units for manufacturing of electronic goods/products. Out of these 127 proposals, 124 proposals with proposed investment of Rs 56,341 crore have been approved. The reported capital expenditure incurred by 104 approved applicants (out of the approved 124 applicants) for electronic equipment manufacturing is Rs. 19,600 crore.

Under the Production Linked Incentive Scheme (PLI) for Large Scale Electronics Manufacturing notified on 1st April, 2020, a total of 12 applications from foreign companies have been approved.

Under the Production Linked Incentive Scheme (PLI) for IT Hardware notified on 03rd March, 2021, a total of 4 applications from foreign companies have been approved.

Indian PC Business

The Indian hardware market has seen a sharp growth with the demand surging for Laptops, smartphones becoming a necessity and the knowledge of using these devices became essential for everyone, equally. To adhere to the social distancing norms, people’s reliance on e-commerce websites and mobile apps has increased multiple times. Businesses that were limited to physical models like fitness centres, also found the last resort in going digital with customized apps, etc.

With more and more dependence on mobile applications and smartphones, the demand for mobile app developers has certainly increased. The app economy and app developers are interdependent. Also, this has led to many tech companies hiring software engineers with experience in mobile application development.

At the same time, the ed-tech industry, in particular, is the most benefited sector during this pandemic situation. Most schools, colleges, and coaching classes have opted for online or virtual teaching methods. In fact, not just academics but virtual training has been extensively used by those offering hobby classes as well.

The global pandemic has certainly brought online education to the limelight. Technologies like digital marketing, cloud, and cyber security, python for machine learning are some courses that have seen a huge demand during this time.

One can call it the pandemic effect, but bumper sales of laptops and notebooks in the lockdown period has prompted Korean giant Samsung to re- enter the segment after a period of nearly nine years.

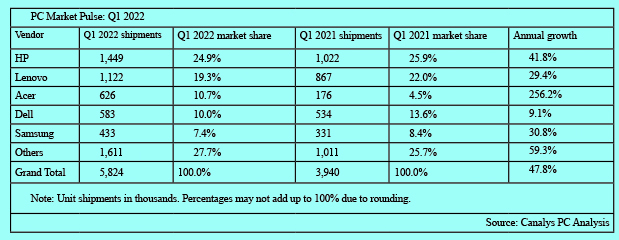

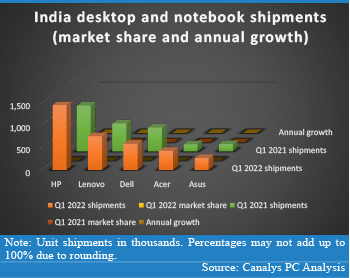

India’s PC shipments (desktops, notebooks and tablets) rocketed by 48% in Q1 2022 to a record-breaking 5.8 million units, beating the previous record of 5.3 million in Q3 2021. In the last six quarters, shipments have grown by 44% on average, despite sustained pressure on the global supply chain. They have now surpassed the 5 million-mark for a third quarter in a row. India now accounts for 5% of global PC shipments, compared with just 3% two years ago. Notebooks were the largest category, with 3.4 million units shipped, up 36% year on year. Desktop shipments surpassed 880,000 units, a phenomenal 64% increase over Q1 2021. But tablets were the strongest category, with shipments reaching 1.6 million, up 69% on a year ago, largely due to government orders picking up again after a two-year hiatus.

Vendor performances

HP took the leading position with ease in Q1 2022, commanding a 25% share of the total market and growing its PC shipments by an impressive 42% to 1.5 million units. HP continues its dream run in notebook and desktop shipments, accounting for 34% of the total market, up by 42% and outpacing the next highest vendor almost twice over in total shipment terms. HP has historically dominated the commercial PC market (desktops, notebooks, workstations and tablets), averaging a stellar 32% market share over the last four quarters. But a strong comeback of 29% year-on-year growth and a 23% market share in the more competitive consumer segment underlines HP’s strategic pricing and channel strategies for the Indian PC market. Furthermore, its local manufacturing initiatives, combined with a diverse range of customized PC offerings across segment groups, drove HP’s total shipments to an all-time high.

Lenovo came second overall (including tablets) in Q1 2022, accounting for 19% of the total PC market with 1.1 million shipments. Lenovo’s shipments grew 29% year on year to surpass the 1 million-mark for a third quarter in a row. This growth was bolstered by the vendor’s consistent performance in notebook and tablet shipments, which increased by 26% and 53% year on year respectively. Lenovo’s ability to channel this mounting demand for notebooks across segments resonates with its global supply chain digitization initiatives and significant R&D investments. While Lenovo sees greater untapped potential in the Indian PC market across segments (particularly private and public education), a third manufacturing line recently added to its Puducherry plant aims to double the current capacity.

Acer surpassed the 600,000-mark for the first time in the Indian PC market (including tablets), taking 11% of the total market and pushing Dell into fourth place. Acer shipped 626,000 units in Q1 2022, up by a lofty 256% year on year and 1.7 times more than in Q4 2021. This uptick was intensified by Acer’s overall performance in the Indian market. But tablet shipments grew by a staggering 1,288% to 205,000 units in Q1 2022, the strongest growth category for an individual vendor in Q1 2022. Acer’s ability to compete in government tenders while offering a diverse range of locally manufactured and efficient PCs enabled it to reap massive benefits.

Dell finished fourth with just over 580,000 shipments in Q1 2022, accounting for 10% of the total PC market (including tablets) and up by 9% year on year. Desktop shipments increased by an exceptional 65% in Q1 2022, taking shipments to 111,000 units. Furthermore, Dell experienced consistent single-digit growth across all segment groups.

Samsung moved up the ranks in Q1 2022 to take fifth place in overall PC shipments (including tablets). In India, Samsung is predominantly a tablet vendor, with shipments reaching a new high of 433,000 units in a single quarter, up 31% year on year. The gradual re-emergence of government tenders boosted Samsung’s shipments in the Indian market, allowing it to reclaim the top spot in the tablet market, where it held a 28% share.

India breaks record again with 5.8 million PC shipments in Q1 2022

“Firstly, India’s success at managing COVID-19, despite its huge population, has to be recognized. While most of the world was in lockdown, India remained open for business as usual to a large degree. This helped the economy resurge, creating additional demand for PCs and other IT infrastructure. Secondly, India is slowly but surely inching toward self-reliance in PC production. 18% of all PCs sold in India are now manufactured locally, implying that India’s vulnerability to black swan events in China is diminishing, and that its own appetite for PC consumption is increasing. While global macroeconomic events are raising multiple concerns over the sustainability of this growth, India will stay strong for the coming few quarters, despite the softness expected in other global markets.”

“Inflation woes continue to plague the market in 2022, as unprecedented global food prices have sent local prices soaring, with average inflation over 6% for the past three months,”. “With the Reserve Bank of India pushing up base lending rates, which are expected to continue to increase through the year to battle wholesale inflation, businesses in debt will feel the crunch, as they have less capital to work with. While consumers will stop making discretionary purchases, companies, both small and large, have shown an inclination to freeze budgets, stop hiring and cut spending, which will have a ripple effect on IT procurement, and thereby PC demand. Canalys advises PC vendors to exercise caution while planning for the quarters ahead. At the same time, large government tenders for education are expected to keep the market buoyant.”

Server Market

The server market revenues were flat in 2020 and early 2021 owing to the pandemic and less spending by enterprises on IT infrastructure upgrades and expansion.

From an enterprise perspective, transformation to hybrid cloud and upgrades of existing infrastructure to handle increased workloads will provide growth impetus after a pause during the COVID-19 pandemic. 5G, automotive, cloud gaming and high-performance computing will remain the key drivers for cloud service providers in data centre expansion.

Companies are looking to strengthen their infrastructure as they prepare for Web3.0 demands from the infrastructure end and secondly, companies are diversifying their IT infrastructure to meet the needs of data evolution and making customers cloud-ready.The market is evolving with the introduction of “As-a-Service” and “pay per use” models by server companies, like Pointnext from HPE, APEX from Dell and TruScale from Lenovo.

Dell and HPE are the server market icons but are seeing companies like Lenovo, Inspur and Supermicro giving strong competition as demand for flexible customised configurations in bare metal options continues to rise.

The x86 server market increased YoY by 12.3% in terms of revenue to reach $261.6 million in Q2 2021 from $232.9 million in Q2 2020. During 2021Q2, verticals such as insurance, media and resource industries witnessed the highest YoY growth in terms of revenue.

The non x86 server market decreased YoY by 28.8% to reach $27.9 million in terms of revenue in Q2 2021 from $39.1 million in Q2 2020. IBM continues to dominate the market with 41.1% of revenue share, during 2021Q2 with an absolute revenue of $11.5 million. Oracle came in second position followed by Hewlett Packard Enterprise (HPE), with a revenue share of 18.4% and 4.5%, respectively.

External Storage

Strong demand driven by the need for storage to support digital transformation initiatives, enhance analytics, increase employee productivity, and improve customer experience, on one hand, and tight supply and increasing system prices on the other.

India’s external storage market witnessed a growth of 14.8% year-over-year (YoY) by vendor revenue and stood at $73.7 million in Q2 2021 (April - June), as per the latest quarterly enterprise storage systems tracker by IDC.

The quarter witnessed YoY growth in storage spending from the government, and manufacturing verticals, while it observed a sharp decline in contribution from BFSI, professional services, and telecommunications verticals during the period.

Enterprises are forced to change their existing IT architectures to be adaptive and efficient while securing the workloads. Additionally, workloads are getting distributed to the edge, which is even more complicating things for organisations,” said Dileep Nadimpalli, senior research manager, enterprise infrastructure, IDC India.

The adoption of All-Flash Arrays (AFA) was evident, contributing 34.4% to the overall external storage systems market in Q2 2021, according to the tracker. The emergence of NVMe flash media would further drive the AFA market due to better cost versus performance ratio across verticals. HDD arrays too saw strong growth in Q2 2021 due to uptake of backup appliances for data protection needs, it further said.

Entry-level storage systems grew by 65.4% YoY due to increased investments from banking, government, professional services, and manufacturing organisations in Q2 2021. The high-end storage segment witnessed a YoY decline; however, this segment would see an uptake in the next couple of quarters, IDC predicted.

“Enterprises are forced to change their existing IT architectures to be adaptive and efficient while securing the workloads. Additionally, workloads are getting distributed to the edge, which is even more complicating things for organisations. Enterprises are looking for an  infrastructure platform which offers complete end-to-end data services along with built-in security features

infrastructure platform which offers complete end-to-end data services along with built-in security features

Dell Technologies continued to be the market leader in India’s x86 mainstream server market in Q1 2022 with an industry share of 44.9%, the highest share achieved in mainstream servers. Dell Technologies continued to be the market leader in the external storage systems market followed by HPE and NetApp.

The war between Russia and Ukraine continues to impact the market in both direct and indirect ways. In the most direct way, system sales in Russia and Ukraine plunged in Q1 2022 and will continue declining, driving the decline in the overall Central and Eastern European region. Indirectly, the war added to already growing energy prices and transportation costs, which have a rippling impact on the IT industry.

Russia and Ukraine are major suppliers of neon gas and palladium, both used in the semiconductor manufacturing process. In the short-term (3-6 months), accumulated inventories should satisfy demand for raw materials resulting in minimal if any disruptions to component manufacturing. Mid-term (9-24 months) will be critically impacted by the ability of alternative suppliers to increase or initiate production of raw materials in other regions. Ramping up of the production and supply chain adjustment could take time resulting in possible component shortage toward the end of 2022 and the beginning of 2023. Long-term, it is expected full adjustment of the supply chain to source raw materials from outside of Russia and, possibly, Ukraine.

Overall, the storage systems market is more resilient to the negative forces than some other IT segments due to continuous business digitization which relies on data. Moreover, some of the developments enable more infrastructure spending in some workloads including security and data protection.

Printer Market

According to the latest data released by IDC Worldwide Quarterly Hardcopy Peripherals Tracker India’s Printer market registered shipment of 0.84 million units in 3Q21 (Jul-Sep) growing by 20.3% quarter-over-quarter (QoQ) however declining by 7.5% from year-over-year (YoY) perspective. The printer market includes Inkjet printers, Laser A3/A4 printers and Copiers, Serial Dot Matrix Printers, and Line Printers.

The inkjet printers’ segment declined YoY by 11.9% due to the low stock availability of ink cartridge printers. From a QoQ perspective, the segment however grew by 21.8%, primarily by HP’s delayed 2Q21 shipment spilling over into 3Q21. Additionally, with schools and colleges being forced to continue the virtual classes, demand from parents and students remained strong in 3Q21.

The inkjet printers’ segment declined YoY by 11.9% due to the low stock availability of ink cartridge printers. From a QoQ perspective, the segment however grew by 21.8%, primarily by HP’s delayed 2Q21 shipment spilling over into 3Q21. Additionally, with schools and colleges being forced to continue the virtual classes, demand from parents and students remained strong in 3Q21.

The laser printers’ segment (including copiers) recorded a marginal YoY decline of 1.8%. The laser copier segment, however, observed a YoY growth of 15.1%. With the markets opening further, the demand from the government picked up following an increase in the number of new projects and execution of those that were previously on hold. The corporate sector, too, observed a surge in demand for laser copiers as they began resuming operations from offices in a phased manner.

“In the inkjet printer segment, while the shipment of single-function printers declined, that of the multifunction printers grew at 25.2% YoY. This growth came primarily at the back of ink tank printers and more specifically from the $200 - $300 category of printers. Because of its price point and added functionalities, there is a growing preference for multi-function Ink tank printers over Laser A4 printers in offices where these printers are typically deployed in the cabins of senior-level management. Most of the demand was met by HP and it could have been higher had it not been for the stock crunch that Epson and Canon faced in 3Q21,” according IDC India.

Overall Top Companies in India Hardcopy Peripherals* (HCP) Market:

HP Inc. (excluding Samsung) maintained its leadership in the overall HCP market with a share of 46.9% and a YoY growth in shipment of 2.3%. The growth was led by the inkjet printer segment, wherein HP grew by 9.1% YoY, increasing its market share from the last few quarters to 46.3%, thus replacing Epson to occupy the 1st position in the inkjet printer segment. The growth came at the back of its ink tank portfolio which grew by 53.5% YoY coupled with the launch of new models in 3Q21. In the Laser A4 printer-based segment HP declined by 6.6% YoY as it struggled with product availability.

Epson occupied the 2nd position in the overall HCP market with a market share of 20.7% while registering a YoY decline of 9.4% because of the challenges it faced at the production end. In the inkjet segment, it occupied the 2nd position in the market with a share of 32.0%. Epson was particularly impacted in the ink tank multi-function printer category.

Canon recorded a YoY decline of 25.4% and occupied 3rd position in the overall India HCP market, capturing a unit market share of 20.1%. In the inkjet segment, Canon observed a YoY decline of 43.2% as it struggled with the stock availability of certain Ink cartridge models. In the laser segment (including laser copiers) Canon maintained its 2nd position with a market share of 24.8% while growing YoY by 12.0%. In the laser copier segment, Canon grew by 37.7% YoY and continued to lead the copier segment with a 35.1% market share.

Worldwide Industrial Segment Highlights for Q4 2021

Large format digital printer shipments grew 3.2% worldwide in 4Q21 compared to 3Q21.

Dedicated direct-to-garment (DTG) printer shipments declined 3.5% sequentially in 4Q21. IDC believes this is partially due to the impact of aqueous direct-to-film printers.

Direct-to-shape printer shipments grew 10% quarter over quarter in 4Q21.

Digital label & packaging printer shipments declined 11% sequentially in 4Q21.

Industrial textile printer shipments grew more than 10% in 4Q21, continuing a strong performance for the full year 2021.

The sharp shortage in the chip and increase in logistics costs will continue to impact the supply of printers and is also likely to cause an upward revision in prices as well. As schools/colleges open, we can expect demand for ink tank printers to start stabilizing in the coming quarters. Laser copier demand is expected to remain strong in Q4, as enterprises continue to bring employees back to offices.

Legal Battle Over IT Act Intensifies Amid Musk’s India Plans

The outcome of the legal dispute between X Corp and the Indian government c...

Wipro inks 10-year deal with Phoenix Group's ReAssure UK worth

The agreement, executed through Wipro and its 100% subsidiary,...

Centre announces that DPDP Rules nearing Finalisation by April

The government seeks to refine the rules for robust data protection, ensuri...

Home Ministry cracks down on PoS agents in digital arrest scam

Digital arrest scams are a growing cybercrime where victims are coerced or ...

Hrithik Roshan to endorse RuPay as Brand Ambassador

RuPay is reportedly planning to feature Bollywood superstar Hrithik Rosha

India Today Group launches – AI Pop Stars

Staying true to our industry leadership position in using cutting-edge tech

TelioLabs ropes in Phaniraj V A as the Group CEO

TelioLabs has announced the onboarding of Phaniraj V A as its new Group CE

Wipro Appoints Amit Kumar as Managing Partner and Global Head

Wipro Limited (NYSE: WIT, BSE: 507685, NSE: WIPRO), a leading technology s

Bolstering its commitment to help build a truly self-reliant B

CP PLUS is dedicated to spreading a sense of security to every corner of In

Acer addresses evolving customer needs by consistently pushing

Acer offers a comprehensive range of products under one roof, including des

MSI Announces the availability of RTX 50 series of laptops in

MSI, the innovative computing manufacturer in gaming, creator

goes on sale today, starting at Rs 19,999")

Nothing Phone (3a) goes on sale today, starting at Rs 19,999

The phone was launched on March 4, featuring a 50MP main, ultra-wide, and t

LAVA INTERNATIONAL LTD.

POLYCAB INDIA PVT. LTD

VERSA NETWORKS INDIA PVT. LTD.

BEETEL TELETECH LTD.

ICONS OF INDIA : SACHIN BANSAL

Sachin Bansal is an Indian entrepreneur. He is best known as the found...

Icons Of India : Debjani Ghosh

Debjani Ghosh is the President of the National Association of Software...

Icons Of India : Puneet Chandok

Puneet Chandok is President, Microsoft India & South Asia and is respo...

PFC - Power Finance Corporation Ltd

PFC is a leading financial institution in India specializing in power ...

NIC - National Informatics Centre

NIC serves as the primary IT solutions provider for the government of ...

DRDO - Defence Research and Development Organisation

DRDO responsible for the development of technology for use by the mili...

Indian Tech Talent Excelling The Tech World - Dheeraj Pandey, CEO, DevRev

Dheeraj Pandey, Co-founder and CEO at DevRev , has a remarkable journe...

Indian Tech Talent Excelling The Tech World - Sanjay Mehrotra, CEO- Micron Technology

Sanjay Mehrotra, the President and CEO of Micron Technology, is at the...

Indian Tech Talent Excelling The Tech World - AJAY BANGA, President - World Bank

Ajay Banga is an Indian-born American business executive who currently...

of images belongs to the respective copyright holders

of images belongs to the respective copyright holders