Software Industry : Adapting To changing Times

By MYBRANDBOOK

Riding on its exports prowess, as usual, the Indian IT and ITES industry could able to register a solid growth in the last fiscal

The Indian IT and ITeS industry showed a solid performance in FY2019 growing at almost 8.5% over the previous year. Multiple factors influenced this performance for the Indian players. An electrifying startup ecosystem, future-looking government initiatives like digital India, rapid upgradation of IT and communications infrastructure, increased export business and an ever increasing IT talent pool – all added to the momentum of the industry in last couple of years.

India’s highly qualified talent pool of technical graduates is one of the largest in the world, facilitating its emergence as a preferred destination for outsourcing. This leads to project India as a low-cost outsourcing market – almost 6 to 8 times less expensive compared to the US.

Like the past years, 2018 also saw India as the leading sourcing destination across the world, accounting for approximately 55 per cent market share of the $ 185-190 billion global services sourcing business in 2017-18. Indian IT & ITeS companies have set up over 1,000 global delivery centres in about 80 countries across the world and has become the digital capabilities hub of the world with around 75 per cent of global digital talent present in the country.

Factors like digitization, non-linear business models and SMAC remained the primary focus of Indian IT industry through out the year and these trends are expected to drive the growth of the industry in coming times as well.

Overall Market Size

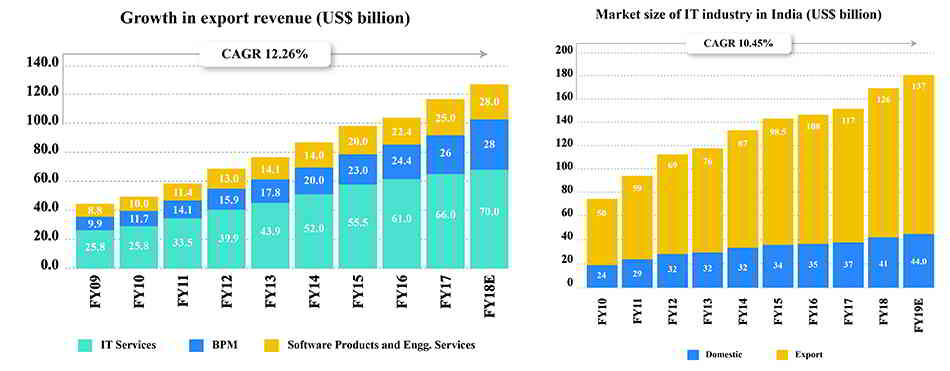

India’s IT & ITeS industry grew to $ 181 billion in 2018-19. Exports from the industry increased to $ 137 billion in FY19 while domestic revenues (including hardware) advanced to $ 44 billion. The market has grown at a CAGR of 10.45% from FY2010-19. Spending on Information Technology in India is expected to grow over 9 per cent to reach $ 87.1 billion in 2018.

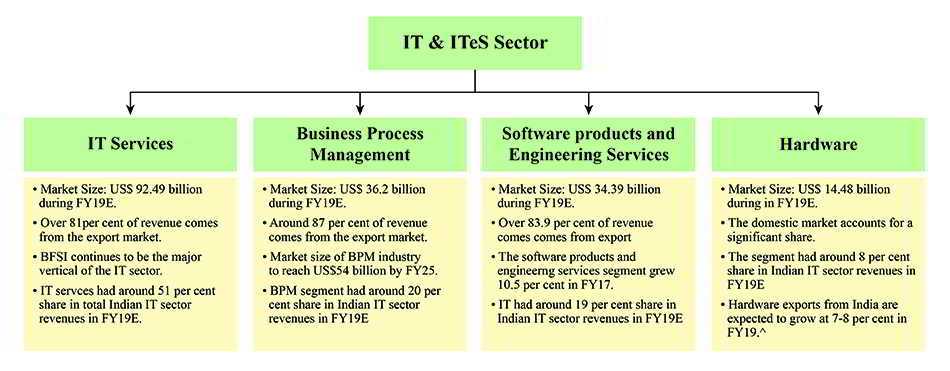

India’s IT industry is a collective of four distinct segments – IT services, business process management or BPM, software products and engineering services, and IT hardware.

IT services that includes export is the largest segment and contributed 51% of the total revenue of the Indian IT industry. Over 81% of the revenue of the segment comes from export alone. In FY19 the size of the Indian IT services market was pegged at $92 billion and BFSI remained the biggest industry vertical for the market.

The BPM market in FY2019 was pegged at $36.2 billion and contributed around 20% of the total revenue of the industry. 87% revenue of the segment came from exports and the market is expected to reach $54 billion by 2025, according to Nasscom.

The software product and engineering services accounted for 19% of India’s IT business and was pegged at $34.39 billion during last fiscal. Exports also contribute a major chunk of this business segment, around 83.9%, and the segment witnessed a growth of 10.5% during the fiscal.

Going forward, India’s IT-BPM sector is expected to expand to $ 350 billion by 2025 and BPM is expected to account for $ 50-55 billion out of the total revenue. Moreover, revenue from the digital segment is expected to form 38 per cent of the total industry revenue by 2025.

IT industry employs nearly 3.97 million people in India of which 105,000 were added in FY18. The industry added around 105,000 jobs in FY18 and is expected to add over 250,000 new jobs in 2019. Hardware exports from India are expected to grow at 7-8 per cent in FY19

Notable Trends

The ever dynamic Indian IT industry, both software and hardware, saw some notable trends in the last year. Though these trends, being a part of a continuous part of the industry, did not just show up in 2018, but it certainly saw some sort of maturity in the last year.

Social, Mobility, Analytics and Cloud (SMAC), a paradigm shift in IT-BPM approaches experienced until now, is leading to digitisation of the entire business model and impacting in a big way how companies conduct business.

Emergence of tier II, tier III cities as preferred IT destinations was also a key trend during the last couple of years. Tier II and III cities are increasingly gaining traction among IT companies, aiming to establish business in India. Cheap labour, affordable real estate, favourable government regulations, tax breaks and SEZ schemes facilitating their emergence as a new IT destination. Giving rise to the domestic hub and spoke model, with Tier I cities acting as hubs and Tier II, III and IV as network of spokes.

For example, in October 2018, HCL Technologies laid the foundation stone for a new global IT development centre at Vijayawada. The facility will come up over 29.86 acres at an investment of Rs 700 crore.

Also the business dynamics of the Indian IT industry is also changing very rapidly. The market saw focus shifting from bagging big ticket deals to number of small ticket contracts. Startups played a big role in it as customers booked these small players for their expertise in the relevant areas rather than going for a big IT firm having presence in multiple domains. This also proved to be more cost effective. Riding on this trend it is expected that number of startups in India would rise to 50000 and would contribute 2% of the country’s GDP in coming times.

Rising of onshoring was also a notable trend in 2018 as fall in automation costs and rise of digital has led to higher onshoring by the industry. Onshore revenue of Indian IT industry has grown from around 48 per cent in 2011-12 to 55.2 per cent for the quarter ended June 2018.

Exports Driving The Business

The Indian IT industry is thriving on the power of its business in exports, US being the biggest importer of our services. In 2018 almost 81% of business came from the industry’s export segment and IT services remained the biggest contributor to that contributing to almost 57% of total IT exports. BPO business contributed 21.20% whereas and engineering and R&D, and software products business contributed to 21.80% of total IT exports by the Indian companies during 2018.

US has traditionally been the biggest importer of Indian IT exports; over 62 per cent of Indian IT-BPM exports were absorbed by the US during FY18. Non US-UK countries accounted for just 21 per cent of total Indian IT-BPM exports during FY18. As of FY18, US and UK are the leading customer markets with a combined share of nearly 80%. However, there is growing demand from APAC, Latin America and Middle East Asia.

Being the low cost exporter of IT services, India is going to attract more markets in other regions in the same manner it tapped US markets.

Investments/ Developments

Indian IT’s core competencies and strengths have attracted significant investments from major countries. The computer software and hardware sector in India attracted cumulative FDI inflows worth $ 35.82 billion between April 2000 to December 2018, according to data released by the Department of Industrial Policy and Promotion (DIPP).

Leading Indian IT firms like Infosys, Wipro, TCS and Tech Mahindra, are diversifying their offerings and showcasing leading ideas in blockchain, artificial intelligence to clients using innovation hubs, research and development centres, in order to create differentiated offerings.

Government Initiatives

Some of the major initiatives taken by the government to promote IT and ITeS sector in India are as follows:

• The government has identified Information Technology as one of 12 champion service sectors for which an action plan is being developed. Also, the government has set up a Rs 5,000 crore fund for realising the potential of these champion service sectors.

• As a part of Union Budget 2018-19, NITI Aayog is going to set up a national level programme that will enable efforts in AI and will help in leveraging AI technology for development works in the country.

• In the Interim Budget 2019-20, the Government of India announced plans to launch a national programme on AI and setting up of a National AI portal.

• National Policy on Software Products-2019 was passed by the Union Cabinet to develop India as a software product nation.

Road Ahead

India is the topmost offshoring destination for IT companies across the world. Having proven its capabilities in delivering both on-shore and off-shore services to global clients, emerging technologies now offer an entire new gamut of opportunities for top IT firms in India. Export revenue from the industry has grown at a CAGR of 11.85 per cent to $ 137 billion in FY19E from $ 50 billion in FY10. The industry is expected to grow to $ 350 billion by 2025 and BPM is expected to account for $ 50-55 billion out of the total revenue.

Going forward it is expected that digital exports will become a major factor of growth for Indian IT players. This vertical is expected to rise to $310 billion by 2020 from $180 billion now, and the Indian IT majors would love to latch on to this opportunity.

"

GST Council likely to reduce tax on food delivery to 5%

The Goods and Services Tax (GST) Council is reportedly considering a prop...

Nazara and ONDC set to transform in-game monetization with ‘

Nazara Technologies has teamed up with the Open Network for Digital Comme...

Jio Platforms and NICSI to offer cloud services to government

In a collaborative initiative, the National Informatics Centre Services In...

BSNL awards ₹5,000 Cr Project to RVNL-Led Consortium

A syndicate led by Rail Vikas Nigam Limited (abbreviated as RVNL), along wi...

Pushpa 2 leaks online after recording highest pre-sales in Ind

Pushpa 2, which is one of the most anticipated films of the year, has had a

Eloelo teams up with Elvish Yadav for India's biggest digital

Eloelo, India’s leading platform for live entertainment and creator-drive

Visa elevates Rishi Chhabra as new Country Manager for India

Rishi holds a Master’s in Industrial Engineering from The Ohio State Univ

Genesys welcomes Albert Nel as Senior VP and Regional Sales Le

Genesys continues to deepen its investment in the APAC region. Earlier this

Autodesk continually pushing the boundaries in the Design and

Autodesk’s vision is of a better world designed and made for all. It inte

Cisco building a trusted and resilient future for the nation

Security is foundational to everything Cisco does and customers insist on e

SonicWall Launches TZ80: A Powerful Solution for Remote Office

SonicWall announced today the launch of the TZ80, a groundbreaking securit

Gigabyte X3D Turbo: A Gaming Revolution

GIGABYTE X3D Turbo Mode is a cutting-edge feature that unifies cores distr

WIPRO LTD.

ALPHAMAX TECHNOLOGIES PVT. LTD.

TEJAS NETWORKS INDIA PVT. LTD.

LENOVO INDIA PVT. LTD.

ICONS OF INDIA : SACHIN BANSAL

Sachin Bansal is an Indian entrepreneur. He is best known as the found...

ICONS OF INDIA : RISHAD PREMJI

Rishad Premji is Executive Chairman of Wipro Limited, a $11.3 billion ...

Icons Of India : MUKESH D. AMBANI

Mukesh Dhirubhai Ambani is an Indian businessman and the chairman and ...

BSE - Bombay Stock Exchange

The Bombay Stock Exchange (BSE) is one of India’s largest and oldest...

ITI - ITI Limited

ITI Limited is a leading provider of telecommunications equipment, sol...

CERT-IN - Indian Computer Emergency Response Team

CERT-In is a national nodal agency for responding to computer security...

Indian Tech Talent Excelling The Tech World - Dheeraj Pandey, CEO, DevRev

Dheeraj Pandey, Co-founder and CEO at DevRev , has a remarkable journe...

Indian Tech Talent Excelling The Tech World - Steve Sanghi, Executive Chair, Microchip

Steve Sanghi, the Executive Chair of Microchip Technology, has been a ...

Indian Tech Talent Excelling The Tech World - Rajiv Ramaswami, President & CEO, Nutanix Technologies

Rajiv Ramaswami, President and CEO of Nutanix, brings over 30 years of...