Fiscal 2025–26 marked the moment India's semiconductor ambition crossed from policy intent to operational reality, with the country's first modern chip packaging facility inaugurated, its first fabrication plant under construction, and a global AI-driven boom reshaping the entire semiconductor value chain

For decades, India's semiconductor story was one of conspicuous imbalance. The country produced approximately 20 percent of the world's semiconductor design engineers, the intellectual architects of chips that powered everything from smartphones to satellites, yet manufactured virtually none of those chips on home soil. Every chip consumed by India's booming electronics, automotive, telecom, and data centre industries arrived as an import, drawing down foreign exchange, extending supply chains, and leaving the country exposed to geopolitical disruptions it could not control. Fiscal 2025–26 did not fully resolve that imbalance, but it delivered the most consequential set of steps toward resolution in India's history. A new facility was inaugurated. A fab broke ground in earnest. Policy was translated into steel, silicon, and cleanrooms. And a global semiconductor boom, driven by artificial intelligence at a scale the industry had never seen, created both the urgency and the commercial logic for India's manufacturing ambitions to finally take root.

The Global Market: A Historic Boom Driven by AI

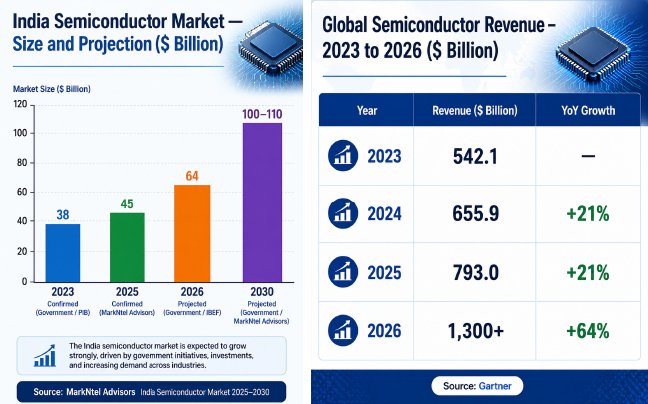

The global semiconductor industry delivered one of its most extraordinary performances in calendar year 2025. Worldwide semiconductor revenue totalled $793 billion, an increase of 21 percent year-on-year from $655.9 billion in 2024, according to preliminary results from Gartner published in January 2026. AI semiconductors, including processors, high-bandwidth memory, and networking components, accounted for nearly one-third of total semiconductor sales in 2025, with AI processor revenue exceeding $200 billion. HBM, the high-performance memory architecture essential for AI accelerators, surpassed $30 billion in sales in 2025, representing 23 percent of the total DRAM market.

NVIDIA became the defining story of the year, crossing $100 billion in semiconductor revenue in 2025, the first vendor in history to do so, and extending its lead over Samsung by $53 billion. NVIDIA contributed over 35 percent of total industry growth in 2025, according to Gartner. Samsung retained the second position, driven by DRAM and HBM demand, while Intel continued to lose share across its major product lines.

IDC, in its September 2025 Worldwide Semiconductor Technology Supply Chain Intelligence update, projected the semiconductor market to become a trillion-dollar industry by 2028, nearly two years ahead of earlier consensus estimates. IDC also projected the compute segment of the semiconductor market to grow 36 percent to $349 billion in 2025, with a 12 percent five-year CAGR through 2030.

Looking into fiscal 2026–27, the outlook is dramatic. Gartner's April 2026 forecast projects global semiconductor revenue to exceed $1.3 trillion in 2026, representing growth of 64 percent in a single year, driven by AI processing demand, data centre networking, power semiconductors, and a phenomenon Gartner analysts are calling "memflation." This refers to a sharp inflation in memory chip prices, with DRAM prices projected to rise 125 percent and NAND flash prices 234 percent in 2026. Gartner analysts cautioned that memflation will suppress non-AI demand into 2028 and advised enterprises against signing supply agreements with unfavourable pricing terms extending beyond 2027.

India's Semiconductor Market: A $45 Billion Base, Targeting $100 Billion India's semiconductor market was valued at approximately $45 billion in 2025 and is projected to reach $100 billion by 2030 at a CAGR of 13.05 percent, according to MarkNtel Advisors. The government's own projections, cited in PIB communications, place India's semiconductor demand at $100–110 billion by 2030, making it one of the fastest-growing semiconductor consumption markets in the world. A separate government projection, cited by IBEF, targets India's semiconductor market at $64 billion by 2026, an aggressive near-term figure driven by data centre AI infrastructure demand, 5G rollout, EV proliferation, and smartphone manufacturing expansion.

India's semiconductor market was valued at approximately $45 billion in 2025 and is projected to reach $100 billion by 2030 at a CAGR of 13.05 percent, according to MarkNtel Advisors. The government's own projections, cited in PIB communications, place India's semiconductor demand at $100–110 billion by 2030, making it one of the fastest-growing semiconductor consumption markets in the world. A separate government projection, cited by IBEF, targets India's semiconductor market at $64 billion by 2026, an aggressive near-term figure driven by data centre AI infrastructure demand, 5G rollout, EV proliferation, and smartphone manufacturing expansion.

South India dominates India's semiconductor ecosystem, capturing 36.2 percent of revenues in 2025, according to IMARC Group. Bengaluru is Asia's largest chip design hub outside Taiwan and South Korea, housing design centres for Intel, AMD, Qualcomm, Micron, Texas Instruments, Broadcom, and over 100 fabless semiconductor companies. India accounts for approximately 20 percent of the world's semiconductor design workforce, a talent concentration that has historically been the country's primary contribution to the global chip industry, and the foundation on which its manufacturing ambitions are now being built.

The end-use demand picture is equally broad. Consumer electronics led with a 30.4 percent share of India's semiconductor demand in 2025, followed by automotive at 16.2 percent and industrial at 14.8 percent, according to IMARC Group. The automotive segment carries the highest growth potential given India's electric vehicle transition, which is driving demand for power management ICs, SiC and GaN power semiconductors, ADAS sensors, and domain controllers. AI-driven data centre demand, with over $30 billion in infrastructure investment commitments in fiscal 2025–26, is creating a new high-value demand vertical for advanced logic chips, HBM, and networking semiconductors within India.

The Policy Architecture: Semcon India Programme Doubles Its Target

The India Semiconductor Mission, anchored by the Semcon India Programme with an original outlay of Rs 76,000 crore, crossed a landmark in fiscal 2025–26. Investment commitments under the programme reached Rs 1.15 lakh crore by September 2025, nearly double the original target, according to Invest India. This acceleration reflects the combination of policy credibility, infrastructure progress, and the global strategic logic of diversifying semiconductor supply chains away from Taiwan and South Korea amid geopolitical uncertainty.

The Union Budget 2025–26 eliminated customs duties on lithography tools and ultrapure gases, two critical inputs for semiconductor manufacturing, trimming both build-out timelines and operational costs for approved projects. The Union Budget 2026–27 allocated Rs 8,000 crore to the semiconductor mission, the largest single-year outlay since the programme launched, signalling sustained government commitment through the construction and ramp-up phase. The Design Linked Incentive programme continued to support fabless chip design companies, with incentives specifically targeting gallium nitride and silicon carbide IP development, wide-bandgap semiconductor technologies critical for EV and power applications.

In June 2025, the government amended SEZ Rules to reduce the minimum land requirement for semiconductor facilities from 50 hectares to 10 hectares, introduced flexible encumbrance norms, and permitted domestic sales from semiconductor SEZs on payment of applicable duties, addressing practical barriers that had previously complicated greenfield fab development. The Union Ministry of Commerce and Industry formally notified the establishment of a Special Economic Zone for Tata Semiconductor Manufacturing Private Limited at Dholera, India's first chip fabrication SEZ, spanning 66 hectares and projected to create approximately 21,000 jobs.

The Milestone That Changed Everything: Micron Sanand Inaugurated

The single most significant operational event in India's semiconductor history during fiscal 2025–26 occurred on February 28, 2026, when Prime Minister Narendra Modi inaugurated Micron Technology's Assembly, Test, Mark and Package facility in Sanand, Gujarat. The facility, India's first operational semiconductor manufacturing unit of the current mission cycle, involved a total investment of $2.75 billion, supported by $825 million in government incentives from the Centre and the Gujarat government. It processes DRAM and NAND flash memory chips for mobile devices, data centres, and automotive applications, with Tata Projects having executed the construction.

The Micron Sanand facility is not a fabrication plant. It does not produce chips from raw wafers. It is an ATMP facility, meaning it receives partially processed semiconductor wafers from overseas fabs and performs the assembly, testing, marking, and packaging steps that convert them into finished, shippable chips.

This distinction matters for understanding where India sits in the semiconductor value chain. ATMP is the downstream layer, with lower capital intensity and lower technological complexity, but high employment intensity and strategic significance as the first step toward a complete domestic manufacturing ecosystem. With Micron Sanand now operational,

India has demonstrated that it can attract, build, and operate a global-standard semiconductor facility. That credibility milestone makes every subsequent investment easier to justify.

Key Players and Developments: Building the Ecosystem

Tata Electronics is the centrepiece of India's semiconductor manufacturing ambitions. Its 300mm AI-enabled fab in Dholera, Gujarat, developed in partnership with Taiwan's Powerchip Semiconductor Manufacturing Corporation with an investment of Rs 91,000 crore (approximately $11 billion), is under active construction, with first silicon targeted for late 2026. The facility will cover process nodes from 28nm to 110nm, targeting automotive, computing, communications, AI, and IoT chip markets, with capacity of up to 50,000 wafer starts per month. In April 2026, the Union Ministry of Commerce and Industry notified the Dholera facility as India's first chip fabrication SEZ, formally establishing its regulatory and incentive framework. In parallel, Tata Electronics' semiconductor Assembly and Test facility in Jagiroad, Assam, with an investment of Rs 27,000 crore, is progressing toward operational status, targeting 48 million chips per day at full capacity. TCS is collaborating with Tata Electronics to support the first made-in-India chip design and production initiative.

CG Power and Industrial Solutions, in partnership with Japan's Renesas Electronics and Thailand's Stars Microelectronics, is establishing a semiconductor ATMP facility in Sanand, Gujarat with an investment of Rs 7,600 crore, targeting 15 million chips per day at capacity. CG Power is scaling high-volume assembly and testing operations within the fiscal year, making it the second major domestic semiconductor manufacturer after Micron to reach operational status within India's Semcon India Programme.

HCL Technologies and Foxconn formed a joint venture in May 2025 to establish a semiconductor fabrication unit in Jewar, Uttar Pradesh, with a total investment of Rs 3,700 crore, approximately $446 million. The facility was allocated approximately 30 acres of land in Uttar Pradesh and represents the entry of India's IT services ecosystem into semiconductor manufacturing.

Kaynes Semicon, the semiconductor subsidiary of Kaynes Technology, committed Rs 3,307 crore to a chip manufacturing facility in Sanand, Gujarat, designed to deliver a daily output of 6.33 million chips targeting automotive and industrial electronics applications.

Mindgrove Technologies launched India's first homegrown microcontroller in September 2025. Named Secure IoT and based on an open-source RISC-V architecture, the chip is designed for IoT, industrial automation, and consumer electronics applications. Mindgrove's achievement represents the first tangible commercial output of India's Design Linked

Incentive ecosystem, demonstrating that the country can produce not just chip design services for global customers but its own proprietary silicon.

Qualcomm completed a 2nm chip tape-out in fiscal 2025–26 with design work done entirely across its Bengaluru, Chennai, and Hyderabad engineering centres, making it the first major US chipmaker to validate India's advanced chip design capability at the 2nm leading-edge node. The tape-out was fabricated at TSMC Taiwan, but the design validation demonstrates that Indian engineers are technically qualified for the most advanced semiconductor work globally.

ISRO built India's Vikram-32 chip microprocessor in 2025, a space-grade processor designed and developed entirely within India, marking the country's entry into sovereign chip design for critical and defence applications.

The Design Ecosystem: India's Enduring Strength

India's semiconductor design ecosystem continued its expansion in fiscal 2025–26. Bengaluru, Chennai, Hyderabad, and Pune collectively house design centres for virtually every major global semiconductor company. The Design Linked Incentive programme, which offers incentives of up to 50 percent of eligible expenditure for chip design companies, continued to attract new entrants, with particular momentum in RISC-V based architectures, AI accelerator designs, GaN and SiC power semiconductors, and edge computing chips.

Venture capital funding in Indian semiconductor startups rose to approximately $50 million in 2025, a 79 percent increase from $28 million in 2024, according to Inc42. While modest compared to software or AI startup investment, the upward trend reflects growing investor interest in less capital-intensive segments of the semiconductor stack, including chip design, RISC-V IP, AI ASICs, and specialised edge computing designs. India's semiconductor startup ecosystem, led by companies including Mindgrove, Saankhya Labs, Sensesemi, and Incore Semiconductors, is building a layer of indigenous IP that complements the global design services delivered by MNC design centres.

The Road Ahead: From ATMP to Full Fab Nation

India's semiconductor trajectory through fiscal 2026–27 and beyond is defined by a clear sequence of milestones. Union Electronics Minister Ashwini Vaishnaw stated in early 2026 that four semiconductor plants will be operational by end 2026, two more in 2027, and India's first full fabrication unit, Tata Electronics' Dholera fab, will be ready in 2028. That timeline is aggressive but grounded in verified construction progress and the regulatory framework now in place.

The global semiconductor market is projected to exceed $1.3 trillion in 2026, according to Gartner. AI semiconductors are expected to account for approximately 30 percent of total semiconductor revenue in 2026, with hyperscaler AI infrastructure spending rising more than 50 percent. India sits at the intersection of two powerful forces: a global supply chain diversification imperative driven by US-China geopolitical tensions and Taiwan Strait risk, and a domestic demand surge driven by AI data centres, EVs, 5G infrastructure, and a 155 million unit smartphone market.

The country that was once the world's chip design house is building the infrastructure to become its chip manufacturing partner. The Micron Sanand inauguration in February 2026 was the proof of concept. The Dholera fab will be the proof of scale. India's semiconductor decade is not coming. It has arrived.