FinTech Industry : Unprecedented Growth

By MYBRANDBOOK

Within a span of just 2 years, more than 1000 firms have joined the FinTech bandwagon to offer agile, improvised and easy-to-avail financial services to end users

Fintech refers to the technologies that aide in offering financial services, including banking, investments, insurance etc. These technologies are being used by startups as well as established players in the financial value chain to offer customized, secured, improvised and easy-to-avail financial services to the customers. Fintech also pertains to the start‑ups that are emerging to challenge traditional banking and financial players, using these technologies and covers an array of services, from crowd funding platforms and mobile payment solutions to online portfolio management tools and international money transfers.

As per RBI India ranks second in terms of FinTech adoption globally, with an adoption rate of 52 per cent. It is reported that there are as many as 1,218 FinTech firms operating in India which have created a large number of jobs. They are also generating a healthy appetite for investment.

Some of the major FinTech products and services currently used in the market place are Peer to Peer (P2P) lending platforms, crowd funding, block chain technology, distributed ledgers technology, Big Data, smart contracts, Robo advisors, E-aggregators, etc. These FinTech products are currently used in international finance, which bring together the lenders and borrowers, seekers and providers of information, with or without a nodal intermediation agency.

Some of the major FinTech products and services currently used in the market place are Peer to Peer (P2P) lending platforms, crowd funding, block chain technology, distributed ledgers technology, Big Data, smart contracts, Robo advisors, E-aggregators, etc. These FinTech products are currently used in international finance, which bring together the lenders and borrowers, seekers and providers of information, with or without a nodal intermediation agency.

FinTechs are attracting interest both from users of banking services and investment funds, which see them as the future of the financial sector. Even retail groups and telecom operators are looking for ways to offer financial services via their existing networks. This flurry of activities raises questions over what kind of financial landscape will emerge in the wake of the digital transformation.

Financial institutions are seeking to increase their knowledge in relation to technological innovation, both through partnerships with tech companies and by investing in or acquiring such companies. Despite this, there are wide differences in the preparedness of market participants for these changes in practice.

Developments in Payments landscape in India

Fintech enablement in India has been seen primarily across payments, lending, security/biometrics and wealth management. The modes of payments in India have leapfrogged from cash to alternate modes of payments registering phenomenal growth. The innovations have happened in all spheres - from common USSD channel access through NUUP, Immediate Payment Service (IMPS) – initiation of transactions through various options for real-time payments to end customer, with the latest being the Unified Payments Interface (UPI). Some of the developments in this regard are discussed below.

Fast Payments: Leveraging on the high mobile density in India, with a population of more than one billion, many PSPs utilize mobile payment apps to link underlying payment instruments with mobile phone numbers for fast payments via the Immediate Payment Service (IMPS) or for issuance of m-wallets. The Unified Payment Interface (UPI) developed by NPCI provides complete interoperability for merchant payments as well  as P2P payments. The UPI enables users to link their bank accounts with their mobile phone numbers through an application provided by the payment service providers (PSPs) and obtain a virtual address which can be used for making and receiving payments. Introduction of UPI has the potential to revolutionize digital payments and take India closer towards being a “Less Cash” society.

as P2P payments. The UPI enables users to link their bank accounts with their mobile phone numbers through an application provided by the payment service providers (PSPs) and obtain a virtual address which can be used for making and receiving payments. Introduction of UPI has the potential to revolutionize digital payments and take India closer towards being a “Less Cash” society.

Process Innovation: With the nation-wide implementation of Aadhaar, providing a unique identification number to all residents of India, NPCI has launched an Aadhar Enabled Payment System (AEPS) that is a safe and convenient channel enabling micropayments with every transaction validated by biometric authentication. In a further impetus to digital innovations, Unique Identification Authority of India (UIDAI) in collaboration with TCS plans to roll out an Android-based Aadhaar-Enabled Payment System (AEPS). The application can be downloaded by merchants on a smartphone and would require a fingerprint scanner to use it. The application is intended to facilitate undertaking transactions without any Card or PIN.

Wallets: The traditional modes to make payments include cheque, electronic payment modes viz., NEFT, RTGS, etc. and card (debit and credit) payments. The need for prepaid payment instruments in the form of physical card or e-wallet was felt to give non-bank customers the facility to use electronic modes of payments and give existing bank customers a safeguard measure that limits the extent to which they are exposed. The emergence of bank (State Bank Buddy, Citi MasterPass, ICICI Pockets) and non-bank (PayTM, Mobikwik, Oxigen, Citrus Pay, etc.) payment wallets in India has changed the landscape of payments. Many start-ups have entered the space to simplify mobile money transfer, such as Chillr application, which provides peer-to-peer money transfer without using bank account details. Several leading banks have launched their own digital wallets leveraging NPCI’s IMPS platform. These digital wallets are integrated with social media features as well. Digital Innovators are also promoting the Online to Offline (O2O) model to facilitate digital payments at local stores.

According to the Capgemini’s World Payment Report, mobile wallets will witness a compound annual growth rate (CAGR) of 148 per cent over the next five years and will be $4.4 billion by 2022. The digital wallets are also supposed to outshine UPI.

BHIM (Bharat Interface for Money): BHIM is a mobile app developed by NPCI, based on the Unified Payment Interface (UPI) and was launched on 30 December 2016. It is intended to facilitate e-payments directly through banks and as part of the drive towards cashless transactions. BHIM allow users to send or receive money to other UPI payment addresses or scanning QR code or account number with IFSC code or MMID (Mobile Money Identifier) Code to users who do not have a UPI-based bank account. BHIM allows users to check current balance in their bank accounts and to choose which bank account to use for conducting transactions, although only one can be active at any time. Users can create their own QR code for a fixed amount of money, which is helpful in merchant transactions.

The Market

India’s FinTech sector may be young but is growing rapidly, fueled by a large market base, an innovation-driven startup landscape and friendly government policies and regulations. Several startups populate this emerging and dynamic sector, while both traditional banking institutions and non-banking financial companies (NBFCs) are catching up. This new disruption in the banking and financial services sector has had a wide-ranging impact.

In India, FinTech has the potential to provide workable solutions to the problems faced by the traditional financial institutions such as low penetration, scarce credit history and cash driven transaction economy. If a collaborative participation from all the stakeholders, viz., regulators, market players and investors can be harnessed, Indian banking and financial services sector could be changed dramatically. FinTech service firms are currently redefining the way companies and consumers conduct transactions on a daily basis.

According to a report by Google and Boston Consulting Group (BCG), the Indian digital payments industry is estimated to touch $500 billion by 2020, contributing 15 per cent to the country’s GDP.

An interesting angle to India’s digital payment story is that it is going to be dominated by micro transactions (tractions of value lower than Rs 100). In fact, 50% of person-to-merchant transactions are to be under Rs.100, says the Google-BCG report. Alternate digital payment instruments like digital wallets, UPI, payment banks, Bharat QR are expected to grow fiercely and estimated to double their contribution to 30 per cent in the digital payment industry.

The Indian FinTech industry grew 282% between 2013 and 2014, and reached USD 450 million in 2015. At present around 1200 FinTech companies are operating in India and their investments are expected to grow by 170% by 2020. The Indian FinTech software market is forecasted to touch $2.4 billion by 2020 from a current $1.2 billion, as per NASSCOM. The transaction value for the Indian FinTech sector is estimated to be approximately $ 33 billion in 2016 and is forecasted to reach $ 73 billion in 2020.

The NEFT system handled 195 crore transactions valued at around Rs.172 lakh crore in 2017-18 growing by 4.9 times in terms of volume and 5.9 times in terms of value over the previous five years. Similarly, the number of transactions carried out through credit and debit cards in 2017-18 was 141 crore and 334 crore, respectively. Prepaid payment instruments (PPIs) recorded a volume of about 346 crore transactions, valued at Rs.1.4 lakh crore. Thus, the total card payments, in volume terms, stood at 52 per cent of the total retail payments during the year 2017-18.

Investments

In 2018, Asia achieved a new high for fintech funding, with almost $22.7 billion raised across 372 deals. More than half of this investment, however, came from one global-record shattering megadeal in H1’18: a $14 billion Series C round by Ant Financial. Outside of the Ant Financial deal, Asia only saw only one additional deal over $1 billion: a $1.3 billion raise by online lending platform Lu.com in December. While China continued to account for the largest fintech deals in Asia, there was an upswell of activity in other jurisdictions in the region over the course of 2018. Among the top ten deals during the year, three were based in India (Paytm: $356 million; PolicyBazaar: 200 million; CentrumDirect: 175 million), one in Australia (Avoka: $245 million); and one in the Philippines (Voyager Innovations: $215 million).

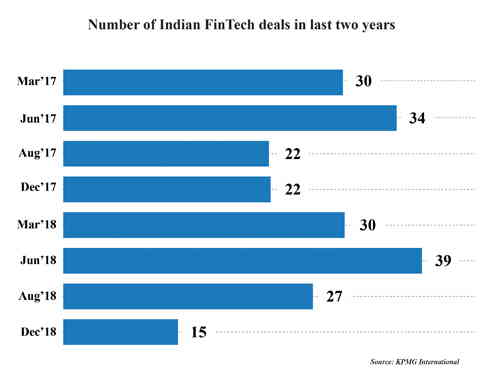

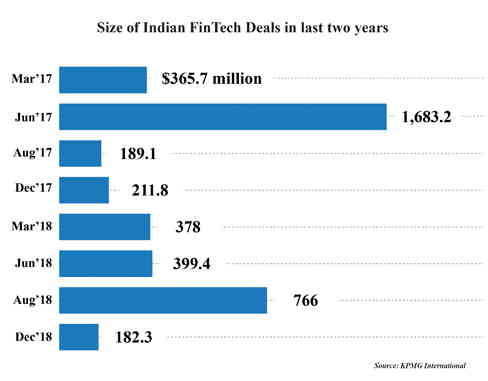

According to KPMG, the Indian Fintech sector raised $1.7 billion (Rs12,000 crore) in investments in 2018 though it is much lower than what the industry raised in 2017 - $4.3 billion. If we pit it against global trend, the size as well as the growth looks pitiable. Worrldwide, investments across mergers and acquisitions, private equity and venture capital funding in fintech space doubled to reach $111.8 billion in 2018.

However, the total number of deal volumes increased in 2018 as compared to 2017. In 2018 the total number of investment deals in the country’s fintech sector increased to 111 from 108 in 2017.

Driving Technologies

This exponential growth of the digital payment sector is driven by multiple factors including convenience to pay, the ever-growing smartphone penetration, rise of non-banking payment institutions (payments bank, digital wallets, etc.), progressive regulatory policies and increasing consumer readiness to the digital payment platform.

Mobile and Digital Payments: The majority of developments in the areas of payments are based on mobile technology by providing wrappers over existing payments infrastructure. Examples include Apple Pay, Samsung Pay, and Android Pay, which sit on top of existing card payment infrastructure enabling the user’s mobile devices to act as their credit/debit cards. There are also mobile payments built on new payment infrastructure, for example mobile phone money services, such as M-Pesa in Kenya and IMPS in India, which provide payment services. While such innovation facilitates the entrance of new users to the financial system, it may also move the provision of some payment services to non-banking companies that are not regulated as financial entities. There are a number of web-based and mobile-based payment applications that primarily focus on the customer experience and often aim to better integrate payment transactions within the commerce value chain. These service providers usually do not offer banking services other than payments, and they normally do not apply for banking licenses. The services can be offered by the payer’s own payment service provider (PSP) or by third party services (TPS), where an innovative service provider links payers and merchants by using the payer’s online banking credentials but without necessarily involving the payer’s PSP in the scheme or solution or by using the card payment infrastructure (Alipay, PayPal).

Mobile and Digital Payments: The majority of developments in the areas of payments are based on mobile technology by providing wrappers over existing payments infrastructure. Examples include Apple Pay, Samsung Pay, and Android Pay, which sit on top of existing card payment infrastructure enabling the user’s mobile devices to act as their credit/debit cards. There are also mobile payments built on new payment infrastructure, for example mobile phone money services, such as M-Pesa in Kenya and IMPS in India, which provide payment services. While such innovation facilitates the entrance of new users to the financial system, it may also move the provision of some payment services to non-banking companies that are not regulated as financial entities. There are a number of web-based and mobile-based payment applications that primarily focus on the customer experience and often aim to better integrate payment transactions within the commerce value chain. These service providers usually do not offer banking services other than payments, and they normally do not apply for banking licenses. The services can be offered by the payer’s own payment service provider (PSP) or by third party services (TPS), where an innovative service provider links payers and merchants by using the payer’s online banking credentials but without necessarily involving the payer’s PSP in the scheme or solution or by using the card payment infrastructure (Alipay, PayPal).

Digital currencies (DCs): Digital currencies (DCs) are digital representations of value, currently issued by private developers and denominated in their own unit of account. They are obtained, stored, accessed, and transacted electronically and neither denominated in any sovereign currency nor issued or backed by any government or central bank.

Digital currencies are not necessarily attached to a fiat currency, but are accepted by natural or legal persons as a means of exchange and can be transferred, stored or traded electronically. DC schemes comprise two key elements: (i) the digital representation of value or ‘currency’ that can be transferred between parties; and (ii) the way in which value is transferred from a payer to a payee.

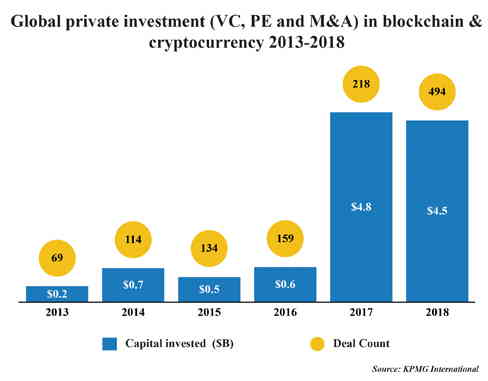

Privately issued DCs, such as Bitcoin, facilitate peer-to-peer exchange, possibly at lower cost for end-users and with faster transaction times, especially across borders. DC schemes are also known as ‘crypto currencies’ due to their use of cryptographic techniques. It is reported that there are hundreds of crypto currencies currently in use with an aggregate market capitalization of around USD 6.5bn5. However, only a very small fraction of these currencies are traded on a daily basis.

Crypto currencies derive their value solely from the expectation that others will be willing to exchange it for sovereign currency or goods and services. DC schemes may allow for the issuance of a limited or unlimited number of units. In most digital currency schemes, distributed ledger technology allows for remote peer-to-peer exchanges of electronic value. The various DC schemes differ from each other in a number of ways; they have different rules for supplying the currency; they differ in the way in which transactions are verified.

The implications of DCs for financial firms, markets and system will depend on the extent of their acceptability among users. If use of DCs were to become widespread, it would likely have material implications for the business models of financial institutions. DCs could potentially lead to a disintermediation of some existing payment services infrastructure.

At the moment, DCs schemes are not widely used or accepted, and they face a series of challenges that could limit their future growth. As a result, their influence on financial services and the wider economy is negligible today, and it is possible that in the long term they may remain a product for a limited user base on the fringes of mainstream financial services.

The regulatory perimeter around DCs is a complicated issue and regulation may depend on the definition of DCs in particular jurisdictions. The cross-border reach of DC schemes may make it difficult for national authorities to enforce laws.

Distributed ledgers Technology: Distributed ledger technologies (DLT) provide complete and secure transaction records, updated and verified by users, removing the need for a central authority. These technologies allow for direct peer-to-peer transactions, which might offer benefits, in terms of efficiency and security, over existing technological solutions.

The impetus behind the development and adoption of distributed ledger technology are the potential benefits. The major benefits are reduced cost; faster settlement time; reduction in counterparty risk; reduced need for third party intermediation; reduced collateral demand and latency; better fraud prevention; greater resiliency; simplification of reporting, data collection, and systemic risk monitoring; increased interconnectedness; and privacy.

Distributed ledger technology is an innovation with potentially broad applications in financial market infrastructures (FMIs) and in the economy as a whole. Its most common use at present is for digital currencies, but firms are stepping up their R&D activities for other uses including securities trading, smart contracts, and land and credit registries. If widely adopted, distributed ledger technology can pose new challenges for regulation. Though there are no imminent concerns, constant monitoring of developments in the application of the distributed ledger technology to financial services and systems is prudent given the significant potential of the technology.

Block chain Technology: Block chain is a distributed ledger in which transactions (e.g. involving digital currencies or securities) are stored as blocks (groups of transactions that are performed around the same point in time) on computers that are connected to the network. The ledger grows as the chain of blocks increases in size. Each new block of transactions has to be verified by the network before it can be added to the chain. This means that each computer connected to the network has full information about the transactions in the network. Block chain potentially has far-reaching implications for the financial sector, and this is prompting more and more banks, insurers and other financial institutions to invest in research into potential applications of this technology.

Frequently cited benefits of Block chain are its transparency, security and the fact that transactions are logged in the network. Some of the disadvantages currently include the lack of coordination and the scalability of this technology. One of the best-known applications of Block chain technology at the present time is bitcoin. Transactions in this virtual currency are largely anonymous. This creates ethical risks for financial institutions dealing with users of this currency, because they are unable to (fully) verify their identity.

It has also been observed that market participants in other securities markets are exploring the usage of Block chain or Distributed Database technology to provide various services such as clearing and settlement, trading, etc. Indian securities market may also see such developments in near future and, therefore, there is a need to understand the benefits, risks and challenges such developments may pose.

Road ahead

The future of Fintech in India looks more bright than the present. With increasing smartphone penetration, surge in broadband userbase, newer technologies helping end users availing financial services in a way hitherto unknown, the future offers an unforeseen success for the industry.

However, the opportunity will also bring along quite a handful of challenges related to regulations and supervision. This, of course, is already being closely watched by the apex bank and the RBI has already started using technologies like SupTech and RegTech to make regulatory framework more efficient through automated processes and lowers the costs of compliance.

"

InterGlobe’s Rahul Bhatia and C.P. Gurnani together announce

In a move that is set to transform the AI landscape, Rahul Bhatia, Group M...

Download masked Aadhaar to improve privacy

Download a masked Aadhaar from UIDAI to improve privacy. Select masking w...

Sterlite Technologies' Rs 145 crore claim against BSNL rejecte

An arbitrator has rejected broadband technology company Sterlite Technolog...

ID-REDACT® ensures full compliance with the DPDP Act for Indi

Data Safeguard India Pvt Ltd, a wholly-owned subsidiary of Data Safeguard ...

Salman Khan trolled for singing with B Praak at Anant Ambani's

To celebrate Mukesh Ambani's youngest son Anant Ambani’s 29th birthday

Disney+ Hotstar wins the Best OTT Platform of the year

Film Critics Guild and Group M Motion Entertainment, in collaboration with

SISL elevates Ankita Wadhawan as CEO—End User Computing

The IT service provider, SISL in a LinkedIn post announced the elevation

InfoVision appoints Radhika Venkatraman to its Advisory Board

Global digital services company, InfoVision has announced the appointment

ESDS commits to presenting clients with the latest technology

According to a NASSCOM report, the Indian IT industry experienced its stron

A few changes in policies can make the PLI scheme even more ef

The Production Linked Incentive (PLI) scheme is a government initiative tha

Canon India Introduces 4K Remote PTZ Camera Controller & 4K In

Canon India, a leading company in digital imaging solutions, further solidi

Dell Technologies launches the new consumer and gaming portfol

Dell Technologies has unveiled its newest line of AI-enabled consumer PCs

NETWEB TECHNOLOGIES INDIA LTD.

JUVAS SOLUTIONS PVT. LTD.

SAMRIDDHI AUTOMATIONS PVT. LTD.

TAC SECURITY SOLUTIONS

Technology Icons Of India 2023: Shailendra Katyal

Shailendra is instrumental in Lenovo achieving the no.1 position in PC...

Technology Icons Of India 2023: Rajiv Memani

As Chair of the EY Global Emerging Markets Committee, Rajiv connects e...

Technology Icons Of India 2023: Bhavish Aggarwal

Ola CEO Bhavish Aggarwal had formed Ola-India’s largest mobility pla...

BEL leveraging next generation technologies to keep the country ahead in Defence space

Bharat Electronics Limited (BEL) is a Navratna PSU under the Ministry ...

New defence PSUs will help India become self-reliant

MIL, India’s biggest manufacturer and market leader is engaged in Pr...

C-DOT enabling India in indigenous design, development and production of telecom technologies

An autonomous telecom R&D centre of Government of India, Center of Dev...

SAVEX TECHNOLOGIES PVT. LTD.

Savex Technologies is the 3rd largest Information & Communication Tec...

TECH DATA, A TD SYNNEX COMPANY

Tech Data Corporation was an American multinational distribution compa...

M. TECH SOLUTIONS (I) PVT. LTD.

M.Tech is a leading cyber security and network performance solutions ...