Indian IT Hardware : Covid Did Not Spare IT

By MYBRANDBOOK

The Indian IT hardware industry too had to bear the brunt of the pandemic and all its leading segments demonstrated a sharp decline in business

The Covid pandemic did not spare the Indian IT hardware industry either. The sector showed a decline of 19% during the last year on account of sharp decline in PC, storage, server and printer business.

While the PC industry showed a decline of 7.2%, the server market plunged 14.3%, the external storage market degrown by 21.8% and the printer market demonstrated a decline of 19.1% on account of the Covid impact.

Indian PC Business

The Indian traditional PC market that includes notebooks, laptops, desktops and workstation, had to face the brunt of the Covid pandemic in the year 2020. The industry declined 7.2% in the year 2020 to ship 10.2 million units as against 11 million units for the year 2019. The Covid-induced movement restrictions and crippled supply chain can be attributed to this decline as vendors struggled to deliver shipments at the demanded time at their customers.

In the last quarter of 2020, the India PC market, according to IDC, witnessed shipments growing by 27.0% year-over-year. 2.9 million PCs were shipped in 4Q20 (Oct-Dec), with notebooks growing 62.1% YoY to contribute more than three-fourths of total shipments. The growth driver continues to be the demand from e-learning and remote working, leading to a 74.1% and 14.1% annual growth in the consumer and enterprise segments, respectively.

3.4 million units shipped during the quarter, as the demand for e-learning and remote working remained strong, resulting in 3Q20 being the biggest quarter in the last seven years in India. Although the commercial segment had very few government and education projects, the consumer segment recorded its biggest quarter ever with 2.0 million shipments, growing 41.7% YoY and 167.2% from the previous quarter.

Schools and colleges continued to function virtually, leading to a surge in demand for consumer notebooks, especially in large cities. Despite the supply challenges, vendors were able to stock up for the upcoming online festivals. However, the demand for notebook PCs remains much higher than the current supply, which is likely to lead to another strong quarter of shipments in 4Q20 (Oct-Dec). New entrants like Xiaomi and Avita were able to leverage this opportunity but remained outside of the top five companies in the consumer segment. Apple shipments also grew 19.4% YoY as it ended its biggest quarter of shipments in the country.

In the commercial segment, enterprises continued investing in PCs under their business continuity planning to manage their remote working requirements. However, the volume of key big deals has come down in this second wave of enterprise buying as compared to initial orders in 2Q20.

This led to a marginal 3.1% YoY growth in the overall enterprise segment. Notebook shipments grew at a strong 70.1% YoY as enterprises preferred them over desktops. SMBs resumed their purchases after taking a slight pause, as business operations started for most of the sectors with a relaxation in the lockdown restrictions. Shipments to this segment grew 5.5% YoY in 3Q20. However, this growth can also be attributed to channel procurement for better control over inventories amid the uncertain supply situation in the ecosystem.

Notebooks recorded a -16.8% decline in Q1 due to significant YoY contractions in the consumer and education segments. The private sector, however, posted much better results with companies advising their employees to work from home in March. In anticipation of an upcoming lockdown, many businesses increased their orders for notebooks, which resulted in a 7.1% YoY increase for this segment. The growth would have been even higher, if not for supply constraints which affected the industry in February and March and caused some of the orders to be delayed until 2Q20. The desktop category had relatively better inventory since most of it is assembled in India but saw a decline in demand and contracted -15.9% YoY in the first quarter of 2020.

2020 ended as the biggest year for notebooks with 7.9-million-unit shipments during the year. Notebook shipments grew by 6.0% in 2020. However, if we exclude the mega ELCOT deal, notebooks witnessed an impressive 34.3% YoY growth this year. Had the industry not been challenged by the component shortages, notebook shipments could have been much higher during the year. Contrary to this, desktop shipments saw a decline of 33.2% in 2020 as companies reduced their spending on fixed computing devices and preferred mobile devices to manage their operations remotely.

Top Players

Dell Technologies replaced HP for the top position in the overall PC market, as its shipments grew 57.1% YoY in 4Q20. The vendor also led the commercial segment with a share of 32.7% resulting in 15.2% YoY growth a despite decline in the commercial segment during 4Q20. Dell’s consumer shipments registered an impressive 159.1% YoY growth and maintained the lead for the second position in the category.

HP Inc. secured the second position with a 26.7% share with 8.8% YoY growth in 4Q20. HP remained the leader for the full year of 2020. Also, HP maintained its lead in the consumer segment as its shipments grew 47.3% from the same quarter a year ago. However, supply constraints restricted its growth in the commercial segment.

Lenovo slipped to the third position as its share dropped to 18.4% in 4Q20 from 21.7% in 3Q20. Strong momentum in its SMB and consumer segments helped the vendor to register 3.7% YoY growth in 4Q20.

Acer Group retained the fourth position with an 8.5% market share in 4Q20. However, the vendor registered an 11.0% decline in its overall shipments, mainly because of its heavy reliance on desktops, which fell 36.9% from the same time a year ago.

ASUS maintained the fifth position with a share of 6.4% as it grew an impressive 183.6% YoY in 4Q20. Its VivoBook 15, VivoBook 14 and TUF Gaming models continued to be the frontrunner in its growth. Also, a balanced portfolio in the online and offline channels helped the brand to sustain this growth.

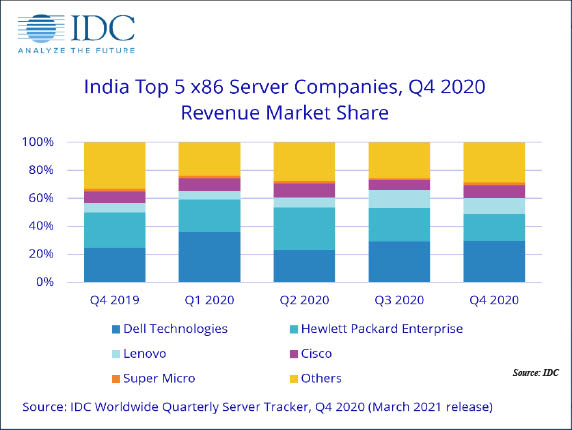

Server Market

Indian server market too saw a big plunge in the year 2020 marred by Covid related challenges. The segment posted revenues of $1051.3 million in 2020 as against $1228 million in 2019 showing a decline of 14.3%.

As per IDC, the overall server market in India witnessed a year-over-year (YoY) decline of 11.2% in terms of revenue to reach $266.1 million in Q4 2020 (Oct-Dec) versus $299.6 million in Q4 2019. The x86 server market contribution grew to 92.9% in terms of revenue, a growth of 4.8 percentage points over last year same quarter. The highest contribution in the x86 market mainly came from the professional services, telecommunications, and manufacturing verticals. In the professional services vertical, original design manufacturers (ODM) and new-age IT companies witnessed positive YoY growth with respect to the server spend. At the processor brand level, AMD witnessed YoY revenue growth of 4.7 percentage points claiming a revenue share of 8.4% at the end of Q4 2020.

The x86 server market in terms of revenue declined YoY by 6.3% to reach $247.2 million in Q4 2020 from $264.0 million in Q4 2019. The contribution largely came from the custom-built server category with revenue growth of 28.7% YoY. Hyperscalers continues to spend towards building robust data centers and support the global and local customer demands. The General-purpose server revenue declined by 13.4% due to the weakening demand across different industries. During Q4 2020, verticals such as utilities, resource industries, and securities and investment services witnessed the highest YoY growth in terms of revenue at 331.5%, 218.7%, and 160.6% respectively.

The non-x86 server market declined YoY by 47.1% to reach $18.9 million in revenue in Q4 2020. IBM continues to dominate the market accounting for 49.4% of revenue share, during Q4 2020 with a revenue of $9.3 million. HPE came at second position followed by Oracle with a revenue share of 27.8% and 8.3% respectively.

In Q4 2020, Dell Technologies emerged as the top vendor in the India x86 server market with a revenue share of 29.6% and a revenue of $73.1 million. Top three verticals for Dell Technologies were professional services, banking, and discrete manufacturing. HPE came at second spot with a revenue share of 19.5% and a revenue of $48.2 million. Key verticals for HPE were telecommunications, discrete manufacturing, and professional services. At number three is Lenovo with a revenue share of 10.9% and a revenue of $27.0 million. Cisco came in fourth accounting for a revenue share of 9.1% and a revenue of $22.6 million.

In Q3, the server market in India witnessed a year-over-year (YoY) growth of 0.3% in terms of revenue to reach $281.1 million versus $280.1 million in Q3 2019. The x86 server market contribution had grown to 91.2% in terms of revenue, a growth of 5.9 percentage points over last year’s same quarter. This contribution to the x86 market mainly came from professional services, telecommunications, and banking verticals. In the professional services vertical, global hyperscaler spend was directed towards building infrastructure to support business continuity operations of end customers whereas telecommunication spend was seen towards building and modernizing their network. Banks continue to spend on compute, supporting the upsurge of digital transactions and on-going digitalization projects.

The x86 server market in terms of revenue grew YoY by 7.3% to reach $256.4 million in Q3 2020 up from $239.0 million in Q3 2019. The growth largely came from the custom-built server category with revenue growth of 18.3% YoY. Hyperscalers were seen spending on infra to build capacity and expanding their datacenter footprint across various availability zones. The general-purpose server witnessed revenue growth of 4.5% due to the spending coming from very large customers across different industries. On the other hand, small and medium businesses, and large businesses failed to show signs of recovery caused due to the pandemic. During Q3 2020, verticals such as insurance, securities and investment services, and process manufacturing witnessed the highest YoY growth in terms of revenue at 201.5%, 137.5%, and 107.4% respectively.

The non-x86 server market declined YoY by 40.1% to reach $24.7 million revenue in Q3 2020. IBM continues to dominate the market accounting for 74.4% of revenue share during Q3 2020 with a revenue of $18.4 million. Oracle came at second position followed by Hewlett Packard Enterprise (HPE) with a revenue share of 20.8% and 4.8% respectively.

In Q2 the server market in India witnessed a year-over-year (YoY) decline of 22.3% in terms of vendor revenue to reach $272.0 million versus $350.2 million in Q2 2019. In Q1 also, the server market showed a decline of 22.1% in terms of revenue to reach $232.1 million versus $298.0 million in 1Q2019.

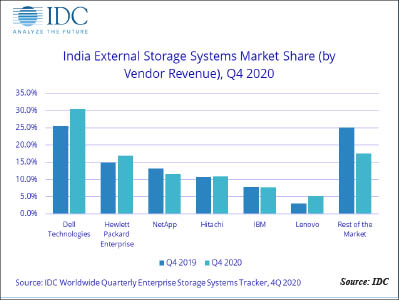

External Storage

The Indian external storage market in the year 2020 plunged 21.8% to post revenues of $308.6 million on account of the cautious approach of the customers during the pandemic hit year.

In Q4 2020, India’s external storage market witnessed a decline of 15.6% year-over-year (YoY) by vendor revenue and stood at $77.1 million. The majority of the YoY decline in storage spending was due to decreased spending from banking organizations, while manufacturing, central government and security, and investment services saw a growth in Q4 2020. The full year decline for the external storage market in India during 2020 (Jan-Dec) was 21.8%.

The growth of All-Flash Arrays (AFA) is evident across verticals with a contribution of 39.6% to the overall external storage systems market in Q4 2020. BFSI, professional services, manufacturing, and government verticals were the major contributors to AFA demand in Q4 2020. Stronger uptake of NVMe-based flash arrays is witnessed due to significant performance benefits with negligible cost differences. In the coming years, enterprises would prefer NVMe-based flash arrays as de facto storage media for all the production workloads.

All the Storage Class segments saw a sharp YoY decline in Q4 2020. Entry storage and high-end storage segments witnessed a strong YoY decline compared to midrange systems in Q4 2020. The impact of Entry storage is due to decreased storage demand from SMB and enterprises for their non-core applications.

Enterprises are investing in the modernization of applications/Infrastructure, seamless movement of data across multiple clouds, AIOps for managing infrastructure platforms, and security to be digitally resilient. Organizations are looking for trusted advisors and not standalone technology deployment partners to enable them to be future-ready.

In Q3 2020, India’s external storage market witnessed a decline of 14.8% year-over-year and stood at $79.9 million. In Q2 the revenue was $63.8 million showing a y-o-y degrowth of 36.8%. In Q1 too there was a sharp decline of 20.6% Year-over-Year (YoY) by vendor revenue and the industry posted a revenue of $ 87.8 million.

Dell Technologies continued to be the market leader in the external storage systems market with a 30.4% market share by vendor revenue, followed by HPE with a 16.9% market share.

Printer Market

For the CY2020 (Jan-Dec 2020), the overall HCP market declined by 19.1% mainly due to the laser segment (including copiers) which declined by 28.5%, following the commercial market’s struggle to resume operations during the COVID-19 crisis. The laser copier market dropped by 44.9% owing to weak corporate and Government demand. The inkjet market declined by 9.2%, due to the surge in demand from the Home segment. CY2020 observed high demand for Wi-Fi and ink tank printers which could be met partially as vendors struggled to furnish enough stock. Vendors were challenged by the limited manufacturing capacity following the global surge in demand for Wi-Fi ink tank printers.

For the CY2020 (Jan-Dec 2020), the overall HCP market declined by 19.1% mainly due to the laser segment (including copiers) which declined by 28.5%, following the commercial market’s struggle to resume operations during the COVID-19 crisis. The laser copier market dropped by 44.9% owing to weak corporate and Government demand. The inkjet market declined by 9.2%, due to the surge in demand from the Home segment. CY2020 observed high demand for Wi-Fi and ink tank printers which could be met partially as vendors struggled to furnish enough stock. Vendors were challenged by the limited manufacturing capacity following the global surge in demand for Wi-Fi ink tank printers.

Indian Hardcopy Peripherals (HCP) market recorded its best Q4 till date in terms of unit shipments. As the country opened further during the festival season and vendors partially resolved their supply issues following a global surge in demand, India’s HCP market witnessed a growth of 4.0% quarter-over-quarter (QoQ) during 4Q20 (Oct-Dec 2020). The market registered shipments of 0.95 million units during the quarter posting a growth of 19.7% year-over-year (YoY), according to the latest IDC Worldwide Quarterly Hardcopy Peripherals Tracker, 4Q20.

In the inkjet segment, vendors continued to face supply challenges during the beginning of the quarter. However, the situation improved as the manufacturing hubs in China and Southeast Asian countries increased their capacity to meet the global surge in demand for inkjet printers from the Home segment. Following this, the inkjet segment noted a YoY growth of 38.8%. Within inkjet printers, the ink tank printer segment grew steadily following improved availability and the pent-up consumer demand owing to continued work from home and e-learning for students.

The laser printers’ segment (including copiers) recorded a YoY growth of 3.8% at the back of laser printers (excluding copiers) as multiple delayed orders from the previous few quarters were executed in 4Q20. The laser copier segment, however, witnessed a YoY decline of 27.5% following muted demand from Corporates.

“In the commercial segment, the demand situation improved from a QoQ perspective as certain segments, primarily jobbers and SMBs/SOHOs, resumed full-time operations. However, demand from large corporates continued to be muted as the offices remain closed. 4Q20 witnessed increased activity from the Government as it released several tenders following directives from Ministry of Finance to other ministers and public sector enterprises to exhaust their planned budget for capital expenditure (CAPEX),” says Bani Johri, Market Analyst, IPDS, IDC India.

Leading Players

HP Inc. (excluding Samsung) maintained its leadership in the overall HCP market with a share of 40.2% and a growth in shipment of 22.1% YoY. The growth was primarily led by the inkjet segment wherein HP grew by 51.7% YoY and captured a market share of 33.8%, occupying the 2nd position, as it smoothened its supply and logistics issues to cater to the increased demand. HP recorded an almost equal growth in both the segments – ink tank and Ink cartridge-based printers. In the laser printer segment (excluding laser copiers), it grew by 2.1% YoY and continued to maintain its number #1 position with a 55.8% market share.

HP Inc. (excluding Samsung) maintained its leadership in the overall HCP market with a share of 40.2% and a growth in shipment of 22.1% YoY. The growth was primarily led by the inkjet segment wherein HP grew by 51.7% YoY and captured a market share of 33.8%, occupying the 2nd position, as it smoothened its supply and logistics issues to cater to the increased demand. HP recorded an almost equal growth in both the segments – ink tank and Ink cartridge-based printers. In the laser printer segment (excluding laser copiers), it grew by 2.1% YoY and continued to maintain its number #1 position with a 55.8% market share.

Epson replaced Canon to occupy the 2nd position in the overall HCP market with a market share of 26.2% while registering a YoY growth of 14.9%. In the inkjet segment, Epson replaced HP to regain its top position in the market with a share of 41.1%. This comes primarily at the back of Epson having resolved the supply issues it was facing previously in 3Q20.

Canon recorded a YoY growth of 34.6% and occupied the 3rd position in the overall India HCP market, capturing a unit market share of 22.7%. In the inkjet segment, Canon observed a YoY growth of 63.9% at the back of its increased online presence and lucrative end-user schemes. In the laser segment (including laser copiers) Canon maintained its 2nd position with a market share of 25.0% with a heavy dependency on entry-level mono printers, primarily LBP 2900B. In the laser copier segment, although Canon declined by 33.3% YoY, yet it continued to lead the copier market with a 32.6% market share because of its wide product portfolio and a strong foothold in the corporate segment.

Happiest Minds brings in an innovative GenAI chatbot

Happiest Minds Technologies has announced the new GenAI chatbot - ‘hAPPI...

Government mandates encryption for CCTV cameras to ensure netw

In the wake of issuing an internal advisory on securing CCTV cameras at g...

TRAI recommends allowing only Indian entities to participate i

The Telecom Regulatory Authority of India (TRAI) has recommended that onl...

Galaxy AI is available on more devices with Samsung One UI 6.1

Samsung has expanded the range of smartphones to which One UI 6.1 and Gala...

Disney+ Hotstar wins the Best OTT Platform of the year

Film Critics Guild and Group M Motion Entertainment, in collaboration with

Miss World 2024: Krystyna Pyszková of the Czech Republic wins

Krystyna Pyszková of the Czech Republic has been crowned as the 71st Miss

Brillio appoints Ashish Singh to its Board of Directors

Brillio has announced that Ashish Singh has been appointed to the company�

JSW One Platforms ropes in Dr Ranjan Pai as Independent Direct

JSW One Platforms, part of US$23 billion JSW Group has appointed Dr Ranjan

Forcepoint positions itself as a trusted protector of sensitiv

To help SMEs and SMBs use the SASE/SSE framework and scale both in terms of

CommScope celebrates its 25 years of legacy in India by contin

A strong brand must also reflect the company values and speak exactly what

HP launches first laptop in India with Microsoft CoPilot butto

HP has launched sleek and stylish Envy x360 14 laptops in India which beco

OnePlus debut its Nord CE4 smartphone

OnePlus Nord CE4 continues the trend of attention-grabbing design with two

DRUVA SOFTWARE PVT. LTD.

STERLITE TECHNOLOGIES LTD.

GLOBUS INFOCOM LTD.

SAMRIDDHI AUTOMATIONS PVT. LTD.

Technology Icons Of India 2023: Harsh Jain

Harsh Jain is an Indian Entrepreneur, the co-founder and CEO of the In...

Technology Icons Of India 2023: Ashish Kumar Chauhan

Ashish works as the CEO of the National Stock Exchange (NSE). He is al...

Technology Icons Of India 2023: Ajit Balakrishnan

The Company markets specific channels, community features, local langu...

C-DOT enabling India in indigenous design, development and production of telecom technologies

An autonomous telecom R&D centre of Government of India, Center of Dev...

STPI encouraging software exports from India

Software Technology Parks of India (STPI) is an S&T organization under...

STPI encouraging software exports from India

Software Technology Parks of India (STPI) is an S&T organization under...

TEXONIC INSTRUMENTS

Texonic has carved a niche for itself in the Technology Distribution i...

INTEGRA MICRO SYSTEMS PVT. LTD.

Integra is a leading provider of innovative hi-technology products an...

SUPERTRON ELECTRONICS PVT. LTD.

Supertron deals in servers, laptops, components, accessories and is a...