Despite the massive disruption brought by COVID-19, fintech companies remain bullish on the long-term growth prospect of the industry.

By MYBRANDBOOK

The landscape of banking and financial sector has undergone a phenomenal transformation since 2008 Global Financial Crisis (GFC), owing to financial technology firms, popularly known as ‘FinTechs’. Both as creative disruptors and facilitators, FinTechs have contributed to the modern banking and financial sector through various channels including cost optimisation, better customer service and financial inclusion. FinTechs have played an important role in unbundling banking into core functions of settling payments, performing maturity transformation, sharing risk and allocating capital.

In India, FinTechs and digital players could function as the fourth segment of the Indian financial system, alongside large banks, mid-sized banks including niche banks, small finance banks, regional rural banks and cooperative banks. This segment has the potential to fundamentally transform the financial landscape where consumers will be able to choose from broader set of alternatives at competitive prices, and financial institutions could improve efficiency through lower costs.

Market Size

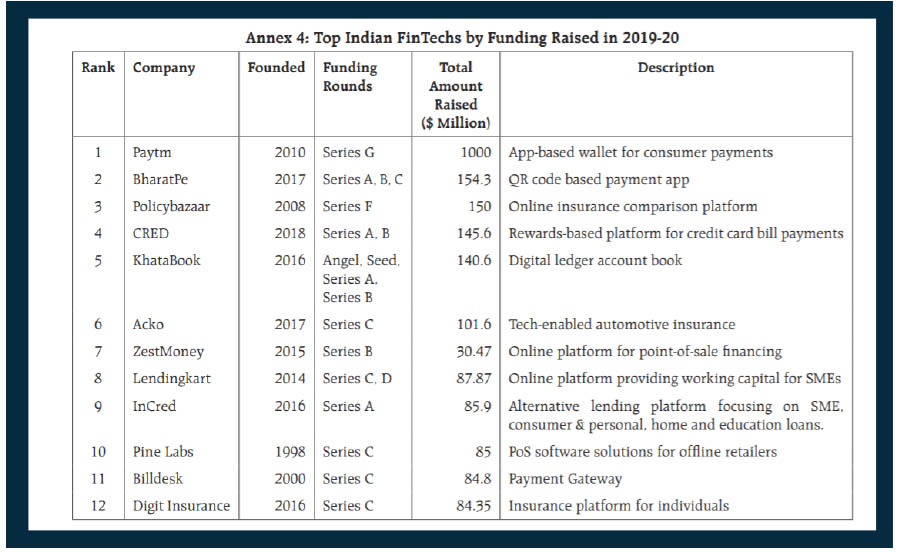

India has emerged as the fastest growing FinTech market and the third largest FinTech ecosystem in the world. Today, we carry out complex financial actions like sending or receiving money, paying bills, buying goods and services, purchasing insurance, trading on stock markets, opening bank accounts and applying for personal loans online using smartphones, without ever physically interfacing with a bank employee. As per the Government’s own estimate, India has the opportunity of a digital payments market of $ 1 trillion by 2023. It recorded 3,435 crore digital payments in the year 2019-20. As per data available, Indian Fintech firms have raised around $3.5 billion and PayTm alone has raised more than $1 billion. And of all the funding, top 10 fintech firms have accounted around 67% of total funds.

Fintech Landscape and growth Drivers

Over the last decade, the Indian FinTech ecosystem has witnessed a plethora of innovations. A report by the Reserve Bank of India (RBI) says there are more than 4680 fintech firms in the country having various business models. These fintech firms are primarily based out of Delhi-NCR, Mumbai-Pune corridor and Southern Indian cities ranging from Bengaluru to Chennai to Hyderabad and Kochi.

The growth of the fintech firms and the availability of their services in the Indian market can be attributed to the massive penetration of smartphones and internet across the length and breadth of the country. Besides, a higher population of young population is also pushing the adoption of new-age and tech driven financial services, Government policies like demonetization and natural incidences like Covid also forced the population to use digital way of banking thus helping the industry grew phenomenally in last few years.

Digital Payments

In the overall fintech space, Digital payments has been the poster boy since the beginning. In recent years, we have witnessed a plethora of exciting innovations like UPI, biometric payments, e-wallets initiations by banks, BharatQR code, and sound-wave-based payment technologies. One of the primary reasons can be attributed to the forward-thinking of central & state governments and Reserve Bank of India for successfully bringing a digital payment revolution in India.

The Indian payments landscape has been revolutionized by the regulators and the central bank’s proactive initiatives such as UPI. India has emerged as one of the most exciting markets for digital payments across the world. As per RBI data, last year, home-grown payment networks (RuPay and UPI) took the lion’s share of the total digital transactions, i.e., 65%, showcasing how their efforts have been in the right direction for achieving targets.

Recently, tech giant Google wrote to the US Federal Reserve, praising the UPI model that has taken the digital payment space in India by storm and recommended creating similar open-payment architecture in the US. Furthermore, With UPI going global, it sets up the stage for the FinTech players as they have already started receiving queries from international financial institutions, banks, and governments. This has further opened immense opportunities for FinTech players who can share their technology with foreign countries like China, the Philippines, Sri Lanka, Bangladesh, and other SEA countries.

The digital payments segment of Fintech has so far seen investments close to $3 billion and some major names in this space include PayTm, PhonePe, BharatPe, BillDesk and Khatabook.

Neobanking

The first wave of disruption in financial services was led by digital payment startups, followed by digital lending, wealth management, and InsurTech startups. However, in the last couple of years or if we call it “FinTech 2.0,” a new age fintech category – Neobanks - took birth and has so far taken the industry by storm. These are purely digital-only financial service providers and offer services like fully digitized account opening, free debit cards, instant payments, personal finance advisory, cash flow analysis & projections, GST-compliant invoicing, and accounting integration. As per the MEDICI report, there are about 15 neobanks in India including SBI Yono, Niyo, Razorpay, Neo, Open, Kotak 811 etc.

With FinTech segments like payments and digital lending getting overcrowded, investors’ interest has shifted towards India’s Neobanking. The total funding raised by Indian Neobanks so far totals $139.8 Mn. This does not include $93 million raised by Razorpay since 2019, a part of which will fund their newly launched Neobanking initiative. In their efforts to become a part of the next wave of FinTech innovation, venture capital & private equity investors have started to invest heavily in Neobanking startups.

Digital Lending

Digital lending FinTechs are targeting the unmet demand from Indian MSMEs as well as consumers for credit. Many banks in India have so far focused on highly creditworthy segments primarily due to a lack of credit history of others. The traditional ways of banking approve only ~25 to 40% of the loan applications. However, with access to more data for credit scoring such as transaction, behavior, app-based data, location information, social data, and more, these new lending models aim to increase this threshold by an additional 10–15%, which is a huge market opportunity. From a small segment a few years ago, India now has over 338 lending startups. The acquisition of Mumbai-based consumer lending platform PaySense by digital payments provide PayU at a valuation of $185 million, further brought the spotlight to the potential of digital lending in India. Several new models of digital lending have emerged, such as DMI Finance offering FinTech startups API access to sandboxes, thus helping them develop bespoke financial products and Apollo Finvest positioning themselves as ‘AWS for Lending’ by enabling partners to offer digital loan products to their end-customers through APIs. In consumer credit, the urban population is likely to leverage FinTech lending services to avoid heavy documentation. The rural population (which is new to credit) can benefit from alternative credit scoring mechanisms to avoid loan sharks. This would provide access to a market with over 300 million unbanked households. Hence, the use of identity, authentication, credit score, job eligibility, and social data to generate ratings for various use cases is likely to draw more attention in the near term. Some of the leading players in this space include Lazypay, Capital Float, Zest, eMudhra etc.

WealthTech

This is one more area where finance is being blended with technology to offer modern, customized and wealth related services including investment, broking, mutual funds etc. These firms help in democratization of investment advisory services, where wealth managers are leveraging technology to offer low-cost investment advisory to mass segments. A major category of wealthtech falls under Robo-advisory- a sort of advisory services primarily offered using artificial intelligence over digital format.

Robo-Advisors: Robo-advisory in India is rapidly evolving. We are seeing startups going beyond Mutual Fund distribution to offering digitized, long-term financial planning. They are using algorithms and artificial intelligence to understand the goals and aspirations of users better and provide them with personalized advice rather than just offering a generic portfolio. As more and more millennials pick up stock market investing and other investment avenues, financial literacy is also improving, leading to a mature outlook towards aspects such as financial life goals and retirement planning.

The services of these platforms range from automated plans, goal-based asset allocation, and end-to-end advisory based on information taken from the client. Today, not only startups but also established financial advisory services, such as Birla, Bajaj Capital, ICICI Securities, and Sanctum Wealth Management, are optimistic about the future of robo-advisory. The competition in robo-advisory is resulting in the expansion of the WealthTech market.

Some of the major names in Wealthtech include Zerodha, Upstox, Bankbazaar, ETMoney, Groww and FundsIndia.

Zerodha is the largest firm among all these and is valued at over $ 1 billion.

InsurTech

InsurTech landscape is quite nascent in India. The current insurance penetration is quite low, i.e., 2.76% in life insurance and 0.93% in non-life insurance compared to the global average of 6.5%. ‘Lack of customer trust’ remains the key challenge facing the InsurTech segment, and so far, industry players have found it as a hard nut to crack. The current InsurTech space in India is being dominated by few new-age insurers like Toffee, Digit, and Acko with their ability to attract and popularity among millennials.

This space has seen investments upto $445 million and some of the big names include Policy bazaar, Coverfox, Digit and Acko.

Besides the core financial services segments, aome other areas like agriculture, healthcare, and housing have started leveraging technology and finance in order to provide easier access to their services to the vast population in India. This is leading to the rise of AgriTech, HealthTech, and PropTech startups that are disrupting traditional ways of doing business in three industries that facilitate the nation’s most vital necessities—food, healthcare, and shelter for citizens

InterGlobe’s Rahul Bhatia and C.P. Gurnani together announce

In a move that is set to transform the AI landscape, Rahul Bhatia, Group M...

Download masked Aadhaar to improve privacy

Download a masked Aadhaar from UIDAI to improve privacy. Select masking w...

Sterlite Technologies' Rs 145 crore claim against BSNL rejecte

An arbitrator has rejected broadband technology company Sterlite Technolog...

ID-REDACT® ensures full compliance with the DPDP Act for Indi

Data Safeguard India Pvt Ltd, a wholly-owned subsidiary of Data Safeguard ...

Salman Khan trolled for singing with B Praak at Anant Ambani's

To celebrate Mukesh Ambani's youngest son Anant Ambani’s 29th birthday

Disney+ Hotstar wins the Best OTT Platform of the year

Film Critics Guild and Group M Motion Entertainment, in collaboration with

SISL elevates Ankita Wadhawan as CEO—End User Computing

The IT service provider, SISL in a LinkedIn post announced the elevation

InfoVision appoints Radhika Venkatraman to its Advisory Board

Global digital services company, InfoVision has announced the appointment

Kaspersky securing the digital landscape by offering enhanced

Kaspersky is a thought leader in cybersecurity that identifies threats by p

HPE’s transformation into an edge-to-cloud company is its un

Hewlett Packard Enterprise (HPE) is driving towards one customer experience

Canon India Introduces 4K Remote PTZ Camera Controller & 4K In

Canon India, a leading company in digital imaging solutions, further solidi

Dell Technologies launches the new consumer and gaming portfol

Dell Technologies has unveiled its newest line of AI-enabled consumer PCs

CENTRE FOR DEVELOPMENT OF TELEMATICS

BEETEL TELETECH LTD.

HIMACHAL FUTURISTIC COMMUNICATIONS LTD.

WIPRO LTD.

Technology Icons Of India 2023: Lt Gen (Dr.) Rajesh Pant (Retd.)

LT Gen(Dr.) Rajesh Panth (Retd.), National cyber security coordination...

Technology Icons Of India 2023: C P Gurnani

CP Gurnani (popularly known as ‘CP’ within his peer group), is the...

Technology Icons Of India 2023: Sachin Bansal

Sachin Bansal’s fintech startup, Navi Technologies, simplifies loan ...

ECIL continues to keep India ahead in the growth of Information Technology and Electronics

ECIL played a very significant role in the training and growth of high...

BSE provides highly secure, efficient and transparent market for trading

BSE (formerly known as Bombay Stock Exchange Ltd.) is Asia's first & t...

Aadhaar: Architecting the World's Largest Biometric Identity System

The Unique Identification Authority of India (UIDAI) is a statutory au...

INGRAM MICRO INDIA PVT. LTD.

Ingram Micro India, a large national distributor offers a comprehensiv...

SUPERTRON ELECTRONICS PVT. LTD.

Supertron deals in servers, laptops, components, accessories and is a...

TECHNOBIND SOLUTIONS PVT. LTD.

TechnoBind’s business model is focused on identifying and partnering...

Limited")