Telecom Services : Bad Times Are Over

By MYBRANDBOOK

Though the telcos are still battling revenue and policy issues, a consolidated market with a humongous growth potential and 5G are expected to bring back the lost glory to the sector

The Indian telecommunications industry, the second largest in the world in terms of subscriber numbers, made some positive moves in 2019. It did some course corrections in the later part of the year by modifying the tariff structure that increased ARPU for the operators. The ARPU of operators, baring Reliance Jio, was on a consistent southward move since the Mukesh Ambani-led firm entered into the Indian telecom services space. The sector also saw quite some good investments from all the operators during the last fiscal that helped them expanding their reach in terms of service offerings as well as strengthening their network infrastructure.

Industry dynamics

India’s telecom market which combines wireless, wireline and internet services, is currently the world’s second-largest telecommunications market with a subscriber base of 1.20 billion and has registered strong growth in the last decade and half. Gross revenue of the telecom sector stood at Rs 185,000 crore in FY20 till the end of December 2019.

Total Telephone Subscribers

The number of telephone subscribers in India at the end of March 2020 reached 1,177.97 million showing a monthly decline of 0.24% from 1,180.84 million at the end of Feb-20. Urban telephone subscription decreased from 661.23 million at the end of Feb-20 to 656.46 million at the end of Mar-20, however the rural subscription increased from 519.62 million to 521.51 million during the same period. The monthly growth rates of urban and rural telephone subscription were -0.72% and 0.36% respectively during the month of Mar-20.

The overall Tele-density in India decreased from 87.66 at the end of Feb-20 to 87.37 at the end of Mar20. The Urban Tele-density declined from 143.59 at the end of Feb-20 to 142.31 at the end of Mar-20. Rural Tele-density increased from 58.61 at the end of Feb-20 to 58.79 at the end of Mar-20. The share of rural and urban subscribers in total number of telephone subscribers at the end of Mar-20 was 44.27% and 55.73% respectively.

Wireless Subscribers: Total wireless subscribers (2G, 3G & 4G) decreased from 1,160.59 million at the end of Feb-20 to 1,157.75 million at the end of Mar-20, thereby registering a monthly decline rate of 0.24%. Wireless subscription in urban areas decreased from 643.24 million at the end of Feb20 to 638.48 million at the end of Mar20 however wireless subscription in rural areas increased from 517.34 million at the end of Feb-20 to 519.27 million at the end of Mar-20. Monthly growth rates of urban and rural wireless subscription were -0.74% and 0.37% respectively.

The Wireless Tele-density in India decreased from 86.15 at the end of Feb-20 to 85.87 at the end of Mar-20. The Urban Wireless Teledensity declined from 139.68 at the end of Feb-20 to 138.41 at the end of Mar-20, however, Rural Wireless Tele-density increased from 58.35 to 58.54 during the same period. The share of urban and rural wireless subscribers in total number of wireless subscribers was 55.15% and 44.85% respectively at the end of Mar-20.

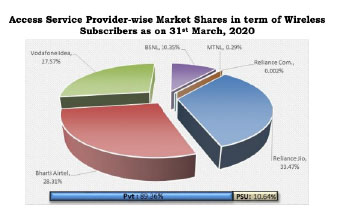

As on 31st March, 2020, the private access service providers held 89.36% market share of the wireless subscribers whereas BSNL and MTNL, the two PSU access service providers, had a market share of only 10.64%.

Wireline Subscribers: Landline or wireline subscribers decreased from 20.26 million at the end of Feb-20 to 20.22 million at the end of Mar-20. Net decline in the wireline subscriber base was 0.04 million with a monthly decline rate of 0.20%. The share of urban and rural subscribers in total wireline subscribers were 88.91% and 11.09% respectively at the end of Mar-20.

Wireline Subscribers: Landline or wireline subscribers decreased from 20.26 million at the end of Feb-20 to 20.22 million at the end of Mar-20. Net decline in the wireline subscriber base was 0.04 million with a monthly decline rate of 0.20%. The share of urban and rural subscribers in total wireline subscribers were 88.91% and 11.09% respectively at the end of Mar-20.

The Overall Wireline Tele-density remained same i.e. 1.50 at the end of Mar-20 as it was at the end of Feb-20. Urban and Rural Wireline Tele-density were 3.90 and 0.25 respectively during the same period. • BSNL and MTNL, the two PSU access service providers, held 58.47% of the wireline market share as on 31st March, 2020.

Broadband Subscribers : The number of broadband subscribers increased from 681.11 million at the end of Feb-20 to 687.44 million at the end of Mar-20 with a monthly growth rate of 0.93%. Top five service providers constituted 98.99% market share of the total broadband subscribers at the end of Mar-20. These service providers were Reliance Jio Infocomm Ltd (388.39 million), Bharti Airtel (148.57 million), Vodafone Idea (117.45 million), BSNL (24.50 million) and Atria Convergence (1.61 million).

Industry Snapshot : By the end of March 2020, India had a total subscriber base of 1178 million of which around 90% is with the three private operators – Reliance Jio, Bharti Airtel and Vodafone Idea. The two PSU telcos – BSNL and MTNL – cater to the rest 10% subscribers.

While by the end of March 2019, Vodafone Idea was the biggest operator, owing to their merger, with 418 million subscribers, in 2020, Jio displaced Vodafone Idea to capture the top position with 387 million subscribers. The Reliance Industries owned firm has consistently been adding subscribers to its kitty since launch on account of its competitive and simplified tariff structure. Also, the operator offers 4G data services from the very first day of its launch to all of its subscribers.

Bharti Airtel which was the second largest telecom operator in 2019 with 340 million subscribers, could manage to hold its position in the current fiscal too with 328 million customers. Vodafone Idea is placed at the third position with 319 million subscribers at the end of March 2020.

In terms of Indian wireless subscribers market share Reliance Jio has got the biggest pie of 33.47% followed by Bharti airtel with 28.31% and Vodafone Idea is having a market share of 27.57%. State-run telco BSNL has a market share of 10.35% of the total subscriber base where as MTNL has got 0.29% of the total subscribers.

In broadband, Jio too has got the lion’s share with 56.50% of the total subscriber base followed by Airtel with 21.61% and Vodafone Idea with 17.09%. BSNL commands a market share of only 3.56% of the total subscriber base of 687 million.

Major Developments

Major Developments

The liberal and reformist policies of the Government of India have been instrumental along with strong consumer demand in the rapid growth in the Indian telecom sector. The Government has enabled easy market access to telecom equipment and a fair and proactive regulatory framework, that has ensured availability of telecom services to consumer at affordable prices. The deregulation of Foreign Direct Investment (FDI) norms have made the sector one of the fastest growing and the top five employment opportunity generator in the country.

With daily increasing subscriber base, there have been a lot of investment and development in the sector. FDI inflow into the telecom sector during April 2000 – March 2020 totalled $ 37.27 billion according to the data released by Department for Promotion of Industry and Internal Trade (DPIIT). FDI cap in the telecom sector has been increased to 100 % from 74 %; out of 100 %, 49 % will be done through the automatic route and the rest will be done through the FIPB approval route.

Some of the developments in the recent past are:

• India had over 500 million active internet users as of March 2020.

• As of July 2019, India achieved 100 % digitisation of cable TV network.

• In August 2019, Reliance commercially launched Jio GigaFiber as a wired broadband service.

• As of August 2019, Jio’s IoT platform was ready to be commercially available from January 2020.

• In December 2019, Airtel disclosed its plans to invest $ 2.86 billion in its business as part of company’s annual target.

• As of January 2020, more than 542 banks were permitted to provide mobile banking services in India.

• In April 2020, Vodafone Group Plc infused Rs 1,530 crore ($ 217.05 million) in Vodafone Idea as accelerated payment to help the company manage its operations.

• In June 2020, Jio Platforms Ltd. sold 22.38 % stake worth Rs 1.04 trillion ($ 14.75 billion) to ten global investors in a span of eight weeks under separate deals, involving Facebook, Silver Lake, Vista, General Atlantic, Mubadala, Abu Dhabi Investment Authority (ADIA), TPG Capital and L. Catterton. This is the largest continuous fundraise by any company in the world.

Government Initiatives

The Government has fast-tracked reforms in the telecom sector and continues to be proactive in providing room for growth for telecom companies. Some of the key initiatives taken by the Government are as follows:

• In January 2020, Government of India allowed 100 % FDI in Bharti Airtel.

• The Government of India planned to roll out a new National Telecom Policy 2018 in lieu of rapid technological advancement in the sector over the past few years. The policy intended to attract investments worth $ 100 billion in the sector by 2022.

• The Department of Information Technology intends to set up over 1 million internet-enabled common service centres across India as per the National e-Governance Plan.

• FDI cap in the telecom sector has been increased to 100% from 74 %; out of 100 %, 49 % will be done through the automatic route and the rest will be done through the FIPB approval route.

• FDI of up to 100 % is permitted for infrastructure providers offering dark fibre, electronic mail and voice mail.

• The Government of India has introduced Digital India programme under which all the sectors such as healthcare, retail, etc. will be connected through internet

Road Ahead

Road Ahead

India’s telecom industry has been the poster boy of India’s global success story for quite a sometime and the industry offers a similar promise in the future years too. The new telecom policy announced in 2019 envisages investment of $100 billion in the telecom sector by 2022 and hopes to generate employment for 4 million people.

The over $20 billion investment in Jio Platforms by a plethora of global bigwigs including Facebook, Microsoft, Silver Lake, Vista, General Atlantic, Mubadala, Abu Dhabi Investment Authority (ADIA), TPG Capital and L. Catterton, is a classic example of India’s investment potential.

Revenue from the telecom equipment sector is expected to grow to $ 26.38 billion by 2020. The number of internet subscribers in the country is expected to double by 2021 to 829 million and overall IP traffic is expected to grow four-fold at a CAGR of 30 % by 2021. The Indian Government is planning to develop 100 smart city projects, and IoT will play a vital role in developing these cities.

The sheer size of the market, demographic advantages, and hunger for new technologies and services, are some of the key factors driving growth in all sort of telecom services across the country. As per TRAI data, Indian users consume more than 10 GB of data every month – highest in the world. It has also been observed that in last couple of years telecom operators’ revenue share from data business has grown significantly compared to voice business which has been the mainstay of their revenue for quite a long time. The same is expected to get another shot in the arm with the availability of 5G services in the coming years as a major chunk of revenue is expected from industrial sector on account of IoT, automation in Industry 4.0.

InterGlobe’s Rahul Bhatia and C.P. Gurnani together announce

In a move that is set to transform the AI landscape, Rahul Bhatia, Group M...

Download masked Aadhaar to improve privacy

Download a masked Aadhaar from UIDAI to improve privacy. Select masking w...

Sterlite Technologies' Rs 145 crore claim against BSNL rejecte

An arbitrator has rejected broadband technology company Sterlite Technolog...

ID-REDACT® ensures full compliance with the DPDP Act for Indi

Data Safeguard India Pvt Ltd, a wholly-owned subsidiary of Data Safeguard ...

Salman Khan trolled for singing with B Praak at Anant Ambani's

To celebrate Mukesh Ambani's youngest son Anant Ambani’s 29th birthday

Disney+ Hotstar wins the Best OTT Platform of the year

Film Critics Guild and Group M Motion Entertainment, in collaboration with

SISL elevates Ankita Wadhawan as CEO—End User Computing

The IT service provider, SISL in a LinkedIn post announced the elevation

InfoVision appoints Radhika Venkatraman to its Advisory Board

Global digital services company, InfoVision has announced the appointment

HPE Aruba Networking bridging the physical and digital worlds

The information technology industry is a critical component of the 21st cen

Cisco committed to help build trusted, resilient future for or

Cisco is delivering on its promise of the AI-driven Cisco Security Cloud to

Canon India Introduces 4K Remote PTZ Camera Controller & 4K In

Canon India, a leading company in digital imaging solutions, further solidi

Dell Technologies launches the new consumer and gaming portfol

Dell Technologies has unveiled its newest line of AI-enabled consumer PCs

STERLITE TECHNOLOGIES LTD.

SAMSUNG INDIA ELECTRONICS PVT. LTD.

SAFE SECURITY SERVICES PVT. LTD.

SECUREYE SERVICES PVT. LTD.

Technology Icons Of India 2023: Madhabi Puri Buch

Madhabi Puri Buch is the chairperson of the securities regulatory body...

Technology Icons Of India 2023: Roshni Nadar Malhotra

Roshni Nadar Malhotra is an Indian billionaire businesswoman and the c...

Technology Icons Of India 2023: Debjani Ghosh

Debjani Ghosh is the first woman president of NASSCOM (the umbrella bo...

INDIANOIL helps reach precious petroleum fuels to every nook and corner of the country

IndianOil, a diversified, integrated energy major with presence in alm...

C-DOT enabling India in indigenous design, development and production of telecom technologies

An autonomous telecom R&D centre of Government of India, Center of Dev...

STPI encouraging software exports from India

Software Technology Parks of India (STPI) is an S&T organization under...

ADITYA INFOTECH LTD.

Aditya Infotech Ltd. (AIL) – the technology arm of Aditya Group, is ...

SATCOM INFOTECH PVT. LTD.

Satcom Infotech Pvt. Ltd is a distribution houses in security in India...

B D SOFTWARE

BD Software is the distributor of IT security solutions in India. The ...

Limited")