Indian IT & ITeS Industry: Staring At A Brighter Future

By MYBRANDBOOK

While India’s IT & ITeS sector has always been a formidable force to reckon with, the COVID-induced digitalization will further its position, at domestic as well as global arena

The Indian IT industry is a crucial pillar of the country’s economy and contributes around 8% of the national GDP. The industry, a combination of India’s IT hardware, software services, BPM and ER&D employs, more than 4 million people and aims at contributing 10% of the nation’s GDP by 2025.

The IT services and BPM, the largest sector of the industry, continues to see solid growth and is being seen as the most favoured sourcing destination across the globe. The global sourcing market in India continues to grow at a higher pace compared to the IT-BPM industry. India is the leading sourcing destination across the world, accounting for approximately 55 % market share of the $ 200-250 billion global services sourcing business in 2019-20. Empowered with the largest IT talent pool in the world and competitive skilled-labour cost, the Indian IT & ITeS companies have expanded to more than 90 countries in the world and have set up over 1,000 global delivery centres.

Market Size

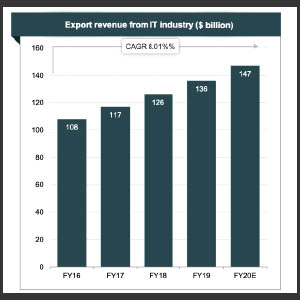

In FY 2019-20, the Indian IT-ITeS industry’s revenue was estimated at around $ 191 billion in FY20, growing at 7.7 % y-o-y. Of this, $147 billion is from export revenue and India’s domestic IT revenue is pegged at $44 billion at the end of March 2020 as per IBEF.

The IT & ITeS market in India is estimated to reach $ 350 billion by 2025, and ITeS is expected to contribute $50-55 billion to the total tally by the same period. On the same breath, it is also estimated that the country’s digital economy will reach $ 1 trillion by 2025. The cloud market in India is expected to grow three-fold to $ 7.1 billion by 2022 with the help of growing adoption of Big Data, analytics, artificial intelligence and Internet of Things (IoT) according to Cloud Next Wave of Growth in India report.

The IT & ITeS segment, the biggest among the Indian IT industry segments, is primarily based on exports and the same grew at 8% during FY20. The export business contributed to around 54% of the total revenue of IT&ITeS sector during the period.

The US has been the biggest importer of Indian IT exports and contributes around 62% of the total business followed by the UK with 17% exports.

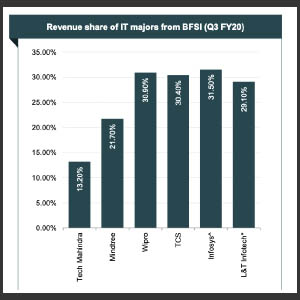

BFSI continues to be the biggest contributor to the IT & ITeS revenue with Infosys being the being leader in that space followed by Wipro, TCS and L&T Infotech. For all these players, more than 30% of their total revenue comes from BFSI business.

The business segment also saw lots of development during the last financial year.

In May 2019, Infosys acquired 75 % stake in ABN AMRO Bank’s subsidiary, Stater, for $ 143.08 million. In June 2019, Mindtree was acquired by L&T. In January 2020, Nippon Telegraph and Telephone, a Japanese tech company, announced its plans to invest a significant part of its $ 7 billion global commitment for data centres business in India over the next four years. In February 2020, TCS bagged a contract worth Rs 10,650 crore ($ 1.5 billion) from pharma company, Walgreens Boots Alliance.

The dynamism of this industry prompts industry watchers to predict that the vertical is expected to grow bigger in the coming days on account of growing number of players joining the race and massive digitalization drives in the businesses. Adoption of new technologies is expected to accelerate growth of the BFSI vertical. The need for undertaking investment in IT will also be required for gaining competitive advantage instead of solely reducing operational costs.

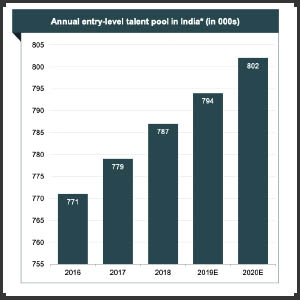

According to reports, the total number of employees grew to 1.02 million cumulatively for four Indian IT majors (including TCS, Infosys, Wipro, HCL Tech) as on December 31, 2019. Indian IT industry employed 205,000 new hires and had 884,000 digitally skilled talent in the last year.

Major Developments

Indian IT’s core competencies and strengths have attracted significant investment from major countries. The computer software and hardware sector in India attracted cumulative Foreign Direct Investment (FDI) inflow worth $ 44.91 billion between April 2000 and March 2020. The sector ranked second in FDI inflow as per the data released by Department for Promotion of Industry and Internal Trade (DPIIT).

Indian IT’s core competencies and strengths have attracted significant investment from major countries. The computer software and hardware sector in India attracted cumulative Foreign Direct Investment (FDI) inflow worth $ 44.91 billion between April 2000 and March 2020. The sector ranked second in FDI inflow as per the data released by Department for Promotion of Industry and Internal Trade (DPIIT).

Leading Indian IT firms like Infosys, Wipro, TCS and Tech Mahindra are diversifying their offerings and showcasing leading ideas in blockchain and artificial intelligence to clients using innovation hubs and research and development centres to create differentiated offerings.

Some of the major developments in the Indian IT and ITeS sector are as follows:

• In May 2020, SirionLabs, a software-as-a-service (SaaS) provider, raised $ 44 million as part of its Series C round led by Tiger Global and Avatar Growth Capital.

• PE (private equity) investment in the sector stood at $ 11.8 billion across 493 deals in 2019.

• In January 2020, Nippon Telegraph and Telephone, a Japanese tech announced its plans to invest a significant part of its $ 7 billion global commitment for data centres business in India over the next four years.

• In February 2020, Tata Consultancy Services bagged a contract worth Rs 10,650 crore ($ 1.5 billion) from pharma company Walgreens Boots Alliance.

• UK-based tech consultancy firm, Contino, was acquired by Cognizant.

• In May 2019, Infosys acquired 75 % stake in ABN AMRO Bank’s subsidiary Stater for $ 143.08 million

• In June 2019, Mindtree was acquired by L&T.

• Nasscom has launched an online platform which is aimed at up-skilling over 2 million technology professionals and skilling another 2 million potential employees and students.

• As of February 2020, there were 417 approved SEZs across the country with 274 from IT & ITeS and 143 as exporting SEZs.

Growth Drivers

The Indian IT&ITeS sector’s consistent growth continued unabated during the last year too. While exports remined the main stay of the business, domestic IT consumption has been on a growth path on account of increase in digitalization, growing startup ecosystem and favourable government policies.

The main drivers of this growth include the rising global demand, huge IT talent pool, policy support, domestic growth in consumption and significant growth in India’s IT infrastructure.

The government considers IT among 12 champion service sectors for which dedicated action plans being put in place. The government is also placing liberal policies for raising capital, seed money and is also helping in ease of doing business.

The government’s IT-SEZ plan is also helping the growth of the industry immensely. These SEZs have been initiated with an aim to create zones that lead to infrastructural development, exports and employment. As of March 2020, there were 421 approved SEZs across the country, and of these, 276 are from IT & ITeS and 145 are exporting SEZs. Over 50 cities already have basic infrastructure and human resource to support the global sourcing and business services industry. Some cities are expected to emerge as regional hubs supporting domestic companies.

The government’s IT-SEZ plan is also helping the growth of the industry immensely. These SEZs have been initiated with an aim to create zones that lead to infrastructural development, exports and employment. As of March 2020, there were 421 approved SEZs across the country, and of these, 276 are from IT & ITeS and 145 are exporting SEZs. Over 50 cities already have basic infrastructure and human resource to support the global sourcing and business services industry. Some cities are expected to emerge as regional hubs supporting domestic companies.

Exports have been the biggest contributor of India’s IT business and growing spend on digital products is going to help further. As per Nasscom, global digital spend is expected to increase from $ 180 billion in 2017 to $ 310 billion by 2020. India’s IT industry is increasingly focusing on digital opportunities as digital is poised to be a major segment in the next few years. It is also currently the fastest growing segment, growing over 30 % annually. In India, domestic market of computer services is growing faster than their export, which is fueled by the government’s Digital India programme. Export revenue from digital segment already forms about 20 % of the industry’s total export revenue. The figure was estimated at $ 33 billion in FY19 and revenue from digital segment is expected to comprise 38 % of the forecast $ 350 billion industry revenue by 2025.

Road Ahead

Besides the potential in offshoring business, the Indian IT&ITeS industry is expected to grow at a faster pace in the coming years on account of Corona-induced aftereffects. The pandemic forced the whole world confined to their homes and the offices and businesses are virtually running from home. This brought huge changes in the WFH culture and rapid transformation in the home infrastructure. Businesses across the globe helped their employees improve their IT infrastructure at home and deployed technology solutions that help in remote working.

Besides the potential in offshoring business, the Indian IT&ITeS industry is expected to grow at a faster pace in the coming years on account of Corona-induced aftereffects. The pandemic forced the whole world confined to their homes and the offices and businesses are virtually running from home. This brought huge changes in the WFH culture and rapid transformation in the home infrastructure. Businesses across the globe helped their employees improve their IT infrastructure at home and deployed technology solutions that help in remote working.

This saw a surge in IT deployments and solutions purchases across the globe. This trend is going to stay longer than is anticipated and will boost India’s IT&ITeS sector.

Technologies, such as telemedicine, health, remote monitoring solutions and clinical information systems, would continue to boost demand for IT service across the globe. IT sophistication in the utilities segment and the need for standardisation of the process are expected to drive demand.

Because people stayed at home, digital content consumption increased during the ongoing pandemic. Digitisation of content and increased connectivity is leading to a rise in IT adoption by media, and this trend is expected to continue in coming days as well.

Besides, RBI is executing a plan to reduce online transaction costs to encourage digital banking in India. The rollout of fifth generation (5G) wireless technology by telecommunication companies is one more factor that is expected to bring at least

$10 billion global business to Indian IT firms by 2019-25.

Download masked Aadhaar to improve privacy

Download a masked Aadhaar from UIDAI to improve privacy. Select masking w...

Sterlite Technologies' Rs 145 crore claim against BSNL rejecte

An arbitrator has rejected broadband technology company Sterlite Technolog...

ID-REDACT® ensures full compliance with the DPDP Act for Indi

Data Safeguard India Pvt Ltd, a wholly-owned subsidiary of Data Safeguard ...

Happiest Minds brings in an innovative GenAI chatbot

Happiest Minds Technologies has announced the new GenAI chatbot - ‘hAPPI...

Salman Khan trolled for singing with B Praak at Anant Ambani's

To celebrate Mukesh Ambani's youngest son Anant Ambani’s 29th birthday

Disney+ Hotstar wins the Best OTT Platform of the year

Film Critics Guild and Group M Motion Entertainment, in collaboration with

SISL elevates Ankita Wadhawan as CEO—End User Computing

The IT service provider, SISL in a LinkedIn post announced the elevation

InfoVision appoints Radhika Venkatraman to its Advisory Board

Global digital services company, InfoVision has announced the appointment

Lenovo aims to solve customers' critical business needs throug

enovo recognizes the immense potential and the crucial role that technology

AMD Pensando innovation CONTINUES

In 2022, AMD announced its acquisition of Pensando Systems, an addition to

Canon India Introduces 4K Remote PTZ Camera Controller & 4K In

Canon India, a leading company in digital imaging solutions, further solidi

Dell Technologies launches the new consumer and gaming portfol

Dell Technologies has unveiled its newest line of AI-enabled consumer PCs

IBALL WORLDWIDE PVT. LTD.

FINOLEX INDUSTRIES LTD.

INFOSYS TECHNOLOGIES PVT. LTD.

DIGISOL SYSTEMS LTD.

Technology Icons Of India 2023: Rajendra Singh Pawar

Rajendra Singh Pawar is an entrepreneur and businessperson who founded...

Technology Icons Of India 2023: Nandan Nilekani

Nandan Nilekani is the Co-Founder and Chairman of the Board, Infosys T...

Technology Icons Of India 2023: C P Gurnani

CP Gurnani (popularly known as ‘CP’ within his peer group), is the...

New defence PSUs will help India become self-reliant

MIL, India’s biggest manufacturer and market leader is engaged in Pr...

STPI encouraging software exports from India

Software Technology Parks of India (STPI) is an S&T organization under...

ECIL continues to keep India ahead in the growth of Information Technology and Electronics

ECIL played a very significant role in the training and growth of high...

IVALUE INFOSOLUTIONS PVT. LTD.

: iValue Info Solutions is a value added distributor, provides solutio...

REDINGTON INDIA LIMITED

Redington (India) Limited operates in the IT product distribution busi...

TECHNOBIND SOLUTIONS PVT. LTD.

TechnoBind’s business model is focused on identifying and partnering...