Indian Mobile Phone Industry : Steady Growth

By MYBRANDBOOK

Though currently dominated by the Chinese brands, the Indian mobile phone market is staring at completely different dynamics in coming times on account of Covid-19, Indo-China border dispute and PLI scheme

India is the second largest smartphone market, just behind China, and among one of the fastest growing markets in the world. The sheer size of the market, more than 300 million untapped population and plethora of handset options are some major factors that are helping the nation posting impressive growth year over year. In FY 2020, the country shipped close to 283 million mobile phones including more than 150 million smartphones, and registered a Y-o-Y growth of 8%. And that too despite the Covid-19 related business lethargy in March. The deadly disease coupled with India-China border dispute in the following months are, however, turning out to be a blessing in disguise for the Indian mobile phone and electronics industry as many of global firms having manufacturing facilities in China are showing interest to shift their bases to India.

Market Dynamics

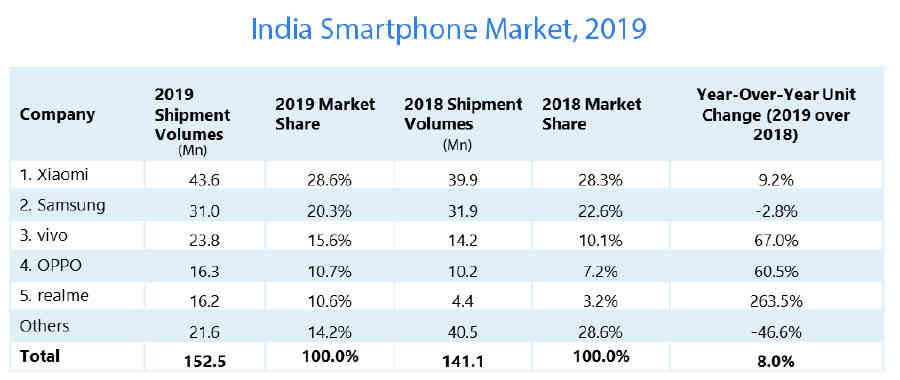

India’s smartphone market shipped 152.5 million units in 2019, according to IDC, with a modest 8.0% year-over-year (YoY) growth. The overall mobile phone market, with annual shipments of 282.9 million units, declined by (-12.3%) YoY in 2019 due to fewer 4G feature phones.

Online distribution channel, like previous years, registered impressive growth of 18.4% capturing a market share of 41.7% in 2019 as per the research firm. Many of the firms held back their online exclusive models to be sold in offline channels. This resulted in slow offline growth of just 1.6% in the year 2019. The reasons for online growth can be attributed to many factors including multi-prong offers and schemes, No cost EMIs, cashback offers etc.

Smartphone ASPs stood at $163 in 2019, registering 2.8% YoY growth with the sub-$200 segment still accounting for 79% of the market. The mid-range segment of $200-500 accounted for the strongest YoY growth of 55.2%, accounting for 19.3% of the overall smartphone market. In the mid-premium ($300-500) segment, vivo continued to lead the market with 28.0% share in 2019, on the back of the high selling vivo V15 Pro, followed by OnePlus at 20.2% share owing to the OnePlus 7 model. In the premium ($500+) segment, Apple surpassed Samsung for the leadership position with a market share of 47.4% in 2019, driven by aggressive price drops on previous generation models, bank offers on debit/credit cards, strong e-Tailer sales momentum, and a lower iPhone 11 launch price compared to the iPhone XR.

Of the entire year, the Q3 smartphone shipments were a record-breaking one. The country shipped 46.6 million smartphones in the three month period ended September 2019 registering a 26.5% Q-o-Q growth. This was driven by multiple online sale festivals, new model launches, and price corrections on a few key models by various brands. While the low-end price segment of $200 still accounted for 80% of the overall India smartphone market in 3Q19, its share dropped by five percentage points YoY at the cost of the mid-range segment of US $200-$500, gaining six percentage points to 18.9% in 3Q19. The fastest growing segment in 3Q19 was $300-500 with double the shipments YoY as key models like the OnePlus 7, Redmi K20 Pro and vivo V15 Pro had good traction. $200-300 was the second fastest growing segment with 47.8% YoY growth in 3Q19, with strong shipments of the Galaxy A50, Redmi Note 7 Pro and vivo Z1 Pro. The ASP for the overall smartphone market was $159, with 2.7% YoY growth in 3Q19.

In Q4, a total of 36.9 million smartphone units were shipped to the country showing a 5.5% YoY growth but a 20.8% quarter-on-quarter decline. Usually the third quarter sees heavy channel loading in preparation for the Diwali festive period, and the last quarter of the year sees a cyclical dip as channels focus on clearing leftover inventory. Owing to multiple rounds of sales by e-Tailers beyond the festive quarter continuing into December, the online channel registered 11.2% YoY growth in 4Q19 with a share of 43.3%. However offline shipments remained flat with 1.4% YoY growth in 4Q19.

The ASP for 4Q stood at an all-time high of $172, as shipments in $200-300 grew by 71.9% YoY on the back of fast selling Galaxy M30s and vivo S1, while strong shipments of the newly launched iPhone 11 series drove the $700 and above segment. In the mid-premium ($300-500) segment in 4Q19, OPPO surpassed OnePlus for the leadership position with a share of 26.8% and 24.4% respectively with the fast-moving Reno 2 series. In the premium ($500+) segment, Apple reached a record 75.6% market share.

In Q2, total shipment of 36.9 million was recorded, with a 9.9% year-on-year (YoY) and 14.8% quarter-on-quarter (QoQ) growth. A total of 69.3 million mobile phones were shipped to India in 2Q19, which was up 7.6% over the previous quarter.

In Q1 India’s smartphone market got off to a good start with a total shipment of 32.1 million units, maintaining a healthy 7.1% year-on-year (YoY). High channel inventory from the previous quarter resulted in a sequential decline of 8.4%. Large shipments in the festival quarters of 3Q18 and 4Q18 led to high channel inventory, leading to flat YoY growth in offline channels in 1Q19. But new products still arrived in Samsung’s A series and online-heavy vendors like Xiaomi and Realme expanded to offline counters.

Chinese Dominance Continues

The Indian mobile phone market is primarily dominated by the Chinese brands and close to 75% of smartphones remained under the dragon’s hold in 2019.

Xiaomi registered annual shipments of 43.6 million units in 2019, the highest ever smartphone shipments made by any brand in a year, with a growth of 9.2% YoY. The Redmi Note 7 Pro and Redmi 6A were the highest shipped devices nationally in 2019. Xiaomi continued to dominate in 4Q19 with 15.9% YoY growth on the back of newly launched Redmi Note 8 Pro/8A/Note 8/8 series. The brand commanded a market share of 28.6% in FY2020, IDC reports.

Samsung shipped a total of 31 million smartphones during the last year and placed in distant second position with a market share of 20.3%. The company registered declining shipments amongst the top five brands with a (15.4%) YoY decline in 4Q19. The refreshed Galaxy As series was unable to sustain its momentum owing to a delay in launch time and a gap in phasing out the older Galaxy A clubbed with fewer channel incentives. However, its Galaxy M series and in particular Galaxy M30s performed well in the online segment, helping to revive its online share in 4Q19 at an all-time high of 16.6%. Despite the attractive cashback offers in the premium ($500+) segment, Samsung faced heat from offerings by Apple, leading to channel inventories.

Vivo, with annual shipment of 23.8 million in the last year, retained its third place in the Indian smartphone chart. The firm captured a market share of 15.6% showing year-on-year growth of 67%. During the last quarter of the financial year it also became the leader in the offline channel, ahead of Samsung on the back of multiple price drops across major models in Nov/Dec’19 to clear off inventory post-Diwali, clubbed with attractive channel schemes in 4Q19. The continued focus on its offline channel, despite the exclusive line-up in online channel and presence across price segments, led to this phenomenal rise in 2019.

OPPO shipped 16.3 million phones during the last year and was placed at the fourth position with a market share of 10.7% In 4Q19, the company posted a huge YoY growth of 88.4% on the back of its affordable A series and successful Reno 2 series. The offline channel remains upbeat with the incentives and offerings and spends on marketing initiatives.

Realme shipped 16.2 million smartphones in 2019 and had a market share of 10.6%. However, if compared the market share on a yearly basis, the company shows a growth of 264% over 2018. The realme C2 featured in the top 5 model list in the online channel in 2019. Further, its newly launched X2 Pro became the highest shipped device in the mid-premium $300-500 segment in 4Q19.

Transsion Group brands (Itel, Infinix, and Tecno) reached its highest ever market share during the last quarter of the year, registering 78% YoY growth. Transsion remained strong in tier 3, tier 4 cities, and rural India. Itel continues to be the number one smartphone brand in the entry-level sub-INR 4,000 (~$ 55) price segment, while Tecno and Infinix showed good YoY growth in the INR 6000-INR 10000 (~$ 80-$130) segment by bringing attractive features in budget level smartphones. Itel also remained the #1 feature phone brand during the quarter.

Poco that debuted as an Independent brand, got off to a good start by capturing a 2% market share during its first entire month of operations in March 2020. It was also among the top five brands in the INR 15-20K (~$200-$260) price segment.

Apple was one of the fastest-growing brands in the year 2019 driven by multiple price cuts on its XR device, thanks to local manufacturing in India. Yet, its market share is less than a percent in India.

Outlook

The Indian mobile phone industry got its biggest jolt at the beginning of the financial year due to Covid-19 pandemic. The markets remained shut for the entire Q1 and there were some online sales started in June.

In the previous three month period, India’s smartphone market saw a relatively flat opening quarter with year-over-year (YoY) growth of 1.5% to 32.5 million units in 1Q20. Despite that, India was the only country amongst the top 3 to see any growth, as both China and USA markets declined YoY by (-20.3%) and (-16.0%) respectively in 1Q20. Inventories remained high throughout the distribution channels due to seasonally low demand in the first quarter, clubbed with the Covid-19 impact from mid-March 2020 onwards as the nationwide lockdown was announced.

The impact of the pandemic is expected to continue for another two quarter, experts believe and the market may shrink by 10-12% during this phase.

There is one more reason that would deepen the shrink – the China-India border dispute that is continuing Since June 2020.

If you look at the contribution of Chinese brands, their market share fell to 72% in Q2 2020 from 81% in Q1 2020. This was mainly due to the mixture of stuttering supply for some major Chinese brands such as OPPO, vivo and realme, and growing anti-China sentiment that was compounded by stringent actions taken by the government to ban more than 50 apps of Chinese origin and delay the import of goods from China amid extra scrutiny. This all resulted from the India-China border dispute during June.

However, huge opportunities lie ahead for India to become a manufacturing and export hub for handsets owing to the Indian government’s push. After the launch of the Rs 41000 crore. PLI scheme in April, OEMs are planning to set up production bases in India. For example, Lava, a homegrown brand is also planning to shift its handset production from China to India to leverage the PLI scheme. Apple is also planning to shift 20% smartphone production from China to India. Post announcement of schemes likes NPE-2019 and PLI, the Indian mobile phone industry is aiming at a revenue of $100 billion including $40 billion from exports by 2025.

This is going to boost the morale of local manufacturers including Lava, Karbonn and Micromax. Couple of the. Companies from the list have already waken up from their slumber and applied to the Government of India to take the benefits of the PLI scheme by commencing their smartphone production in India.

Further, Google’s partnership with Jio is expected to bring a highly affordable 4G Android smartphones to the Indian consumers. The ‘VocalforLocal’ sentiment will also have its play in coming times.

Feature phone is one more segment that might see some growth in coming times. India is home to more than 350 million feature phone users and the feature phone market was the worst affected segment as it declined by a massive 68% YoY in Q2 2020 as consumers in this highly cost-sensitive segment tried to save money by reducing discretionary purchases. In the near-to-mid term, this could actually boost the used and refurbished mobile phone market.

Happiest Minds brings in an innovative GenAI chatbot

Happiest Minds Technologies has announced the new GenAI chatbot - ‘hAPPI...

Government mandates encryption for CCTV cameras to ensure netw

In the wake of issuing an internal advisory on securing CCTV cameras at g...

TRAI recommends allowing only Indian entities to participate i

The Telecom Regulatory Authority of India (TRAI) has recommended that onl...

Galaxy AI is available on more devices with Samsung One UI 6.1

Samsung has expanded the range of smartphones to which One UI 6.1 and Gala...

Disney+ Hotstar wins the Best OTT Platform of the year

Film Critics Guild and Group M Motion Entertainment, in collaboration with

Miss World 2024: Krystyna Pyszková of the Czech Republic wins

Krystyna Pyszková of the Czech Republic has been crowned as the 71st Miss

Brillio appoints Ashish Singh to its Board of Directors

Brillio has announced that Ashish Singh has been appointed to the company�

JSW One Platforms ropes in Dr Ranjan Pai as Independent Direct

JSW One Platforms, part of US$23 billion JSW Group has appointed Dr Ranjan

HPE Aruba Networking bridging the physical and digital worlds

The information technology industry is a critical component of the 21st cen

ESDS commits to presenting clients with the latest technology

According to a NASSCOM report, the Indian IT industry experienced its stron

HP launches first laptop in India with Microsoft CoPilot butto

HP has launched sleek and stylish Envy x360 14 laptops in India which beco

OnePlus debut its Nord CE4 smartphone

OnePlus Nord CE4 continues the trend of attention-grabbing design with two

HIMACHAL FUTURISTIC COMMUNICATIONS LTD.

VVDN TECHNOLOGIES

LAVA INTERNATIONAL LTD.

AGGRESSIVE ELECTRONICS MANUFACTURING SERVICES PVT. LTD.

Technology Icons Of India 2023: Amit Chadha

. An influential leader in the engineering services industry for over ...

Technology Icons Of India 2023: Sunil Gupta

Sunil Gupta is the Co-founder, Managing Partner & CEO of Yotta Infrast...

Technology Icons Of India 2023: Madhabi Puri Buch

Madhabi Puri Buch is the chairperson of the securities regulatory body...

ECIL continues to keep India ahead in the growth of Information Technology and Electronics

ECIL played a very significant role in the training and growth of high...

NIC bridging the digital divide and supporting government in eGovernance

The National Informatics Centre (NIC) is an Indian government departme...

BBNL empowering rural India digitally

BBNL provide high speed digital connectivity to Rural India at afforda...

NETPOLEON SOLUTIONS

Netpoleon Group is a Value-Added Distributor (VAD) of Network Security...

TECHNOBIND SOLUTIONS PVT. LTD.

TechnoBind’s business model is focused on identifying and partnering...

WPG C&C COMPUTERS & PERIPHERALS PVT. LTD.

WPG C&C Computers & Peripherals (India) was incorporated in 2008 and ...

Private Limited")